Unprecedented regulatory tightening in the largest asset class globally

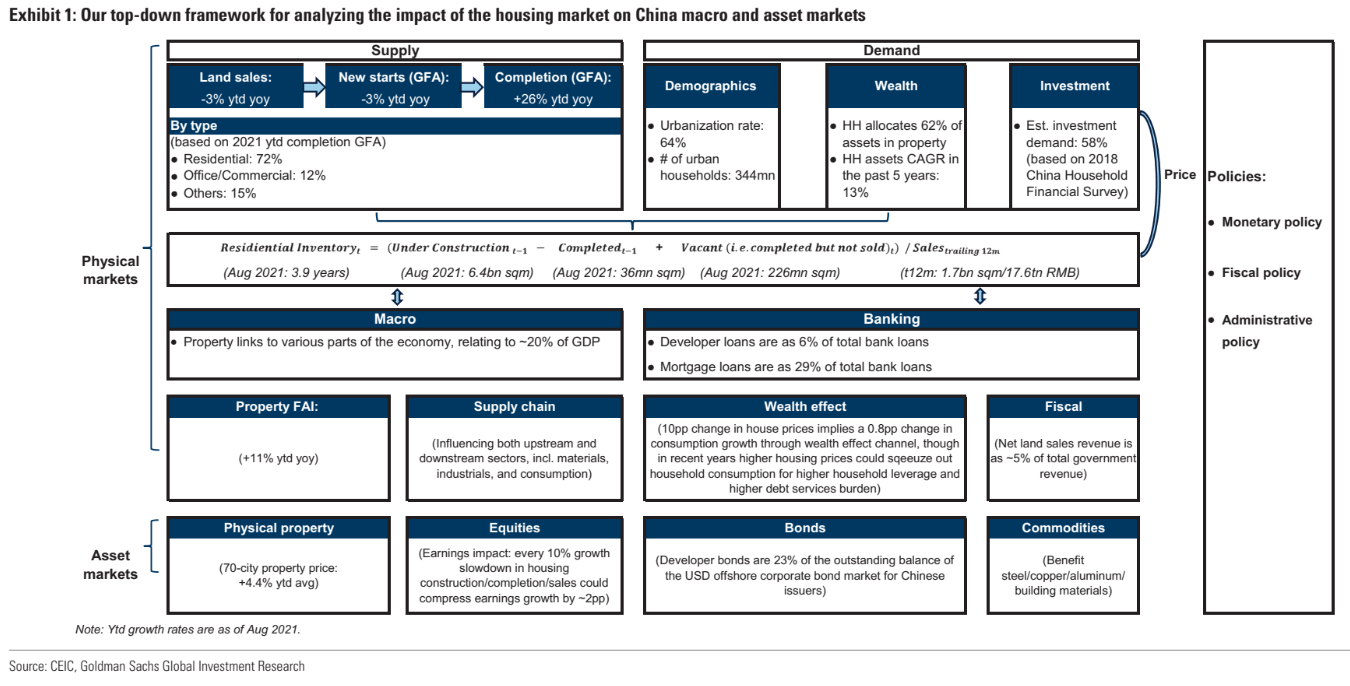

Regulatory actions in China Internet have resulted in more than US$1tn market cap loss on the tech sector since mid-Feb, but in the past two weeks, investor focus has shifted to the US$60tn China property market which is linked to ~20% of Chinese GDP and represents 62% of household wealth. More than 400 new property regulations that are largely tightening in nature have been announced ytd to restrain housing market activity, spanning supply, demand, funding, leverage, to price control measures.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.