The Chinese energy crisis is cooked. Put a fork in it:

On Friday, the NDRC said it held a meeting with large state-run companies including oil refiner Sinopec, aluminium giant Chinalco and steelmaker China Baowu on “rational” energy usage by industry on Thursday and said they should take the lead in energy-saving and carbon reduction.

The NDRC “has concluded that the unbridled soaring of coal prices is partly driven by those hoping to hit the jackpot by taking advantage of the power supply falling short of actual need”, Chinese state media outlet China Daily wrote on Thursday.

There should be “zero tolerance to the hoarding of coal”, the newspaper added. “It is of the utmost importance to rein in coal prices as they will pose a threat to people’s daily lives when winter sets in.”

China’s coal output is rising after some 153 mines received approvals to expand capacity. As of this week, daily production rose 4 per cent from a month ago to 11.6 million tonnes.

China’s second-biggest mining region, Inner Mongolia, expects its 2021 coal production to exceed 1.05 billion tonnes, state media Workers’ Daily reported, citing an Inner Mongolia conference. This would be up from 1 billion in 2020, according to National Bureau of Statistics data.

However, power plants are still facing difficulties in replenishing stocks ahead of winter demand. Average coal stocks at key Chinese power plants this week stood at less than 80% of the level last year, data from China Coal Transportation and Distribution Association shows.

Coal imports have also been tepid since Wednesday as sellers and buyers wait to see the full impact of Beijing’s policies, traders said.

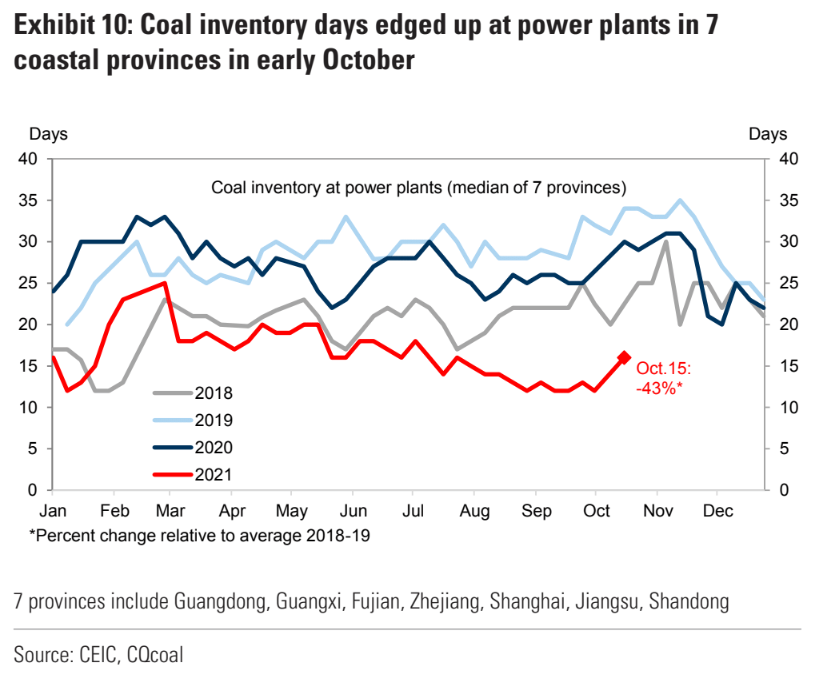

Coal inventories are still low but are rising at a good clip:

Advertisement

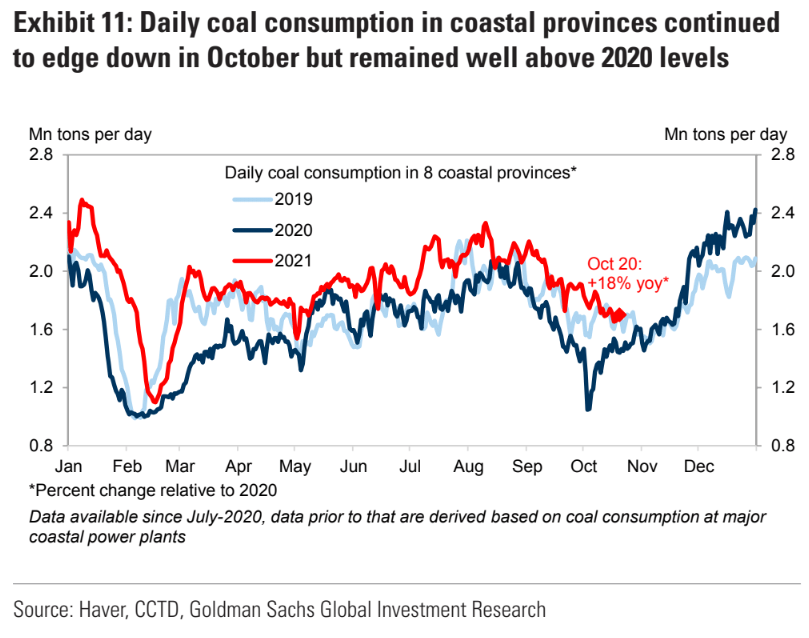

Coal usage is well down from earlier in the year:

