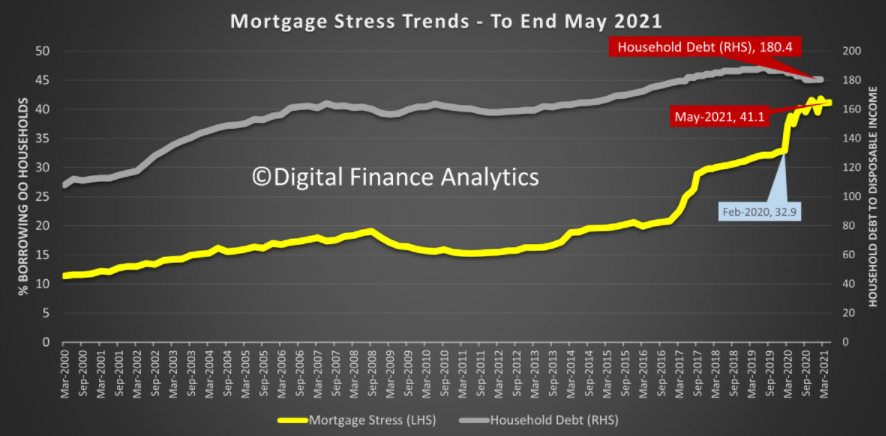

Digital Finance Analytics (DFA) has released its mortgage stress figures for May, which shows that around 41% of households remained ‘mortgage stressed’, up significantly from the pre-pandemic level of 32.9%:

Mortgage stress has risen massively during the pandemic.

Martin North explains the rise in mortgage stress as follows:

Our approach to measuring stress is unique in that we examine household cash flow – money in and money out. Given that many households saved hard last year though the heights of COVID, it is not surprising to see many now draining down those savings, by spending more. This means that their cash flow will in net terms be negative for now, and so will register as stressed. That said, if spending continues unabated financial difficulties will eventuate.

In addition we continue to see more households reaching for credit (from Buy Now Pay Later, to Pay Day loans) as well as equity release from property. In fact the latest hikes in perceived values has led to a run of refinancing, to try and pay down debt, or to provide funds to offspring for property purchase via the Bank of Mum and Dad. Again these one-off moves can adversely impact household stress measures in our methodology.

And we also note that many prefer not to accept the truth that some households are not home and clear in terms of their finances, given the uncertain part-time work, multiple jobs and zero hours contracts which many are on. But we continue to analyze households in net cash flow terms. If more funds drain away, compared with income, they are classified as stressed.

As I have noted previously, the increase in mortgage stress during the pandemic does not gel with the macroeconomic data and seems implausible.

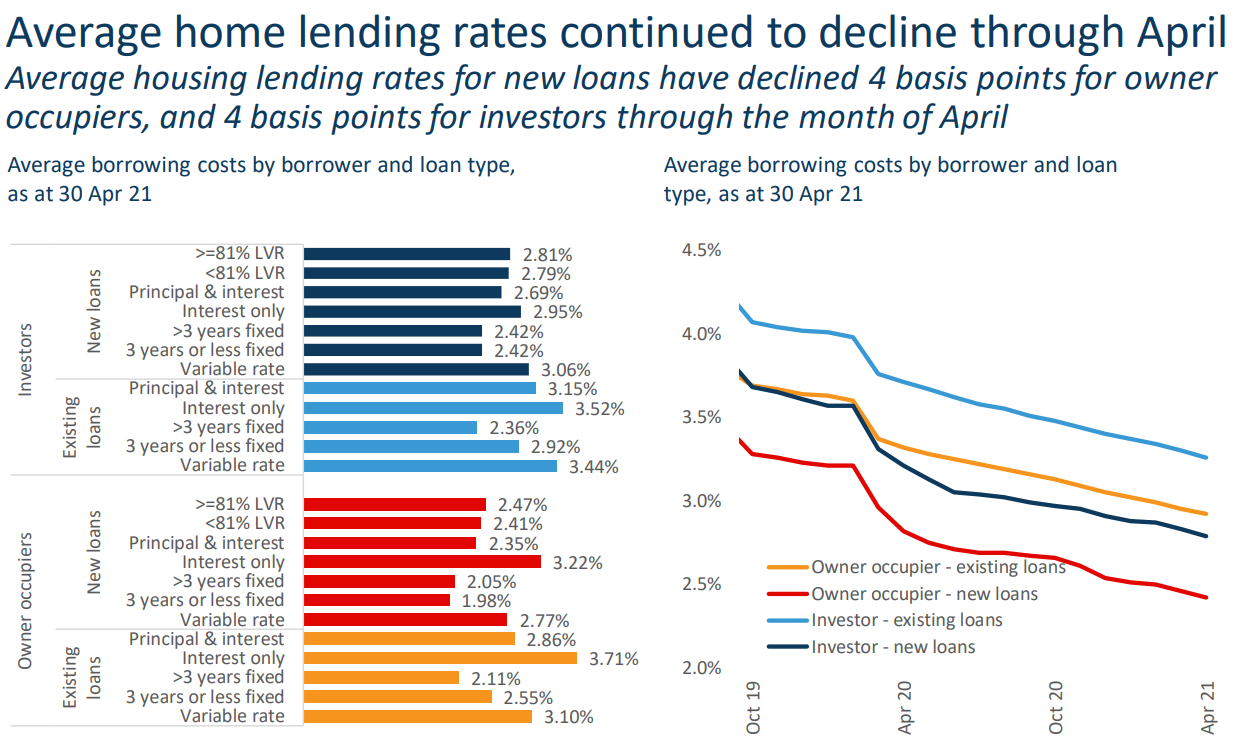

First, mortgage rates have tanked, as illustrated clearly in the next chart from CoreLogic:

Average mortgage rates down sharply since start of pandemic.

