Nordea with a snippet:

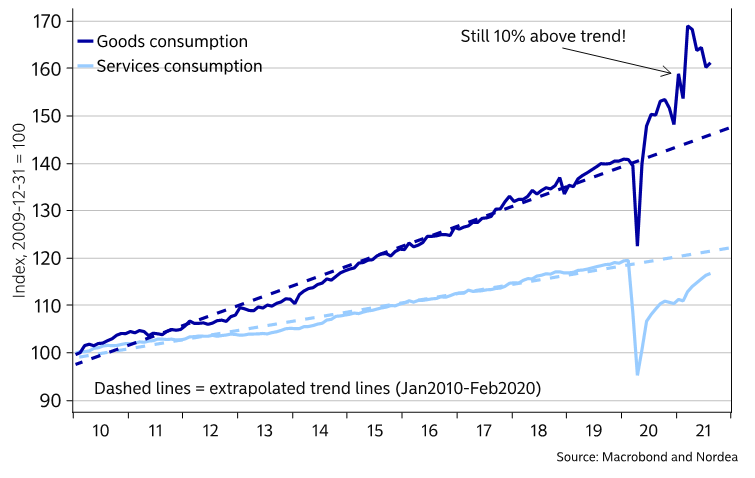

One likely underappreciated driver of so-called supply chain issues stem from demand-side issues. The initial shock from the pandemic depressed demand both for goods and services. However, already by June 2020 US goods consumption had surged way above trend. If you can’t consume services as you’re locked into your apartment – of course goods consumption will surge. This nonetheless caught goods-producing companies off guard since they plan for trend growth in demand, and this has not only exacerbated various shortages but also led to greater CPI “inflation” as goods prices are more flexible than service prices.

Chart 2: Composition of demand still out of whack