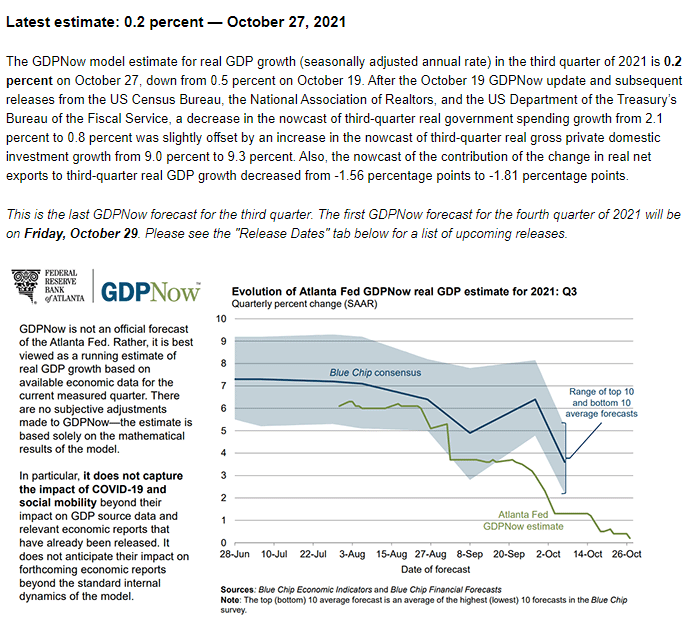

Hard to believe, I know. It was only a few months ago that we were all celebrating the boom of a lifetime but that’s how fast things can turn in the COVID environment.

The Fed’s GDPNow measure is almost in contraction now:

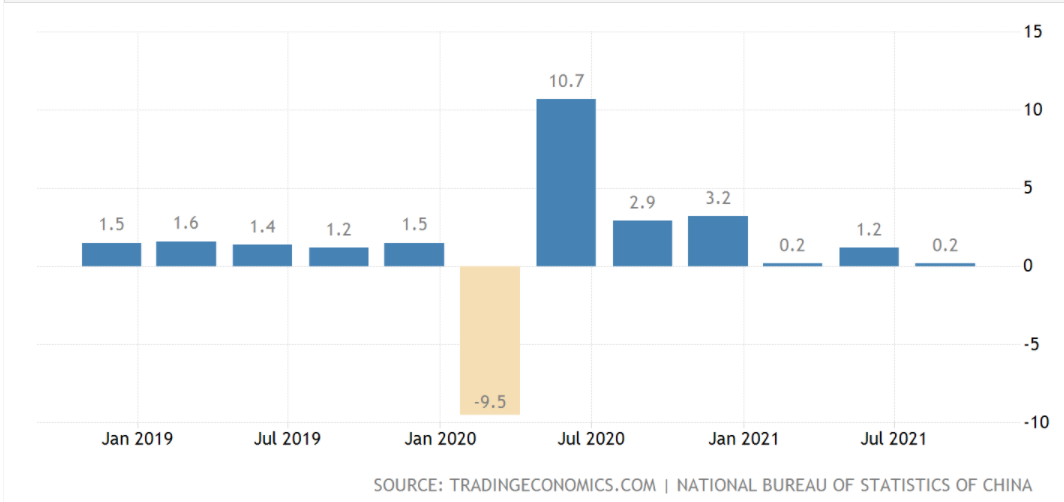

As we know, China is already at 0.2% as well:

Advertisement