DXY popped and dropped last night:

The AUD only popped, like a rocket:

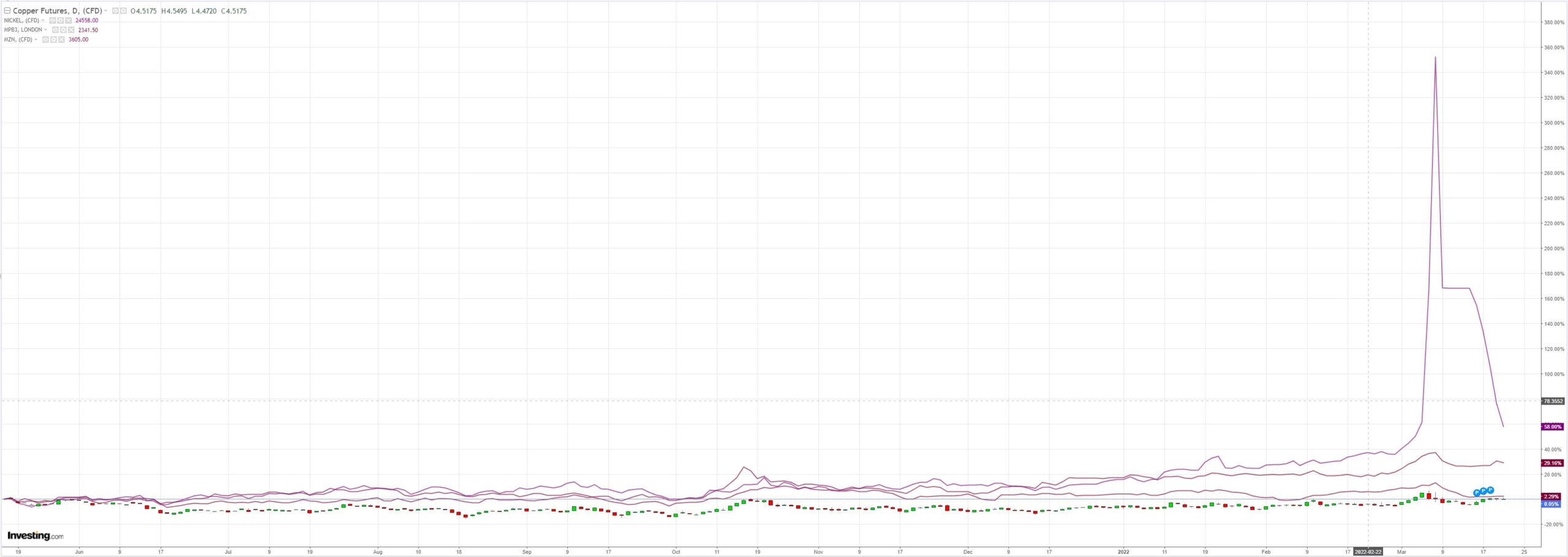

Commodities were relatively weak:

Big miners rolled:

EM stocks were OK:

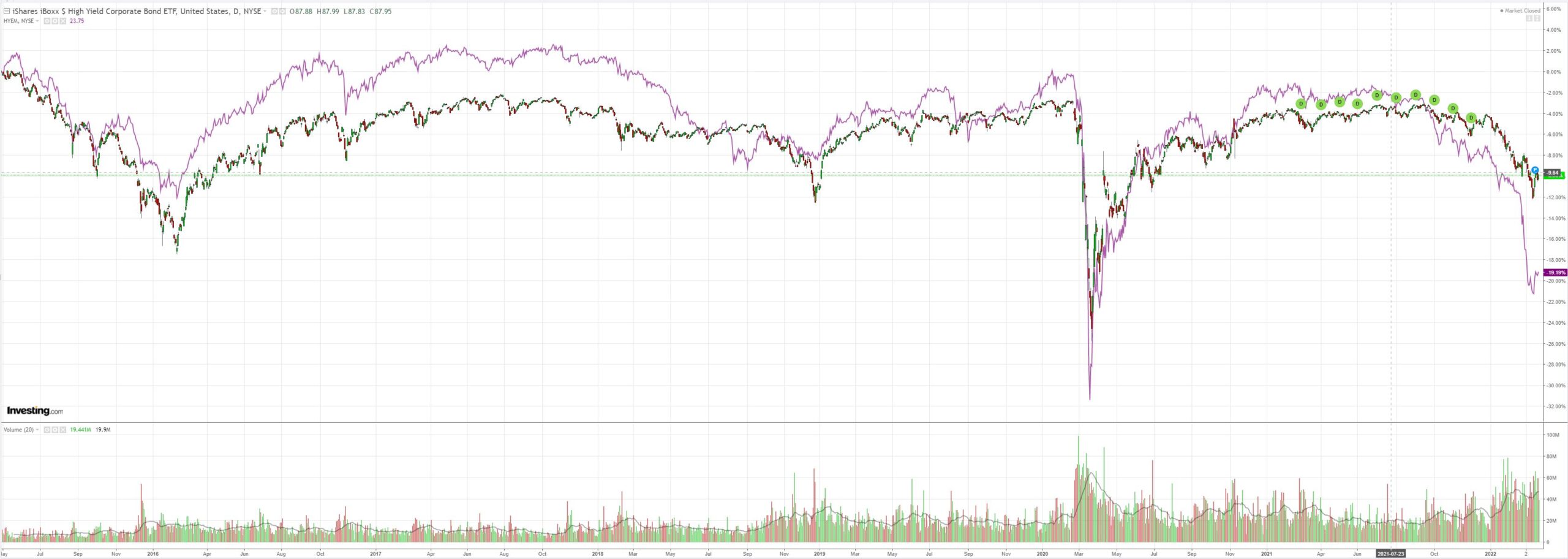

Junk is still lagging not leading this rally, a bad sign:

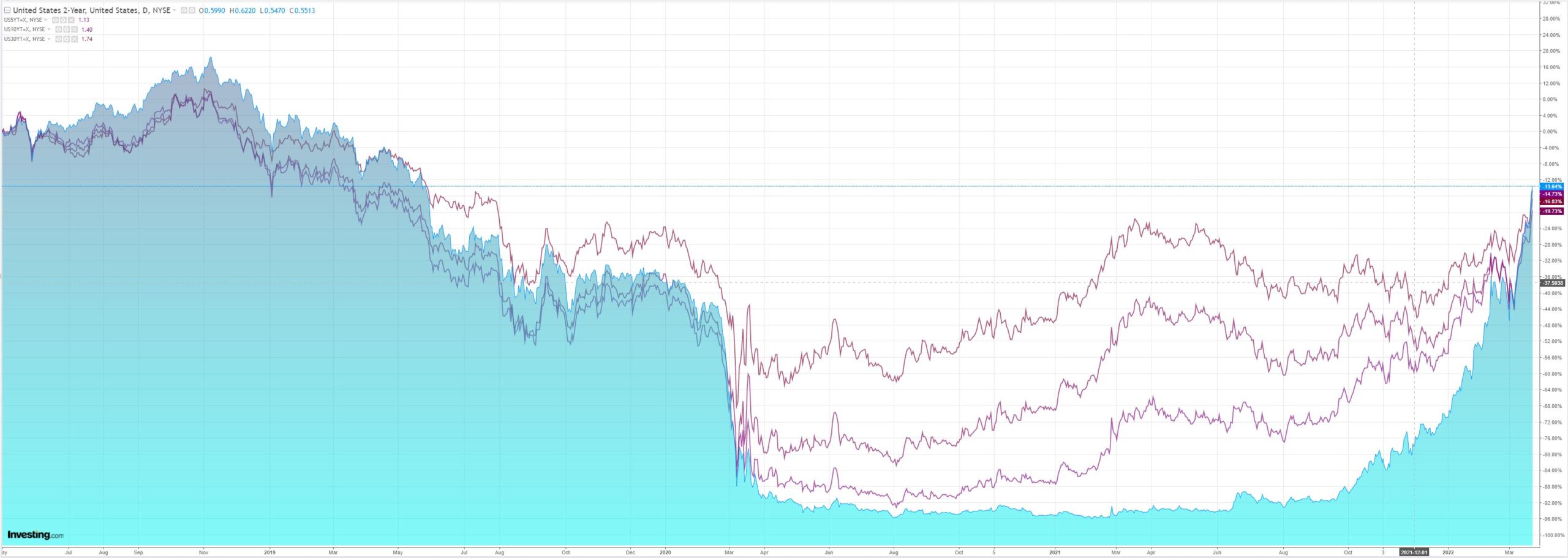

As the yield curve is steamrolled:

But stocks don’t care:

Westpac has the wrap:

Event Wrap

US Richmond Fed activity survey rose to 13 (est. 2, prior 1), due to better than anticipated new orders (rising to +10 from prior -3) and shipments (rising to +9 from -11), as well as increased hiring and wages, in an overall positive report.

Hawkish FOMC member Bullard said that the Fed needs to aggressively curb inflation risks and should not await an easing of geopolitical tensions. He wants to see an early reduction of the balance sheet, and a swift move to slightly restrictive policy levels. Daly said high inflation warrants having interest rates “marching up to neutral” and the Fed considering whether to make policy restrictive.

UK CBI Trends survey of business orders was firmer than expected at 26 (est. 16, prior 20), with both current and future output remaining firm, and export orders liftrisinging from -7 to +7.

ECB’s Villeroy said that there was a danger of over-reacting to current energy price volatility, while de Guindos emphasized that regional banking exposure to Russia was limited and the key concern of the ECB was to monitor second round effects from inflation.

IMF stated that there would be funds available for reconstruction of Ukraine, and the German Fin. Min. suggested an EU Marshal Plan to support Ukraine’s reconstruction.

EU officials continue to float regional fiscal, energy support and transition, security and defence policies in advance of key summits.Event Outlook

Eur/UK: Rising energy prices will remain a key driver of UK consumer inflation in February (market f/c: 0.6%); these inflationary pressures alongside the Russia-Ukraine conflict should continue to weigh on European consumer confidence in March (market f/c: -12.9).

US: The easing of supply issues should support new home sales in February but rising mortgage rates are a headwind (market f/c: 1.1%). FOMC Chair Powell will take part in a BIS panel; Mester and Daly are also due to speak.

The world’s three largest economies are under sustained assault:

- Unprecedented energy and war shock in Europe.

- Unprecedented property bust and COVID shock in China.

- Steepest Fed tightening cycle in 40 years in the US.

It remains my view that the global economy is headed for recession sooner rather than later and, at some point, the fourth horseman – a credit event, – will upset the market applecart.

But, until then, the Ukraine blowoff for commodities makes AUD the hottest ticket in town.