There’s not much point repeating a couple of good posts from ZH on the China property situation given they capture my thoughts so here they are. First up, the Chinese property crash is getting worse fast:

Having already suffered the fastest drop on record, Chinese junk bond markets – where property developer issuers dominate – were routed once again as fears about fast-spreading contagion in the $5 trillion sector, which drives a sizable chunk of the Chinese economy, continued to savage sentiment. Meanwhile, China Evergrande Group’s offshore bondholders still had not received interest payment by a Monday deadline Asia time, Reuters reported citing sources.

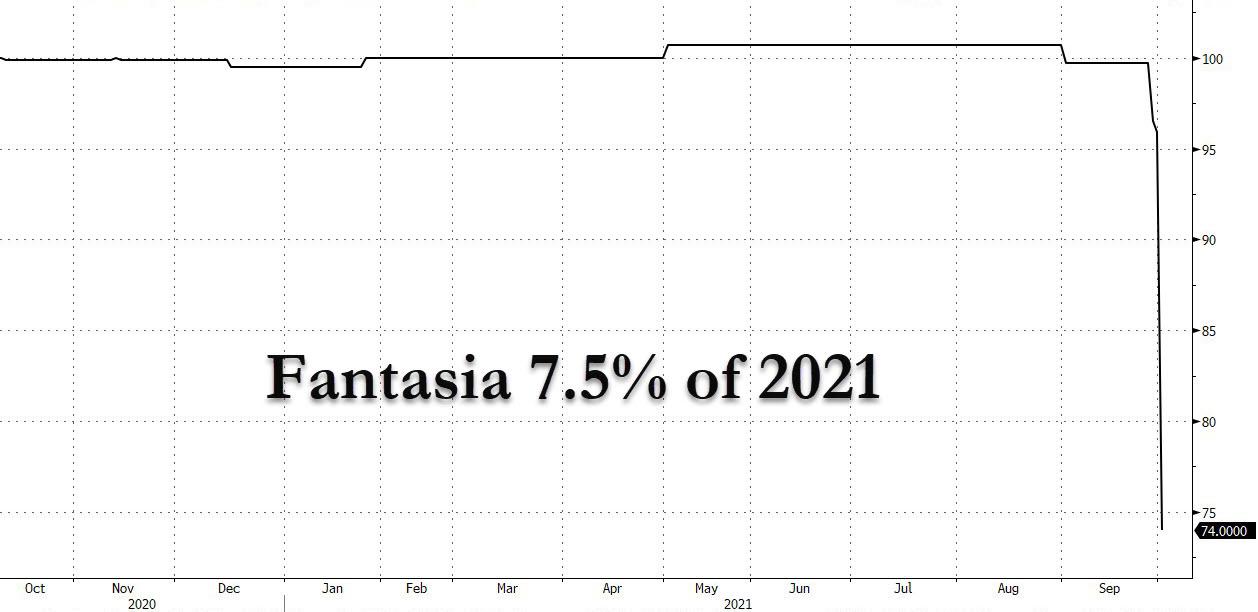

But while Evergrande’s default is now just semantics, and one week after Fantasia shocked bondholders with a surprise announcement it too would stuff creditors just weeks after it had said its liquidity was fine, which sent its bond plunging from par to 74 cents in seconds…

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.