The ferrous complex was mixed on January 7, 2022 as spot and steel lifted but paper fell:

The rally over Xmas looks like pretty typical seasonality to me. Steel mills finished the year with low iron ore inventories, despite the great and growing port pile, and enough hope for stimmies that restocking made sense.

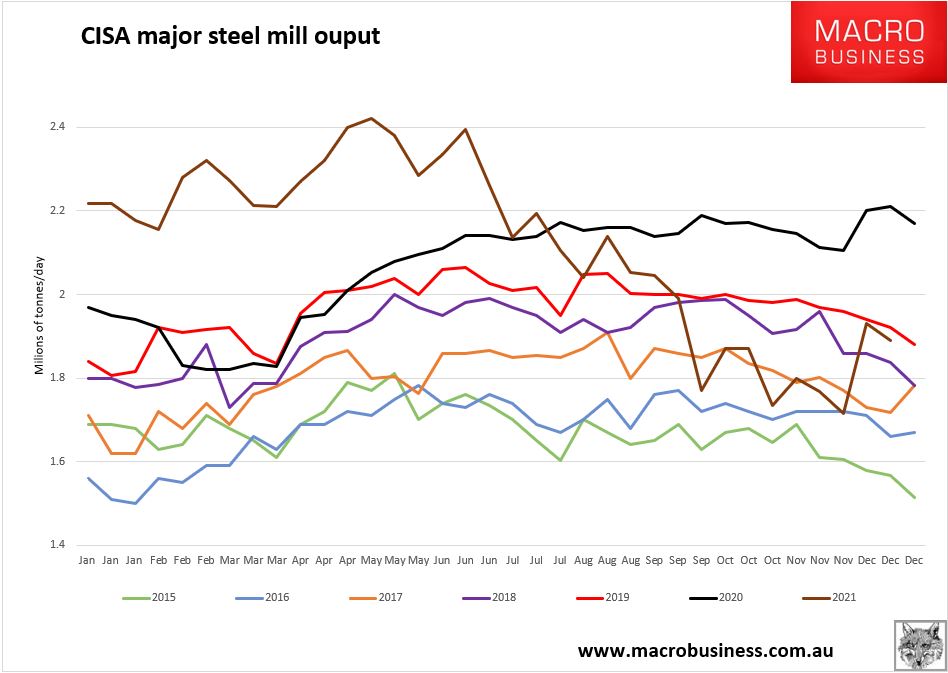

The latest steel output data is also past the worst of the shutdowns, even if it remains very weak, from CISA:

Advertisement