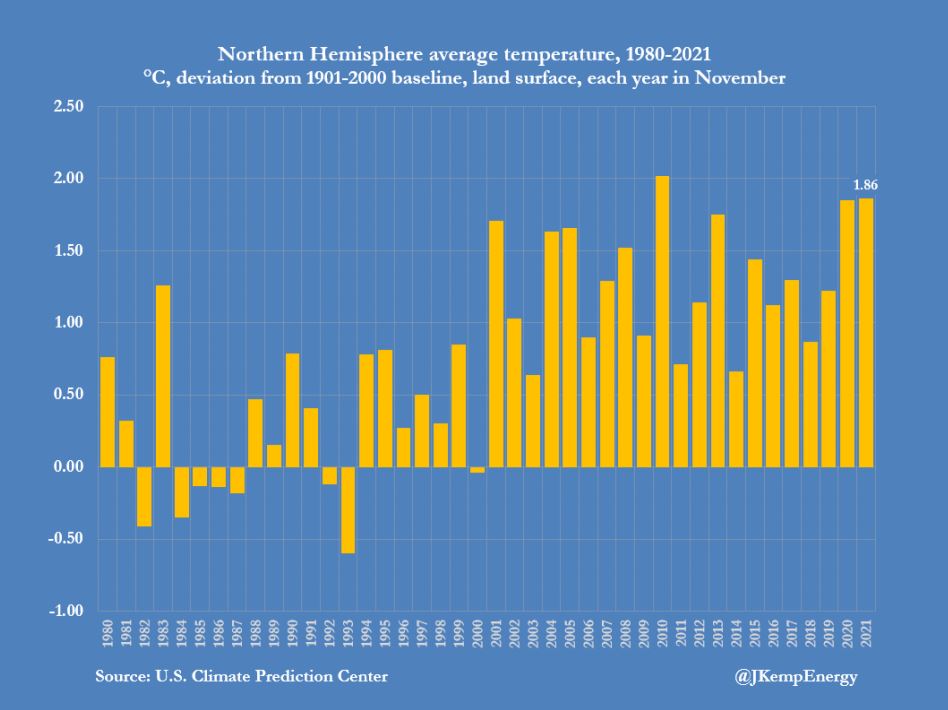

The global energy shock that came out of nowhere last year and has rocked markets and economies ever since is once again easing, this time on a mild northern winter:

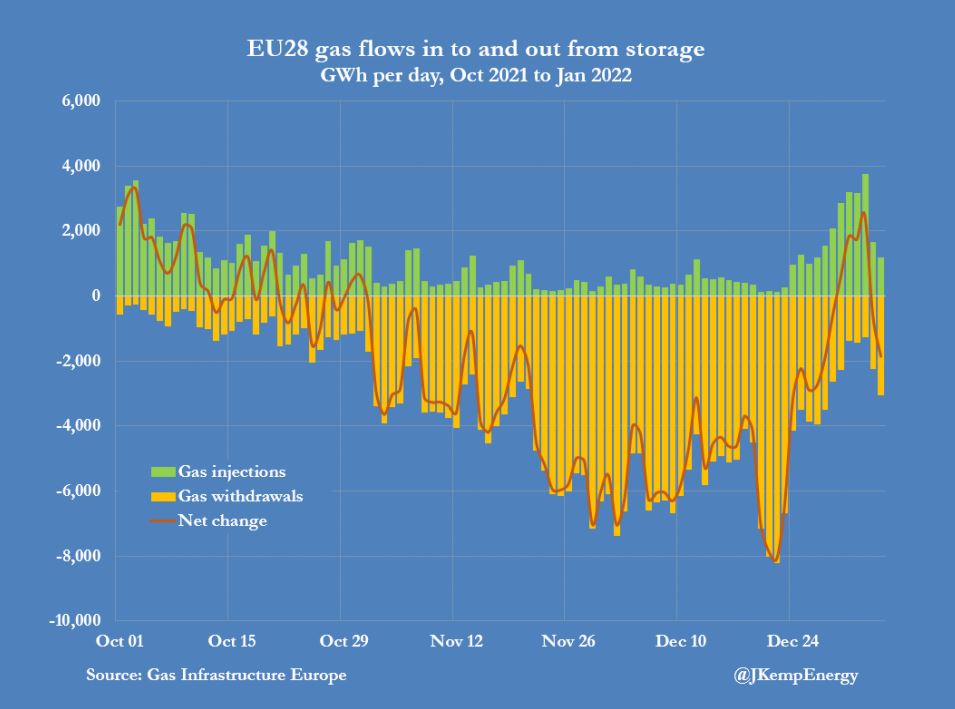

European gas consumption is down and storage has lifted unexpectedly:

Advertisement

The US has also been warm which has helped enable a flood of LNG across the pond: