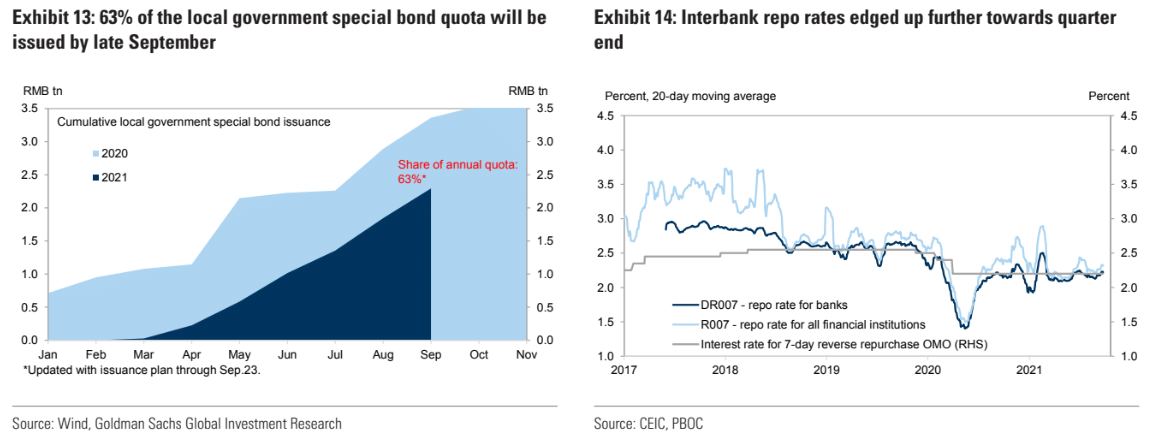

For much of this year, we have heard the bullish narrative from China watchers that any property development slowdown will be offset by increasing infrastructure spending. That has not played out at all. Indeed, infrastructure has collapsed almost as fast as property investment with funding down some 37% year to date:

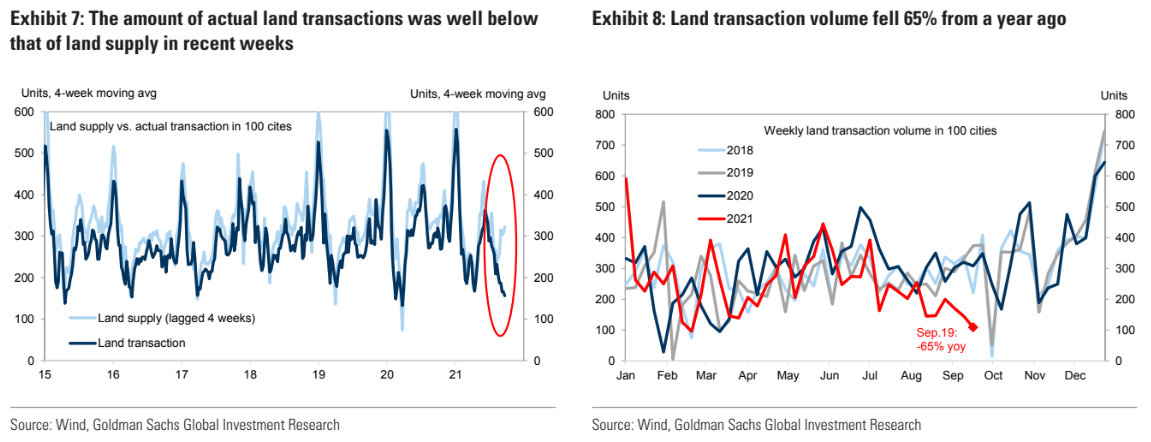

This is no surprise. Infrastructure development in China is very much a local government responsibility and as property developers have been hammered by credit markets, they have been unable to finance land purchases, a key component of local government revenues:

