Goldman with the note. My own view is we’ll have suffered a credit event and global recession long before much of the below happens.

—

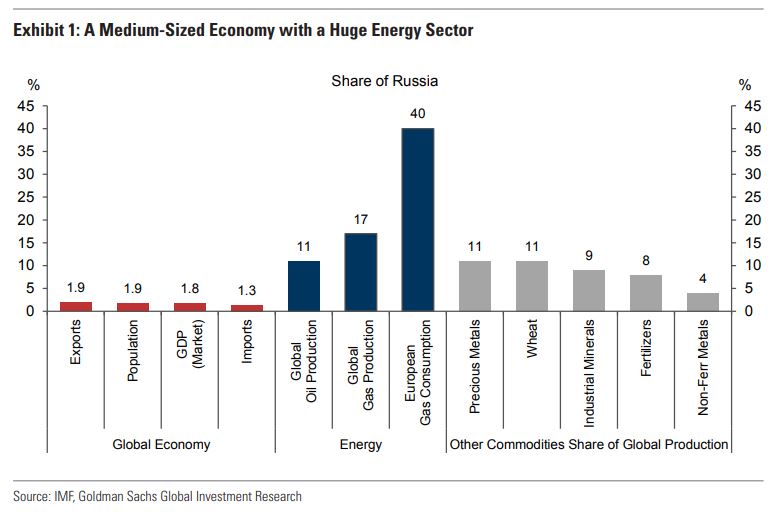

1. Russia’s invasion of Ukraine—and the Western response to it—will exacerbate the supply-demand imbalance that lies at the heart of the global inflation surge. Reducing trade with a current account surplus country via sanctions and boycotts means that the rest of the world needs to produce a larger share of what it consumes. The potential shift is fairly small at an aggregate level, as Russia accounts for less than 2% of global goods trade and GDP. It is considerably larger in oil, where Russia supplies 11% of global consumption. And it is huge in natural gas, where Russia supplies 17% of global consumption and as much as 40% of Western European consumption as of 2021.