There are signs that the global energy shock has peaked and is coming off. Let’s begin at the top with oil. The latest from the EIA short-term outlook:

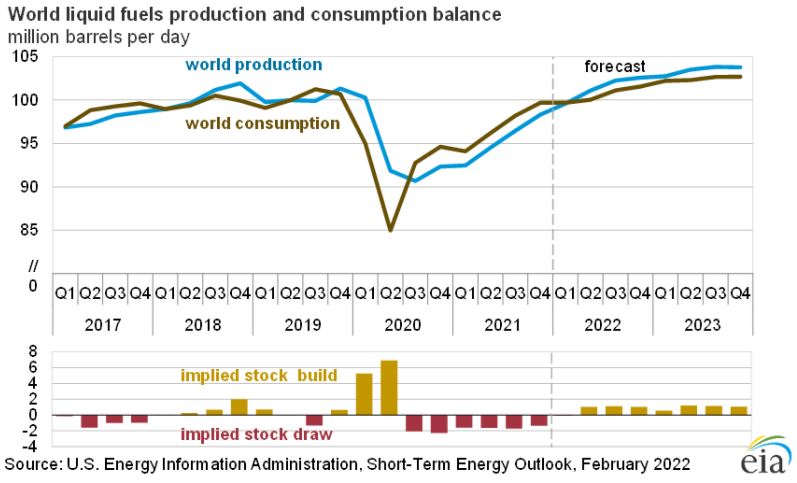

Brent crude oil spot prices averaged $87 per barrel (b) in January, a $12/b increase from December 2021. Crude oil prices have risen steadily since mid-2020 as result of consistent draws on global oil inventories, which averaged 1.8 million barrels per day (b/d) from the third quarter of 2020 (3Q20) through the end of 2021. We estimate that global oil inventories fell further in January—compared with our expectation of an increase in last month’s STEO—and that commercial inventories in the OECD ended the month at 2.68 billion barrels, which is the lowest level since mid-2014. Oil prices have also risen as result of heightened market concerns about the possibility of oil supply disruptions, notably related to tensions regarding Ukraine, paired with receding market concerns that the Omicron variant of COVID-19 will have widespread effects on oil consumption.

We expect Brent prices will average $90/b in February as continuing draws in global oil inventories in our forecast keep crude oil prices near current levels in the coming months. However, we expect downward price pressures will emerge in the middle of the year as growth in oil production from OPEC+, the United States, and other non-OPEC countries outpaces slowing growth in global oil consumption. This dynamic leads to rising global oil inventories from 2Q22 through the end of 2023, and we forecast the Brent spot price will fall to an average of $87/b in 2Q22 and $75/b in 4Q22. We expect the Brent price will average $68/b for all of 2023. However, low inventory levels create an environment for potentially heightened crude oil price volatility and potential risk for prices to rise significantly if supply growth does not keep pace with demand growth. Global supply chain disruptions have also likely exacerbated inflationary price effects across all sectors in recent months. How central banks respond to inflation may affect economic growth and oil prices during the forecast period.

We estimate that 99.0 million b/d of petroleum and liquid fuels was consumed globally in January 2022, an increase of 6.6 million b/d from January 2021. We forecast that global consumption of petroleum and liquid fuels will average 100.6 million b/d for all of 2022, which is up 3.5 million b/d from 2021 and more than the 2019 average of 100.3 million b/d. We forecast that global consumption of petroleum and liquid fuels will increase by 1.9 million b/d in 2023.

That’s a reasonable base case. Wall Street hysteria will keep pressure on prices until the Fed kills it but supply is rebounding.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.