Advertisement

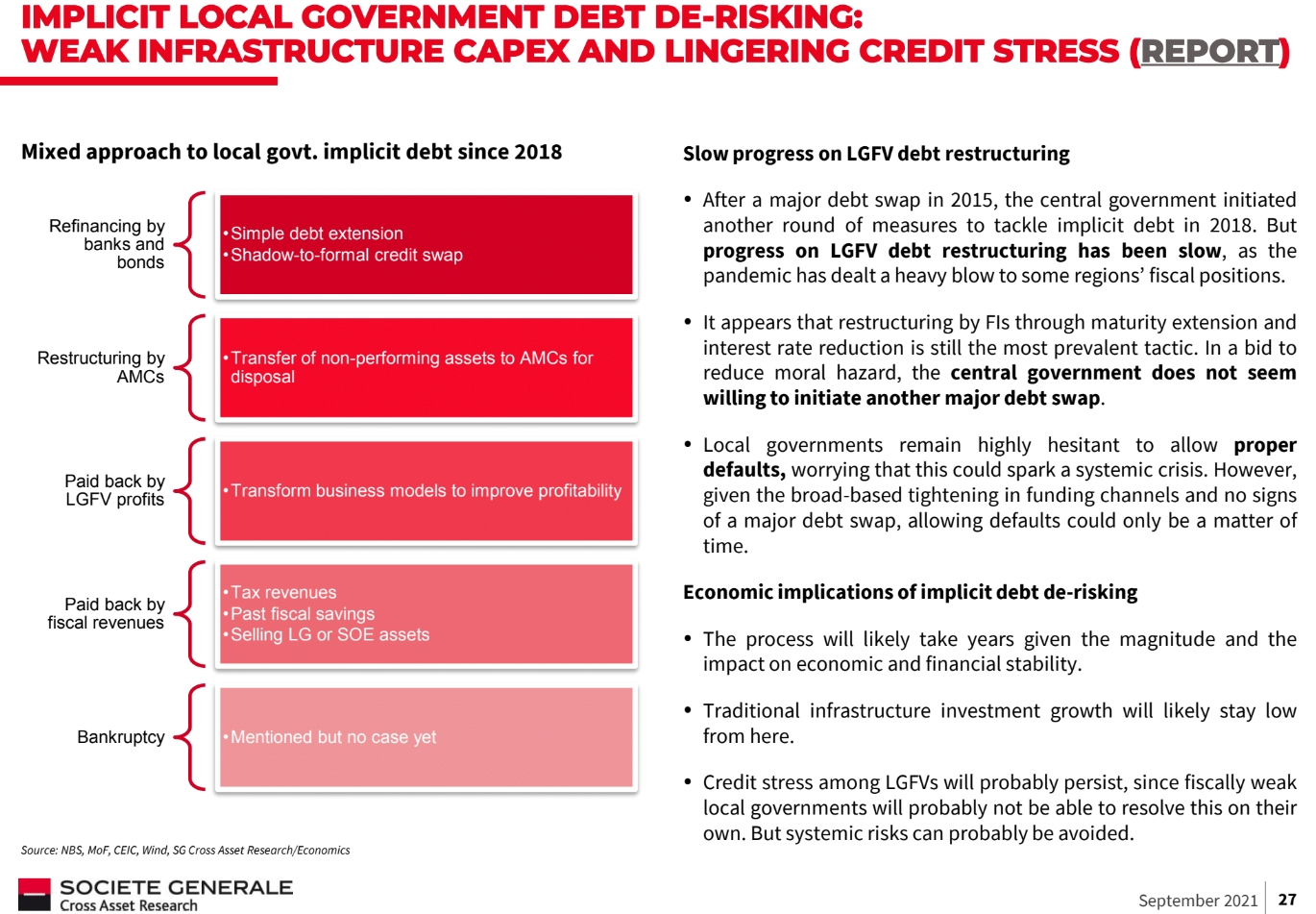

But there is another headwind. Beijing’s deleveraging program has set up some very confusing incentives for local governments. Societe General with the note: