McKinsey Global Institute has released a new report entitled, The rise and rise of the global balance sheet, which shows that the market value of the world’s balance sheet tripled in the first two decades of this century, driven by real estate.

Below is the summary of this report:

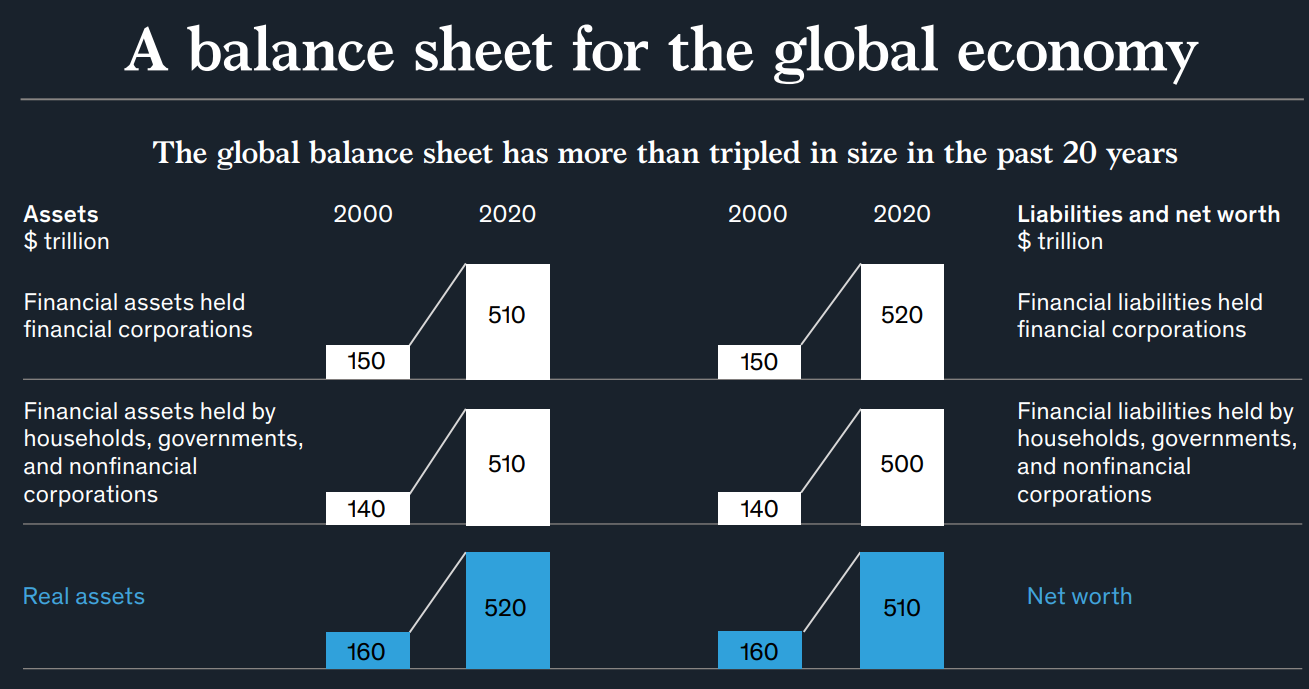

While the state of economies is usually measured by GDP or other metrics of economic flows, this research examines the balance sheets of ten countries representing more than 60 percent of global income: Australia, Canada, China, France, Germany, Japan, Mexico, Sweden, the United Kingdom, and the United States. This view highlights a dual paradox: bricks and mortar make up most of net worth, even as economies turn digital and intangible, and balance sheets have expanded rapidly over the past two decades, even as economic growth has been tepid. How countries and companies adjust to this divergence between wealth and GDP, find 21st-century stores of value, and address growing financial imbalances will determine the future course of the global economy and our wealth.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.