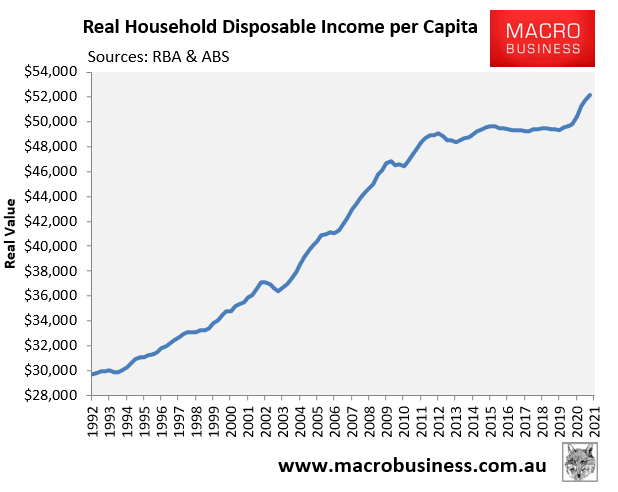

Second, household disposable income has risen sharply on the back of massive stimulus, experiencing its strongest annual rise since 2008:

Real per capita household disposable income has broken a decade of stagnation.

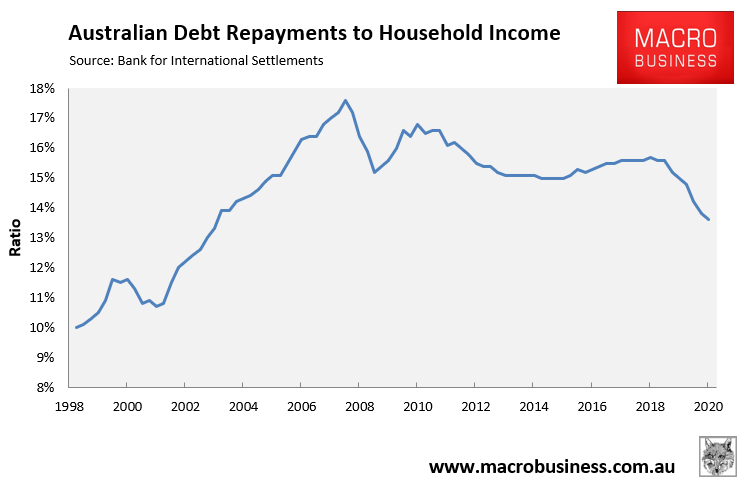

Third, The ratio of debt repayments – both principal and interest – to household disposable income has fallen to a 17 year low, according to the Bank for International Settlements:

Australian household debt repayments have fallen to a 17 year low compared to disposable income.

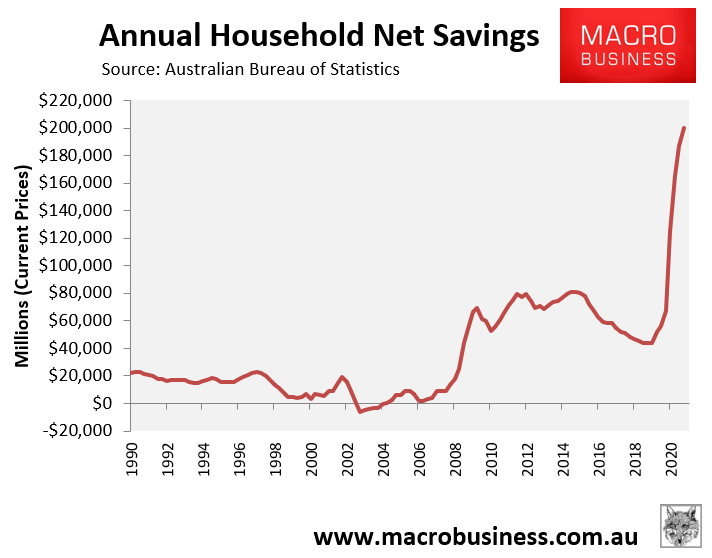

Finally, Australian households have built up a massive war chest of savings, which augers against the ‘mortgage stressed’ theme:

Australian households saved a record $200 billion in the year to March 2021.

According to the above explanation by Martin North, DFA’s mortgage stress data measures “household cash flow – money in and money out”. So, “given that many households saved hard last year though the heights of COVID”, shouldn’t stress levels have fallen, since more money was coming in than out? Instead, mortgage stress rose significantly by around 8%.

What am I missing here?