Inventories need to be rebuilt so there are still weather risks for price spikes. Probably a bit longer for similar in India. But the crisis is over and solutions are here:

Advertisement

“We’re now seeing the fruits of China’s supply response, as the government has given miners carte blanche to produce at full tilt – even permitting the relaxation of safety inspections in some cases,” said Atilla Widnell, managing director at Navigate Commodities in Singapore.

Front end thermal coal managed a rebound on Friday night but the tail is now a bust:

Advertisement

Expect the entire thermal coal price deck to keep falling (with weather exceptions). China’s new energy security imperative means a coal glut will be upon us in months.

Coking coal also managed a small bounce Friday night after its daily evisceration:

Advertisement

Chinese steel output is down 25% from the peak. That’s 190mt less coking coal needed from May, three-quarters of the total seaborne market. This enormous fall in volume has been reduced in the short-term by Chinese power cuts knocking out 120mt of EAF scrap steel production but as that comes back with crashing thermal coal and power prices, the glut for coking coal becomes mindboggling.

Prices will doubtless flop around for a while as the usual coked-up traders, but the energy crisis is for all intents and purposes over in China. There is no ESG constraint for an angry CCP.

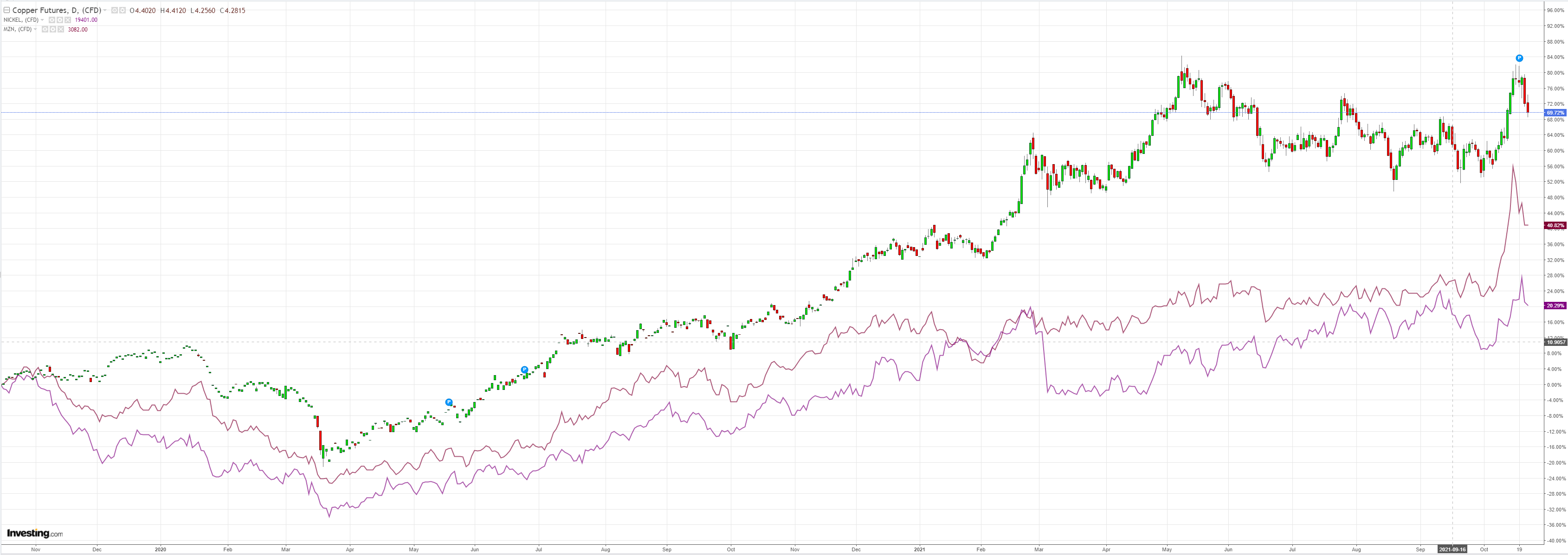

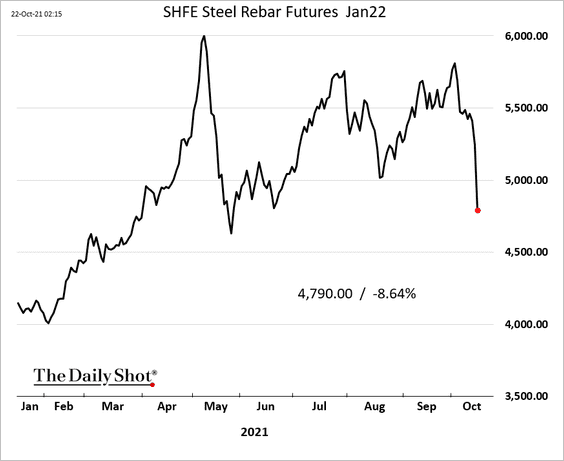

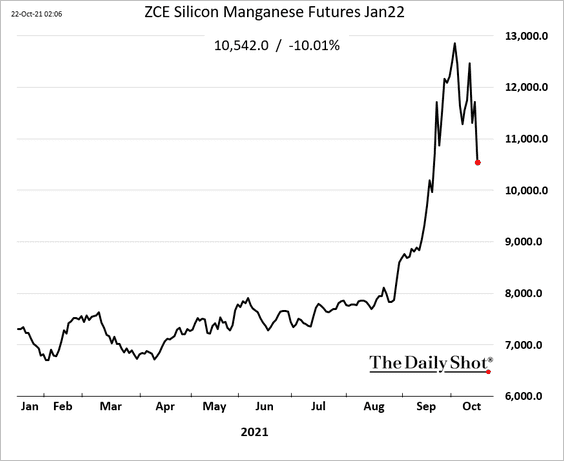

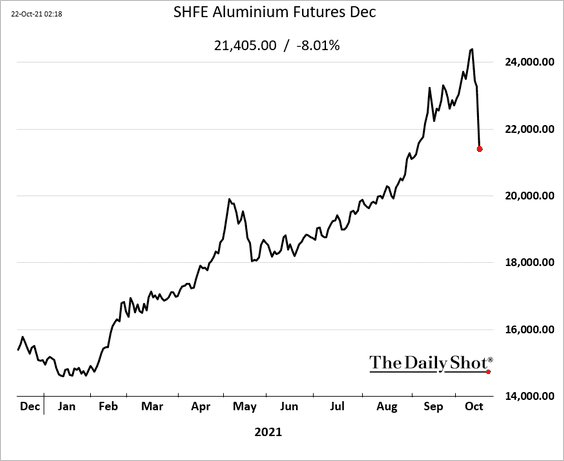

Markets are now pricing the return of Chinese metals processing:

Advertisement

I expect a complete unwind of 2021 bubble prices across the metals complex over the next year.

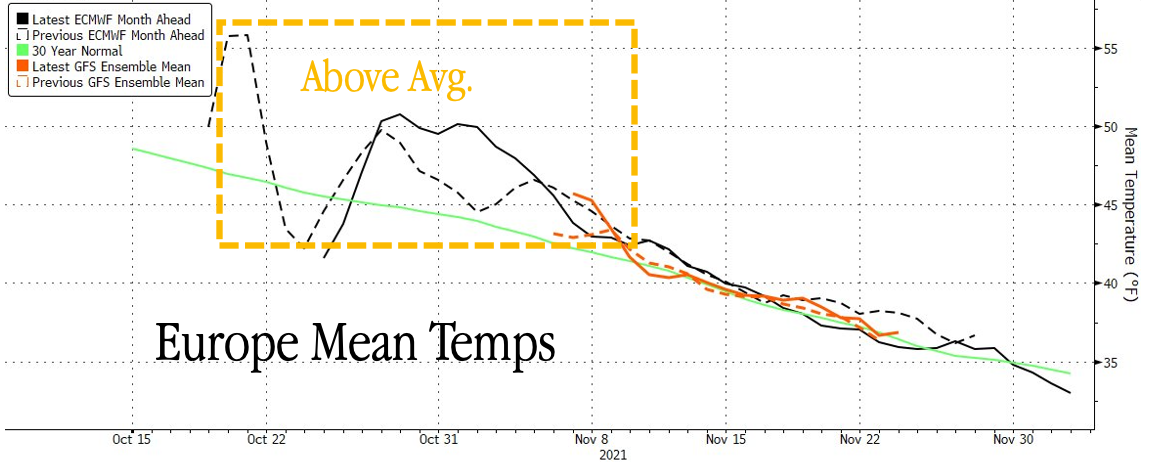

Gas has not made as much progress yet. Its shortage persists and the politics continue as Ukraine offered to discount the transit of Russian gas to Europe. The weather outlook is mixed:

Advertisement

“The main driver that will decide if storage levels will be depleted by during or even before peak winter season, and if there will be further price spikes, is the weather,” Michel Salden, head of commodities at Vontobel said.

