Deutsche Bank with the note:

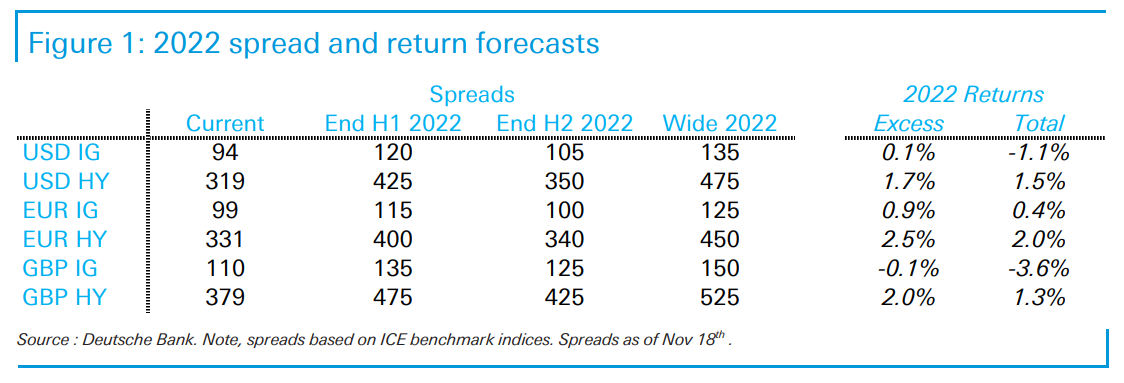

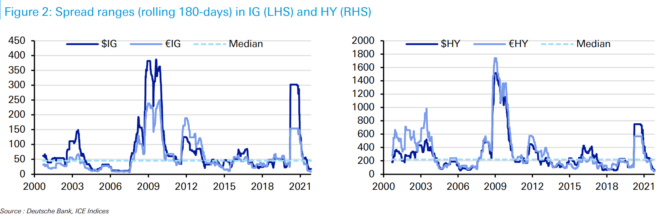

As we close out 2021, it is fair to say that this year has been one of the lowest vol years for credit on record. A perfect calm of the strongest growth for decades, coupled with still extreme level of stimulus has resulted in very low spread ranges.

We think this low vol environment is unlikely to last and spreads will sell-off at some point in H1 when markets reappraise how far behind the curve the Fed is. Even with covid restrictions mounting again in Europe as we go to print, we think it’s more likely that we’ll be in a “growthflationary” environment for 2022. We think the overheating risk is more acute than the stagflation risk, especially in the US. Strong growth and high liquidity should mean that full year 2022 is a reasonable year for credit overall but if we’re correct they’ll be regular pockets of inflationary/interest rate concerns in the market, which we think is more likely to happen in H1.

The full text of this article is available to MacroBusiness subscribers