The ferrous complex was weak on December 10, 2021 as spot fell, paper and steel were soft:

Westpac has a good wrap of where we are:

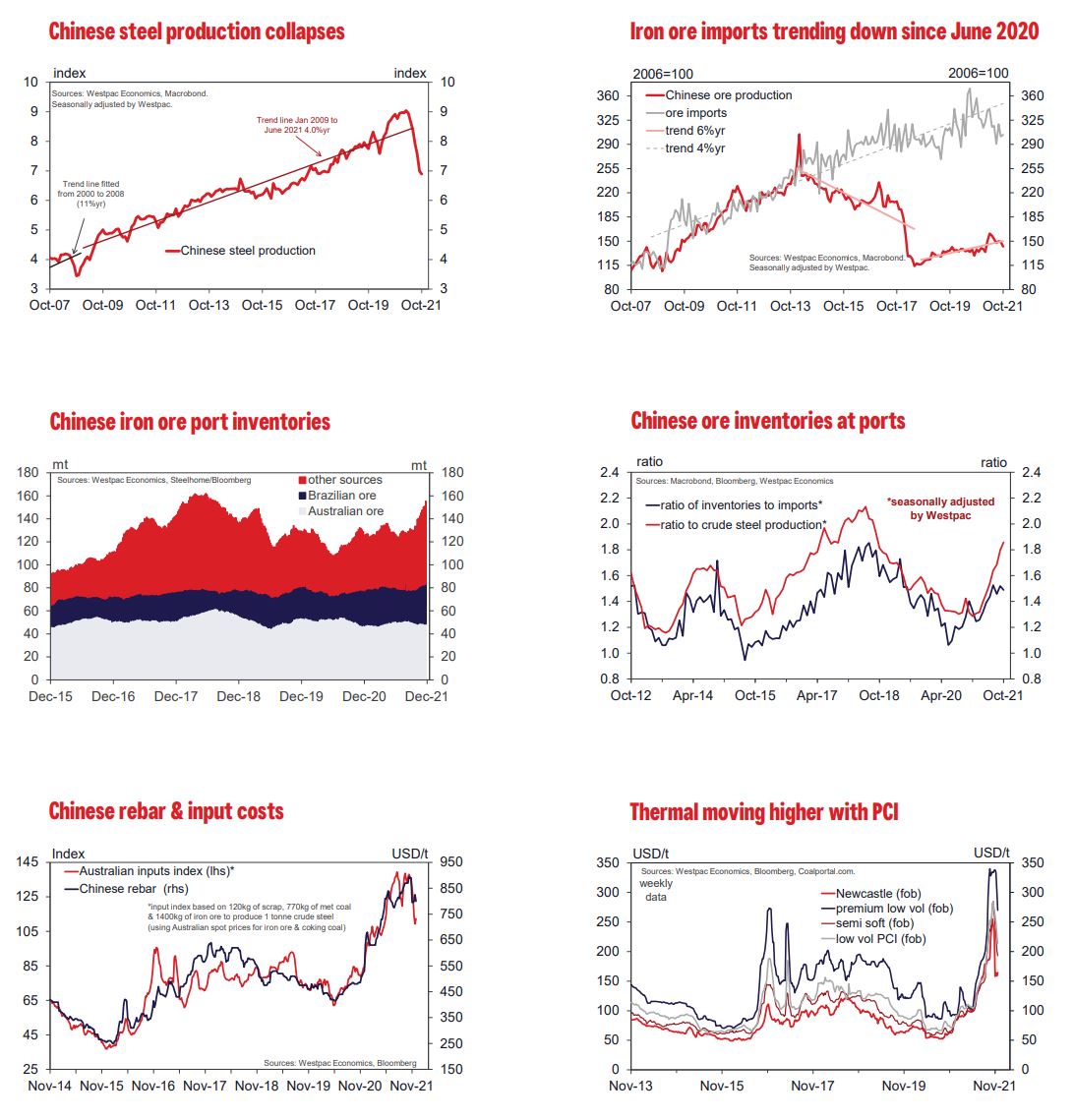

Our forecasts have iron ore drifting down to US$75/t by end 2022. You could put together a stronger argument for iron ore based on demand finding a base, PBoC stimulus backing up the administration’s call for an expansion of domestic demand including “pushing forward social housing construction”. In addition, ore supply has been trimmed with Vale, Rio, Anglo and Mineral Resources all reducing guidance in recent weeks. However, we feel it is to too early to call a base with port inventories building rapidly and prices holding above cost. While we think most of the price correction has already occurred there is still significant downside risk before there is meaningful cost support/supply discipline from the majors. The iron ore port inventories build through recent weeks is a bearish signal and they are expected to continue to lift over the next 2-3 months as pig iron production is not likely to pick up until after the Winter Olympics. This should keep pressure on iron ore prices near term. Pig iron production is down 17% in the year to October – comparable to the 16% fall recorded during the GFC. Crude steel production has gone further still, collapsing 23% in the year to October compared to a 16%yr fall during the GFC. In the last week there has been a positive sign in falling steel inventories by trader and steel mills. This may signal a marginal improvement in downstream demand. However, with current inventory levels at a five year high it has a long way to go before it signals a tight market.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.