The ferrous complex was pretty wild on November 10, 2021 as spot tumbled but steel surged and paper gained overnight:

Here it is in black and white from Wall Street’s Goldman Sachs:

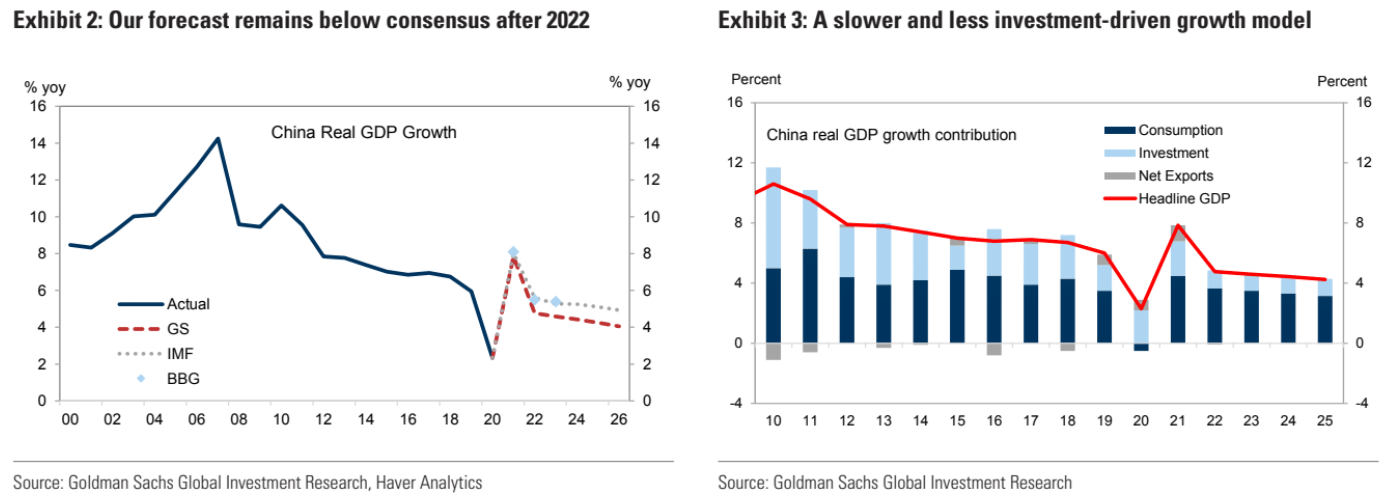

2021 has been a year of change in China, with policymakers continuing normalizing macro policies and introducing regulatory measures in numerous sectors. While we expect macro policies to ease somewhat to support growth next year, much of the structural tightening that intensified this year – especially in the property market – is here to stay, in our view. Therefore, we forecast real GDP to grow 4.8% in 2022 and expect average annual growth of only 4.5% during 2022-25, significantly below market consensus.

Although we think the odds of a housing-driven financial crisis are low in China,we believe the Chinese property market is in a multi-year slowdown. Recognizing the waning fundamental demand for housing in the coming decades, we believe policymakers are acting now to deleverage the sector and to stave off risks of a disorderly correction down the road. By our estimates, housing’s contribution to GDP growth may turn from +1pp in 2019 to -1pp in 2022-25. This is the key reason behind our below-consensus growth forecast over the next few years.

While “new infra” and “green capex” are areas where we expect strong growth for years to come, their scale is simply too small at the moment to fill the void left by slowing property investment. In addition, traditional infrastructure investment is unlikely to rebound sharply as policymakers’ deleveraging and de-risking mentality also applies to local government officials. Taken together, we expect the investment contribution to GDP growth to decline, leading gradually to a less investment-driven economy over time.

Given the upcoming Beijing Winter Olympics and the 20th Party Congress next year, we expect the Chinese government to continue its “zero Covid” policy despite a high vaccination rate and medical improvements. This suggests a continued, but gradual, recovery in household consumption next year. On the other hand, we think Chinese exports are likely to grow further in 2022, although not as fast as this year, supporting Chinese current account surplus and CNY appreciation.

The experience of the US-China trade war and the Covid pandemic have likely convinced Chinese policymakers that resilience is more important than speed whenit comes to growth. As President Xi aims to secure a third term next year, the leadership seems to be taking an even longer-term view on development than before. With this backdrop, we believe the Chinese economy is settling into a new regime where policymakers accept slower growth in the near term for a more resilient economy in the long run.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.