Goldman Sachs with the note:

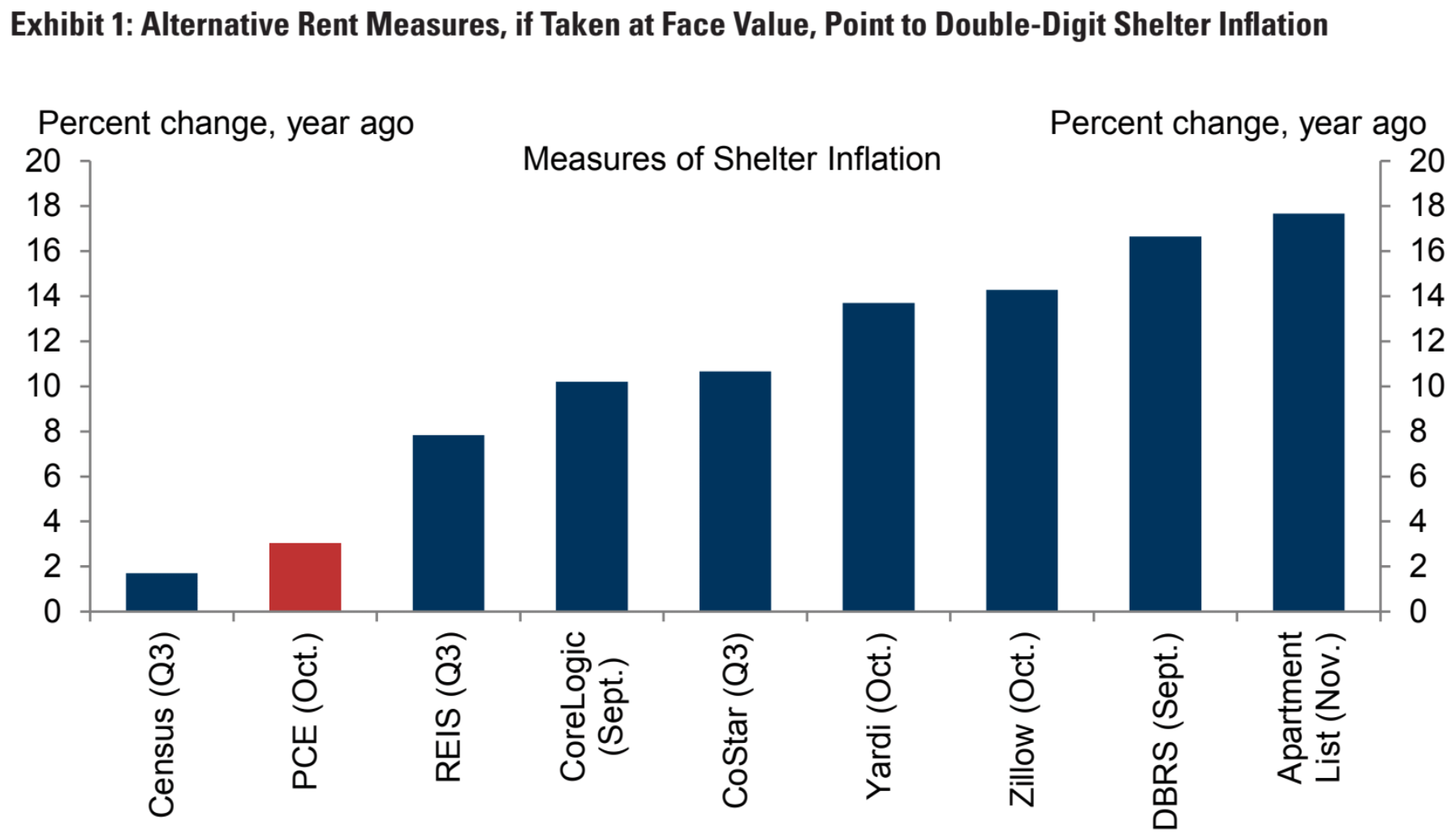

In the spring, we wrote that shelter inflation would rise to 30-year high on the back of substantial home price appreciation and a rapidly improving labor market. Since then, a number of alternative rent measures have increased at dizzyingly high rates, with some pointing to price increases that are almost 15pp above the official shelter inflation measure of 3.0%.

