Goldman Sachs with the note:

Inflation trends:

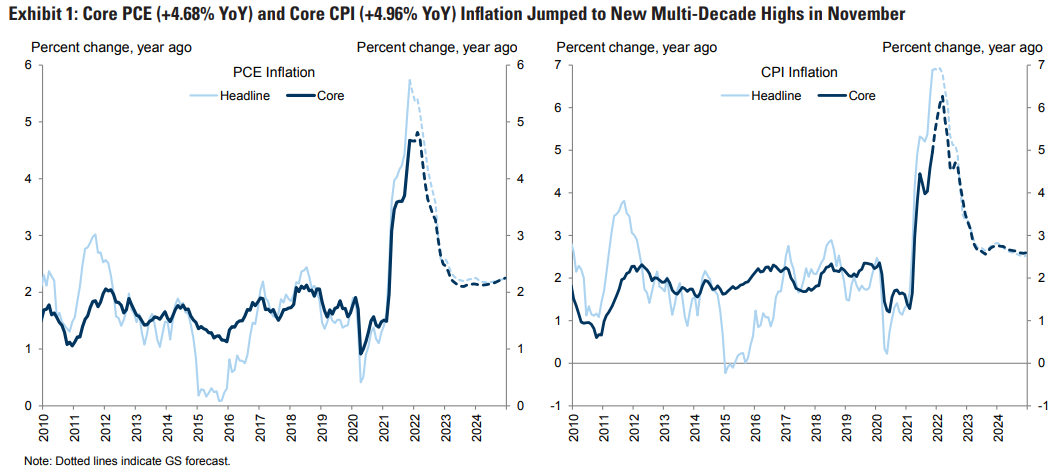

- The core PCE price index rose 0.46% month-over-month in November to a new three-decade high of 4.68% year-on-year, and core CPI inflation rose to 4.96%.

- Core inflation was again boosted by rapid shelter inflation—which has run at the highest level since 1990 over the last three months—and another jump in the prices of durable goods impacted by temporary shortages.

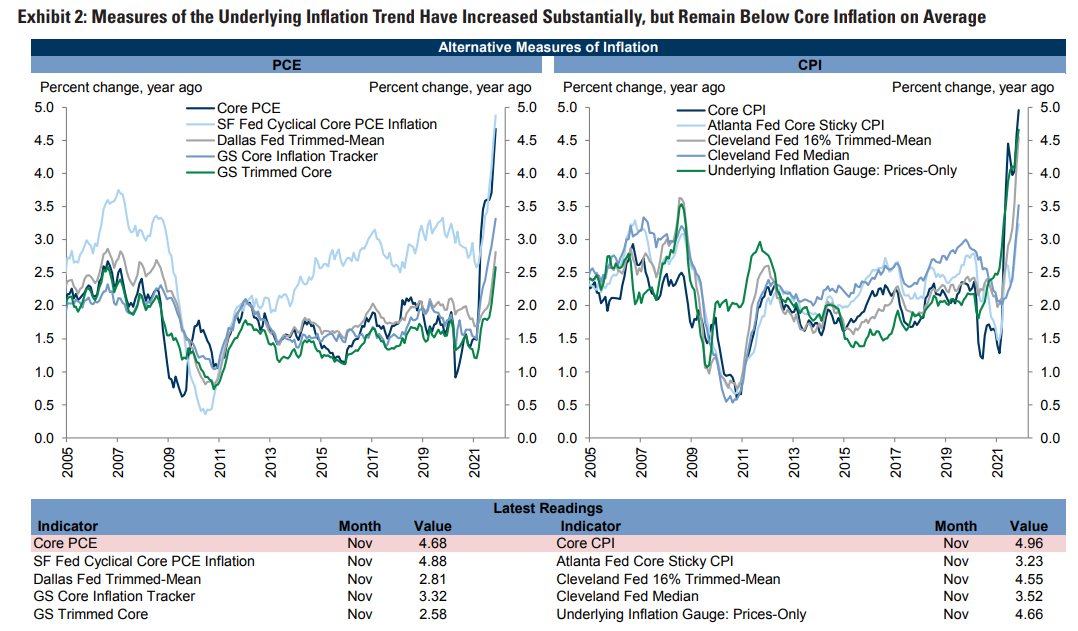

- The role of outliers over the last year is illustrated by the gap between core PCE inflation at 4.68% year-on-year and our GS trimmed core PCE at just 2.58% year-on-year. However, the breadth of inflation has continued to increase and our GS trimmed core PCE has run at an annualized pace of 3.84% over the last three months (vs. 4.82% for core PCE).

