Thermal coal and LNG futures both came off overnight. The former:

The latter:

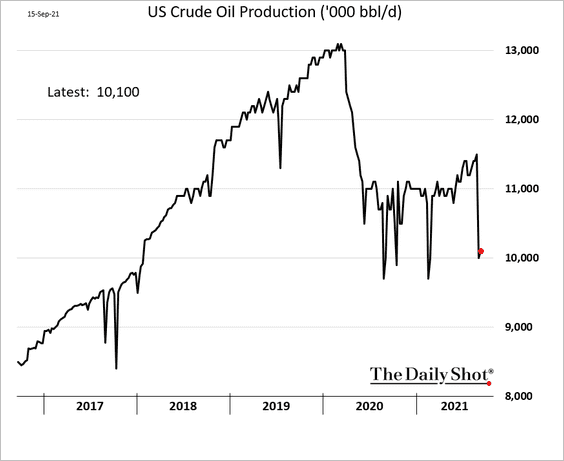

Oil was still strong as we await the return of hurricane shuttered US production:

Advertisement

Thermal coal and LNG futures both came off overnight. The former:

The latter:

Oil was still strong as we await the return of hurricane shuttered US production:

The full text of this article is available to MacroBusiness subscribers