Soc Gen’s Albert Edwards with the note:

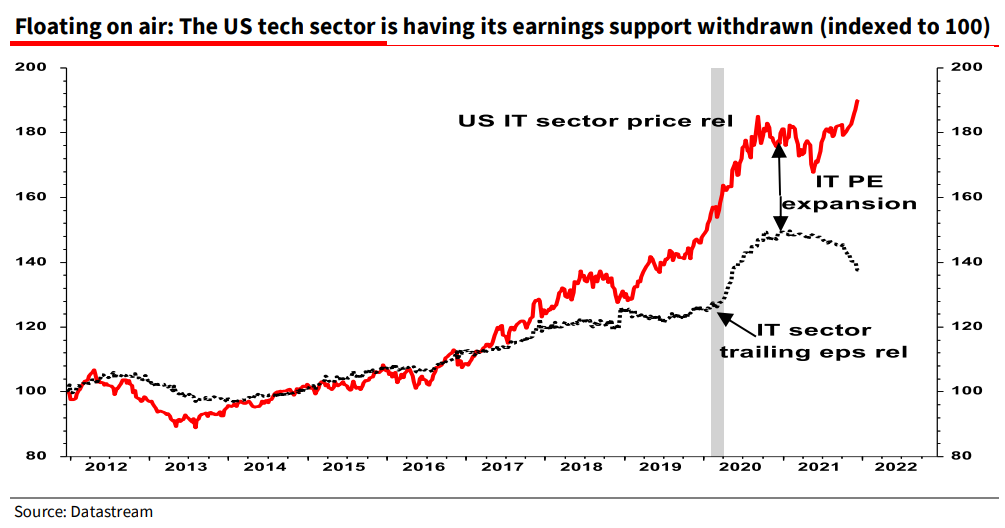

As we end the year, markets are becoming increasingly nervous that US equities – and the US tech sector specifically – are having the rug pulled out from under them. Market internals are also giving out loud warnings. Just as in 2001, could the unravelling of the recent tech bubble trigger the Vortex of Debility that destroys all before it?

Readers know I am a sort of glass half full sort of guy. This stems from my nervousness whenever I see a glass half-full after I had one smashed in my face when I was drinking in a London pub aged a mere 15. Admittedly inviting the man who was threatening me to “go ahead and see what happens”, perhaps wasn’t the wisest strategy but I was young and invincible.