Advertisement

Component-level trends:

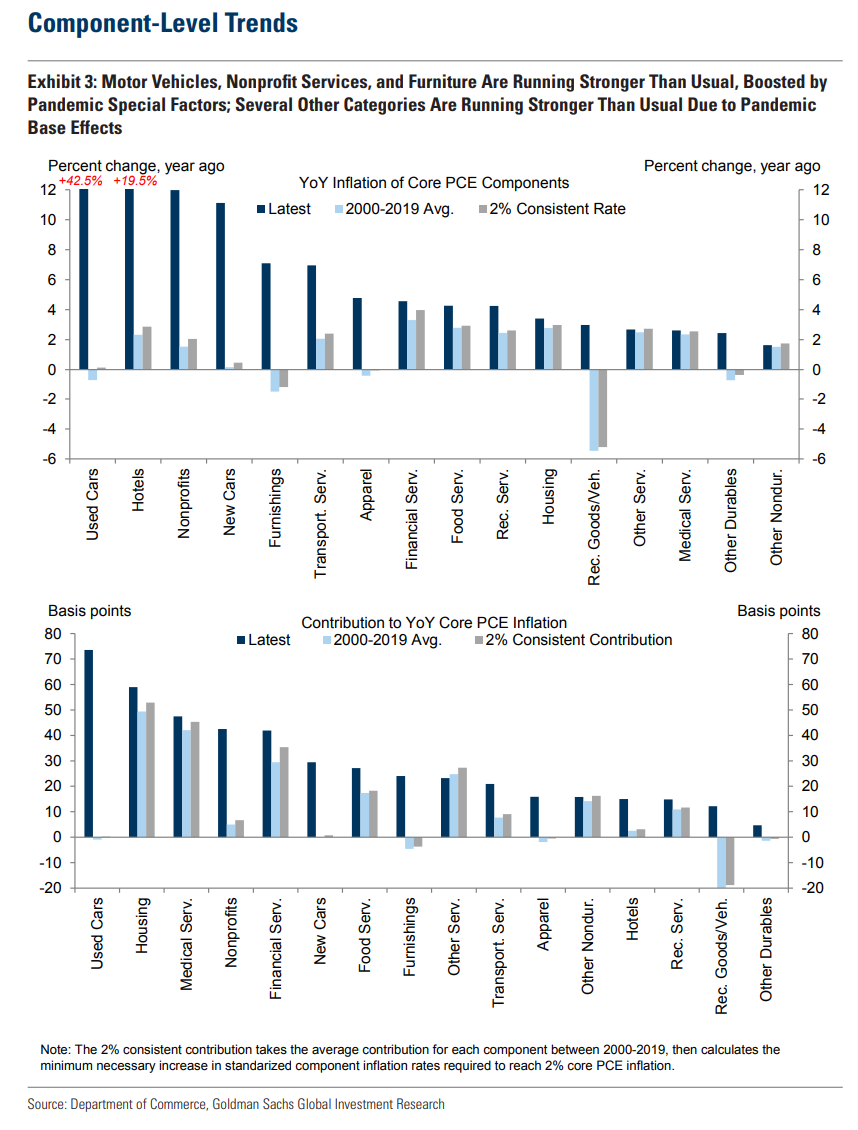

- Used cars, hotels, nonprofit services, new cars, furniture, and transportation services are much stronger than usual on a year-on-year basis, boosted by supply constraints and base effects.

- Used car auction prices increased 3% to 57% above the pre-pandemic level in the first half of December, which could push consumer prices — which are 56% above the pre-pandemic level — even higher.

- Our GS shelter inflation tracker increased to +5.5%, pointing to a pickup in the official shelter series from its current +3.4% year-over-year rate.

- Our high-frequency tracker of hotel prices and airfares has increased to 5% above the 2019 level despite increased virus spread.

Advertisement