BofA Global Research with the note:

The December FOMC meeting minutes included a lengthy discussion of the timing and speed of Fed balance sheet shrinkage (quantitative tightening or “QT”). The broad message appears to be that QT will start sooner than it did in the previous tightening cycle, and proceed at a faster pace. Even so, we argue here that the Fed’s balance sheet policy will remain accommodative for the next several quarters:

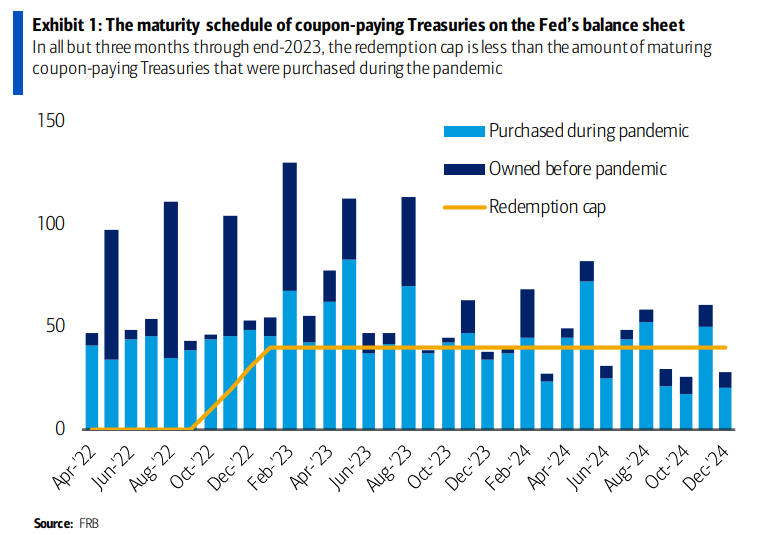

- The Fed has more than doubled its balance sheet during the pandemic.

- Therefore it will have to reinvest a larger quantity of maturing Treasuries even while it is shrinking its balance sheet.

- We expect QT to start in 4Q 2022. But we think the stance of Fed balance sheet policy will remain more accommodative than it was before the pandemic through end-2023.