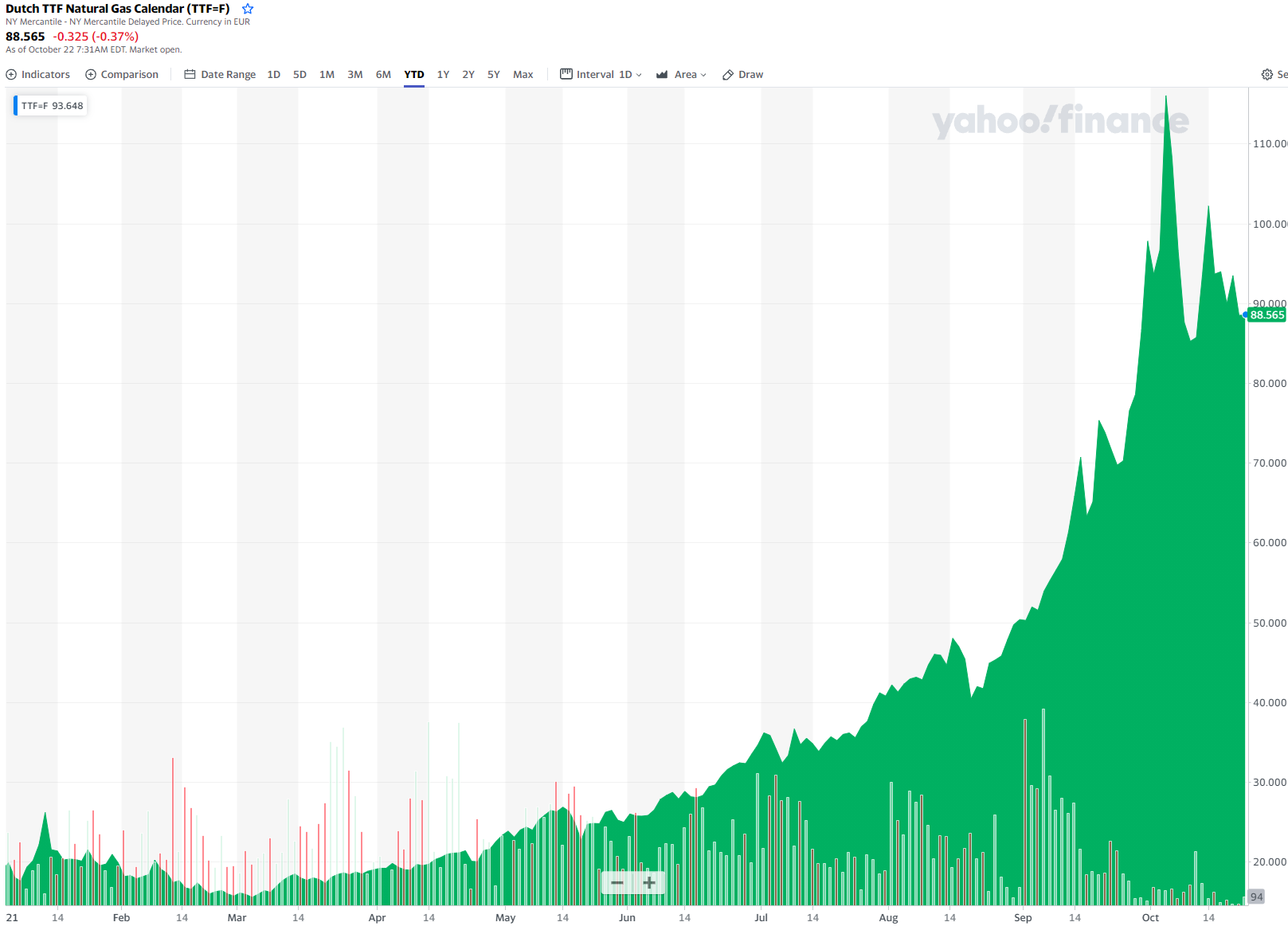

TTF eased a bit:

LNG spot was down Asia last week to $34 and change. We await whatever deal that Europe will do with Russia to keep warm.

Advertisement

All energy prices are going to crash back to normalcy over the next two quarters as the inventory crisis ends, the Chinese economy stalls, global economy slows, supply side pressures ease, plus the Fed tapers.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.