The Reserve Bank of Australia (RBA) has released its June Bulletin, which includes an interesting report on the unprecedented stimulus undertaken by the world’s economies.

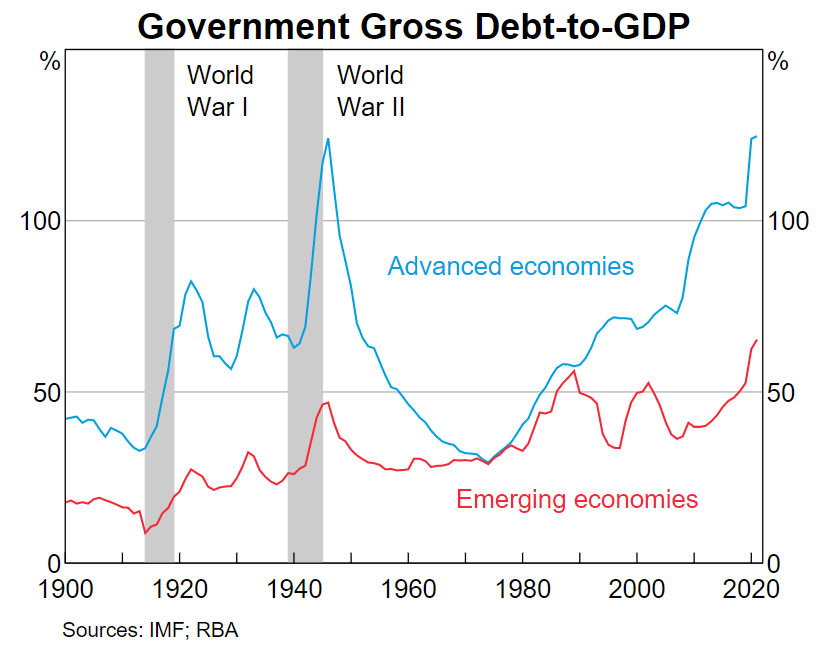

The first chart below shows the ramp-up in debt across advanced and emerging economies, which was driven higher by pandemic stimulus:

These direct measures, including those that are expected to persist into early 2022, have ranged from 5 to 24 per cent of 2019 GDP in advanced economies. Authorities in emerging market economies have provided smaller, yet still significant, direct fiscal support which has been equivalent to between 1 and 9 per cent of GDP (IMF 2021). For many economies, this has contributed to the largest single-year increase in the government debt-to-GDP ratio during peacetime…

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.