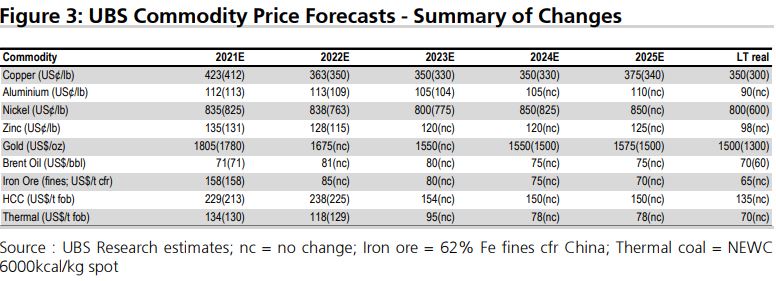

UBS contend that 2022 will not the year for mining, as the macro backdrop weakens as global demand slows down post-pandemic amid tapering of stimulus and easing of supply constraints. They reckon to avoid iron ore and coal, with their new commodity forecasts are as follows:

We maintain a sector underweight but within that w prefer commodities leveraged to EVs and broader energy transition. These include nickel, lithium, aluminium, zinc and, to a lesser extent, copper. Our least-preferred commodities are iron ore and met coal, the latter especially currently trading well above the cost curve. Iron ore prices are still expected to fall to $85/mt in CY22 and $80/mt in CY23 on slowing Chinese demand and ample supply. We believe gold prices are likely to come under pressure from rising real yields, but new Covid variants could spur a ‘safehaven’ bid.

Q: Will commodity prices remain at 2021 levels?

No. Commodity prices looks set to trade lower into 2022 as supply growth outweighs demand growth. China’s property activity will likely fall in 2022, while rest of world goods demand slows as services growth accelerates. Recent policy easing in China aims to moderate recent ~20%-30% y/y falls in property activity (which is one-quarter of GDP), rather than the start of a cyclical expansion in property construction. Supply should lift as winter and power shutdowns ease into mid-2022 and as industry catches up on new capacity development post Covid disruptions. Prices rarely lift sustainably with such fundamentals, and we expect key commodities, including iron ore, met coal, copper and nickel, to trade down and closer to cost support in 2022.