Goldman Sachs with the note:

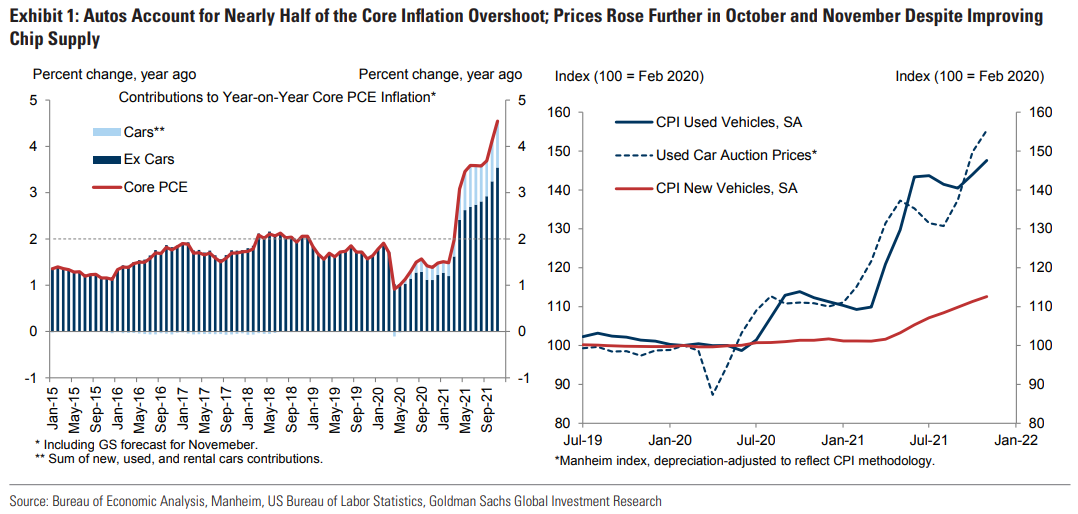

With used car auction prices on the rise again, we revisit the outlook for motor vehicle inflation across three dimensions: 1) the relative prices of new versus used cars, 2) Omicron-driven factory closures in East Asia, and 3) US port congestion.

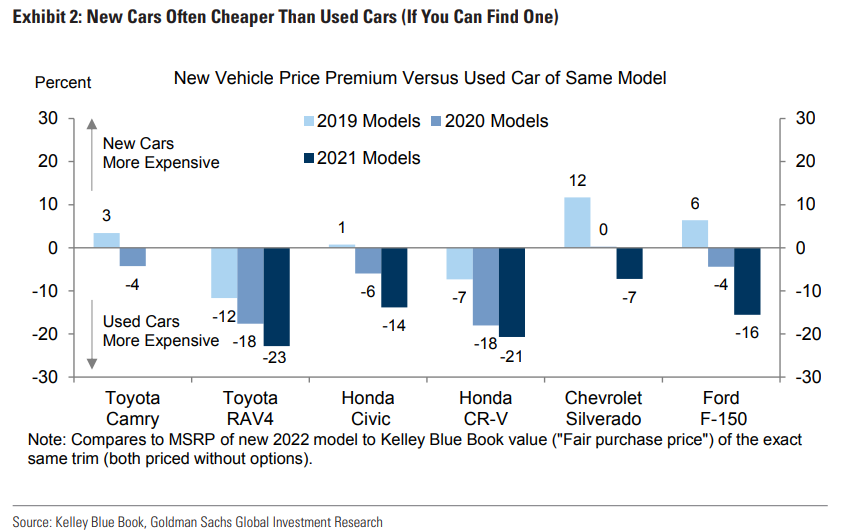

Despite recent appreciation, prices of new cars remain unsustainably low relative to used models, suggesting more inflation in the pipeline. Comparing top-selling new models to Kelley Blue Book values, we find that used models from two years ago are currently selling for ~10% more than their 2022 counterparts—despite the latter’s better technology and zero mileage.

Advertisement