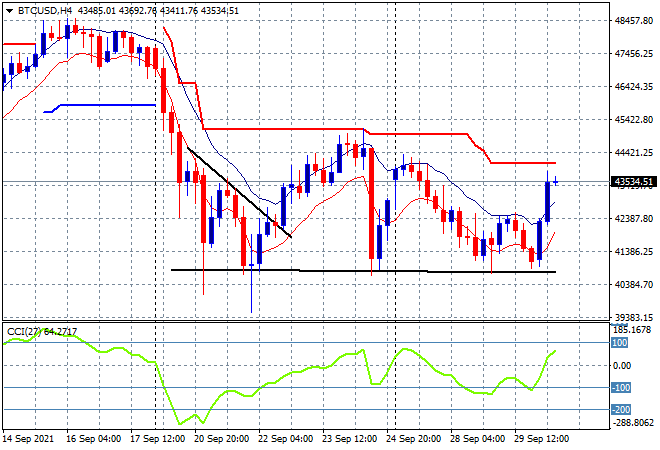

Asian stocks are trying to bounceback after the sharp selloffs on Wall Street but also the growing economic palava in China with the recent volatile moves in iron ore and Evergrande still dominating changes in sentiment. The USD remains very firm against most of the risk currencies as the Australian dollar again tries in vain to make a comeback, gold is still under enormous pressure after making a new monthly low. Meanwhile Bitcoin is trying to bounce off its recent lows at the $40K level, heading through the $43K level but coming up against staunch and nearly week long resistance as it fails to make a new intraweek session high:

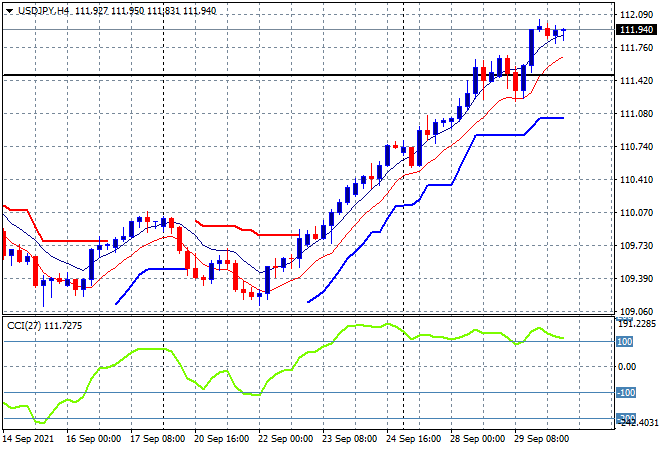

The Shanghai Composite is loving the PBOC shenigans, lifting strongly going into the close to be up nearly 1% to 3568 points while the Hang Seng Index is being quite neutral, unchanged at 24638 points. Meanwhile Japanese markets continue to pull back, with the Nikkei 225 closing 0.3% lower at 29454 points despite Yen selling off as the USDJPY pair rises up against natural resistance at the 112 handle:

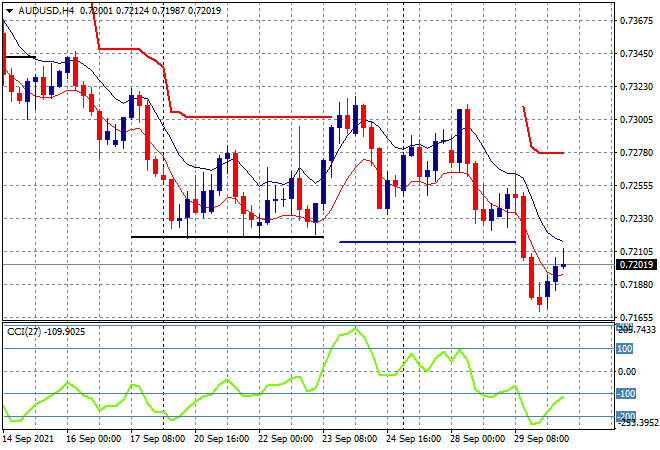

Australian stocks finally saw some relief, moving sharply in line with iron ore fortunes and ignoring the rampant Victorian COVID breakout with the ASX200 jumping nearly 2% to finish at 7332 points, staving a wider selloff. The Australian dollar however is really struggling even though it has managed to lift through the 72 handle, resistance is clearly too strong overhead here after recently putting in a new weekly low:

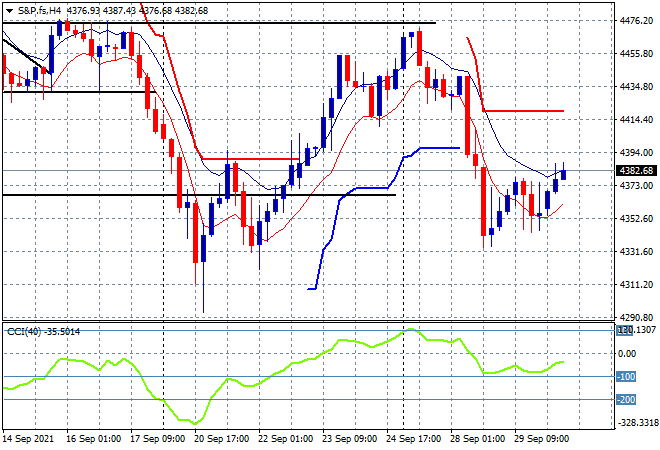

Eurostoxx and S&P futures are up 0.4% and 0.6% respectively or so going into the London open, with the four hourly chart of the S&P500 showing price trying to bounce back from this latest dip-rection (bigger than a dip, not quite a correction – call it a semi). As price never made a new weekly low, nor has momentum been oversold, there is growing potential here for a solid short term swing with the 4400 point level proving the next target, but also steady resistance:

The economic calendar is jam packed tonight with some serious releases, first German (and hence Euro wide) unemployment and inflation, then UK and US GDP prints.