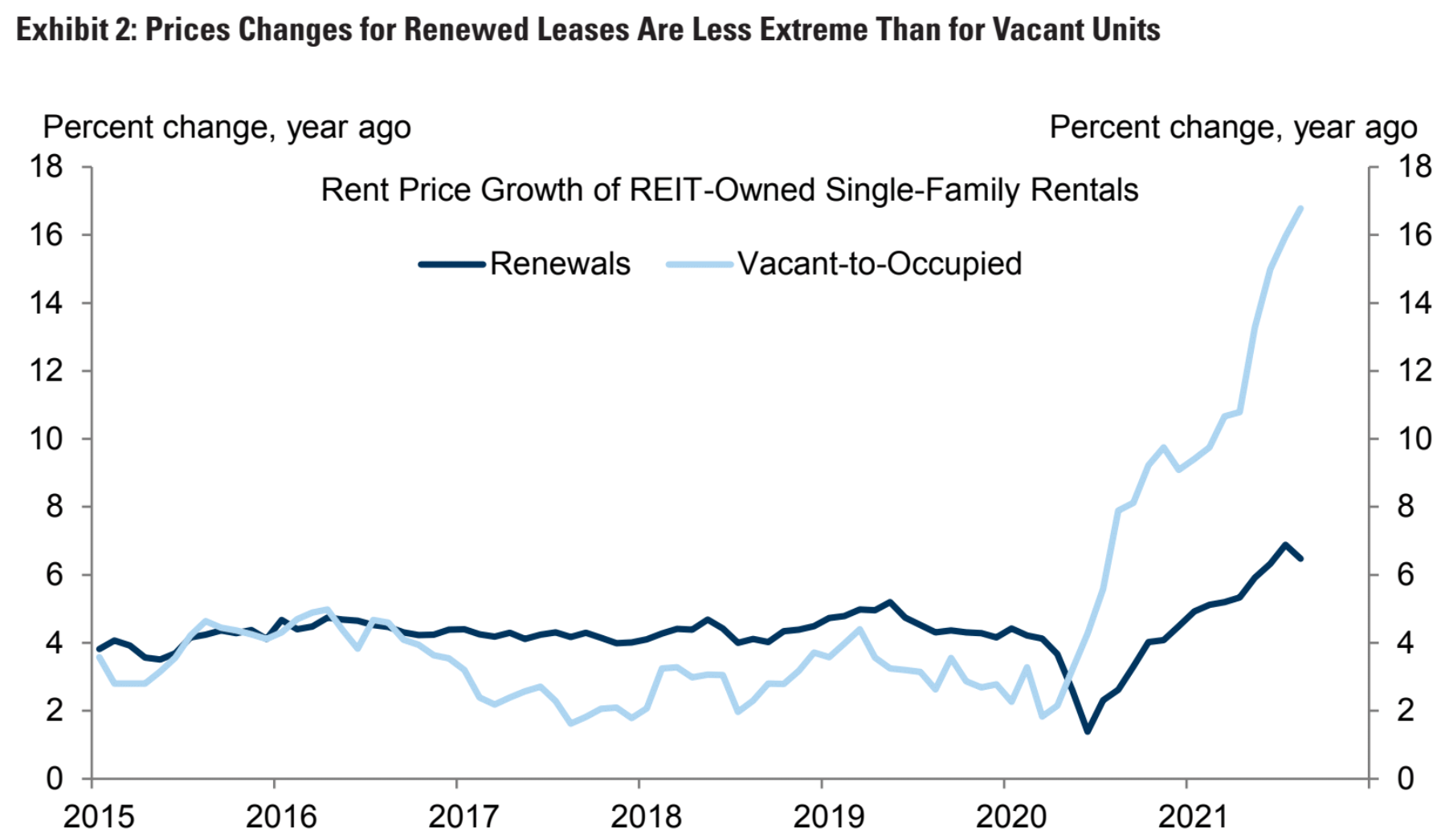

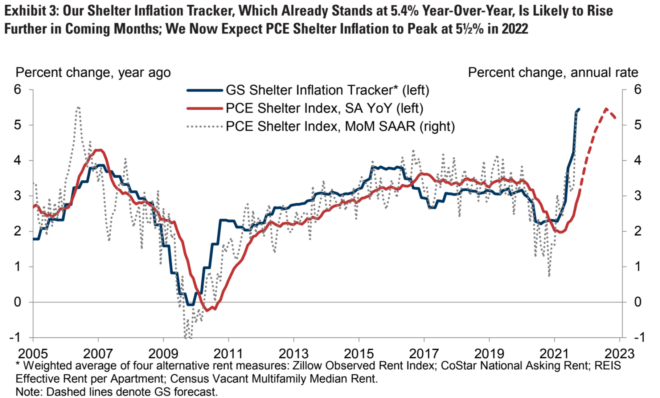

However, we caution that some of these measures could provide a misleading signal about the official data because they focus on units on the market that are turning over, whereas the official measure includes renewed and continuing leases. Our shelter inflation tracker—which translates asking rent measures to the official measure—implicitly adjusts its underlying inputs to account for the gap between asking rents and the rest of the rental stock, and currently points to a more moderate, but still high, +5.4% year-over-year reading.

The full text of this article is available to MacroBusiness subscribers