The DXY rocket flamed out last night as EUR rebounded:

The AUD could not catch the thermal:

Oil and gold did better:

Advertisement

Base metals were mixed. They look very troubled by a rising DXY:

Big miners are sick:

Advertisement

EM stocks want to retest the lows:

Junk did better:

As yields calmed:

Advertisement

Allowing, you guessed it, GAMMA to rise:

Westpac has the wrap:

Event Wrap

US weekly initial jobless claims were close to consensus, with initial claims of 268k (est. 260k) and continuing claims of 2.08m (est. 2.12m). The US leading index for October was firm, rising 0.9% (est. 0.8%). The Philadelphia Fed business outlook survey was strong, jumping to 39.0 (est. 24.0, prior 23.8), driven by higher prices (prices paid rose to equal the recent record high, prices received rose to the highest since 1974), new orders rising, and the average workweek rising. The accompanying commentary referred to an economy that “continues to overheat”. In contrast, the Kansas Fed manufacturing survey fell to 24 (est. 28, prior 31), with a sharp pullback in new orders to -4 from +27. Prices paid fell but remained high.

FOMC member Williams sounded less comfortable about medium term inflation pressures, citing a roaring economy and falling jobless rate, while maintaining that pandemic impacts remain at play.

Event Outlook

Japan: The CPI should remain weak in October despite global inflationary pressures (market f/c: 0.2%).

UK: GfK consumer sentiment for November will be hurt by rising prices and ongoing delta concerns, but should remain well above the lows of 2020.October’s retail sales growth is expected to modest given strengthening demand for services at the expense of goods (market f/c: 0.5%).

US: The FOMC’s Clarida will speak on global monetary policy coordination; Waller will discuss the economic outlook.

The rising DXY is now the only story in town. As we have discussed all year on our podcasts, it doesn’t take long for a rising DXY to punch big holes in EM capital flows and commodity prices. Indeed, each time we have seen DXY shift into the cyclical bull phase over the past several cycles, it has blown up the EM complex quick smart and forced all kinds of central banking backflips, most notably in early 2016 and again in late 2018.

Advertisement

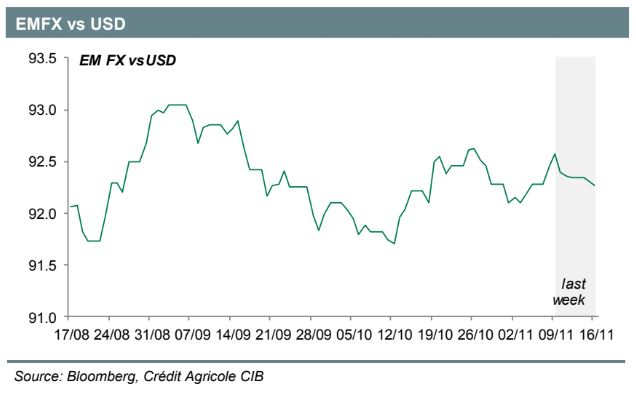

2022 shapes as a similar dynamic. Credit Agricole:

The global backdrop remains marked by expectations of rate hikes in developed economies, and particularly in the US. The announcement of the tapering, followed by the strong USCPI release last week, has confirmed this perspective. Yesterday, the release of a stronger-than-expected retail sales number in October (as well as stronger-than-expected import prices) has added to the narrative. In itself, the normalisation of global monetary policies should make the life of EMs more difficult. However, it is interesting to note that the recent downward correction of EMFX vs the USD actually reflects the strengthening of the USD itself, more than EMs’ intrinsic weakness (with the exception of the most vulnerable EM currencies, such as the TRY for instance). Our EM FX index has depreciated by-1.0% since peaking on 9 November. The USDindex(DXY) has strengthened by 1.8% during the same period. EMFX has actually strengthened vs the EUR.

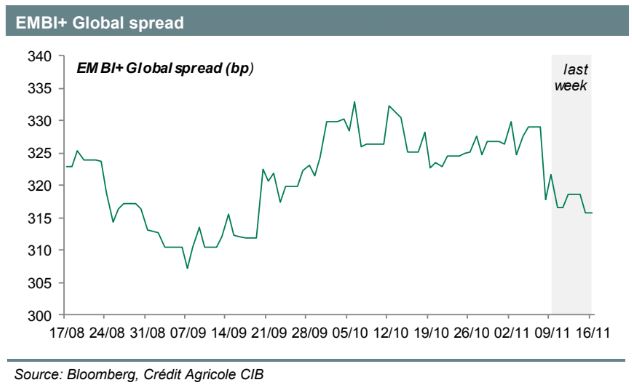

By the same token, the EMBI + sovereign spread index has remained contained in the past few days, suggesting the perception of overall EM risk has not overly deteriorated.

The are a real so some more supporting factors. One of them is the resumption of the dialogue between Presidents Jo Biden and Xi Jinping, even though the bilateral talks have not led to concrete measures. Another factor is the slightly stronger Chinese data pack released at the beginning of the week (although, in our view, the growth of China’s final domestic demand remains fragile). Our view remains that the normalisation of US monetary policy should not lead to a shorting of EM currencies across the board, but to careful picking among them. For instance, even if the TRY remains costly to short, we expect some further possible weakness. The ZAR is also vulnerable if the SARB does not hike rates on Thursday, as the consensus expects. By contrast, in our view the RUB should be less risky at the current level.

It’s early days for DXY. As commodities start falling then the EM pressure will ramp up.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.