Goldman with the note.

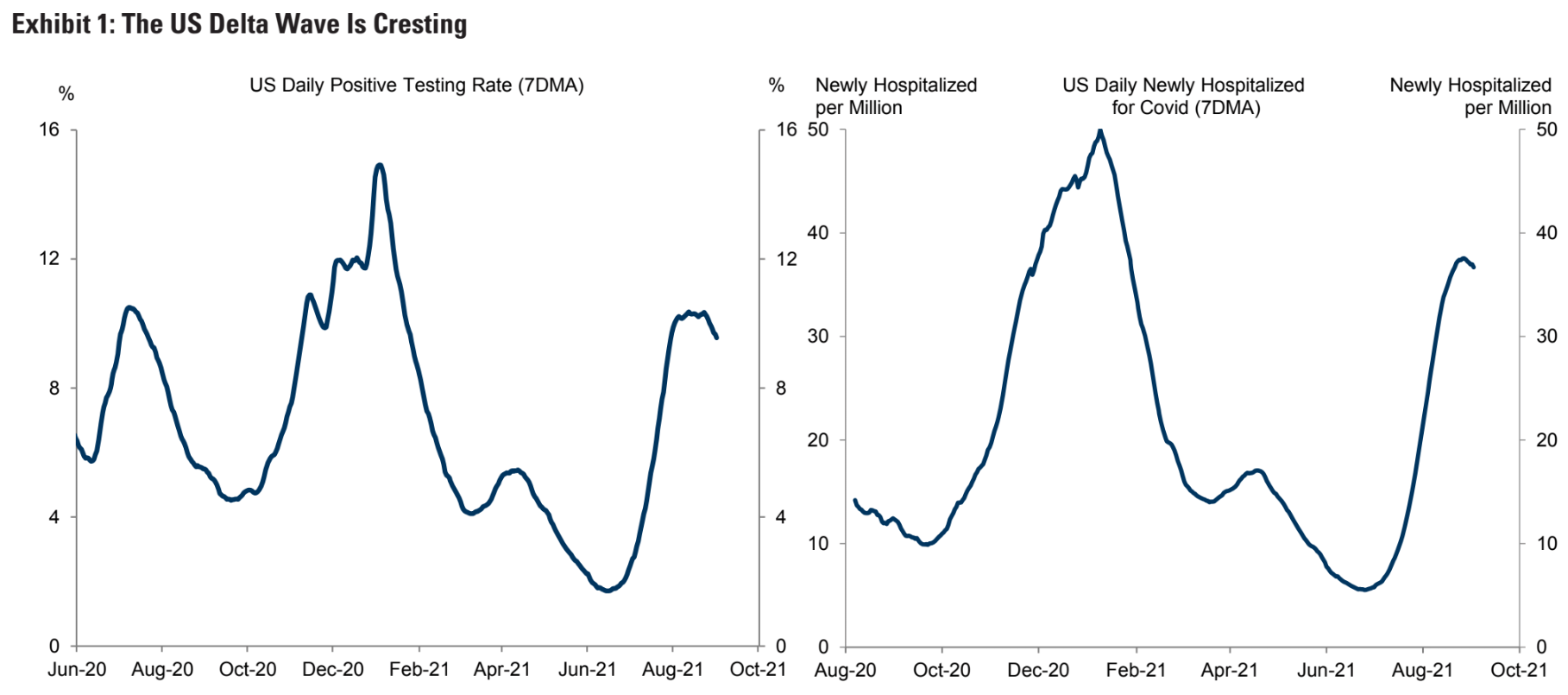

There are now signs that the Delta wave is cresting, with a drop in the positivity rate over the last couple of weeks and a more recent decline in new hospital admissions.

We therefore expect a job market rebound in coming months and have also offset part of the Q3/Q4 GDP downgrade with stronger numbers in the first half of 2022.