Yesterday, Treasurer Josh Frydenberg defended the Coalition’s proposed wind back of responsible lending laws, telling reporters they are essential to helping the economy recover from COVID:

“Ensuring consumers and small businesses can get timely access to credit as the economy continues to recover from the COVID crisis”.

“The reforms are intended to improve efficiency, reducing the time and cost associated with the provision of credit for consumers and small businesses”.

The Treasurer’s defence comes after 33,000 Australians and 125 community groups recently signed an open letter against the reforms.

The Hayne Banking Royal Commission’s very first recommendation was to maintain these responsible lending laws, which came after observing multiple cases of predatory lending over its 12 month deliberation:

Source: Hayne Banking Royal Commission Final Report.

Now the Greens are trying to kill the reforms once and for all by forcing a deciding vote in the Senate, which is likely to block the legislation:

Greens senator Nick McKim will move a motion on Monday to get the planned changes knocked off the notice paper unless it is taken to a vote by the end of the week…

Senator McKim is working on getting enough support from Labor and the crossbench to wedge the government into bringing the bill on this week.

One Nation leader Pauline Hanson has been a vocal critic of winding back the laws. Senator Jacqui Lambie is also reportedly opposed and Senator Rex Patrick has pointed to the lending data as an indication the repeal of the laws may be unnecessary.

The Fact Sheet supporting the legislation claimed the responsible lending reforms were restricting the flow of credit:

The importance of credit to households and businesses makes access to credit vital to Australia’s economic success. Economic studies have consistently demonstrated a positive relationship between credit growth and economic growth, with the cost and availability of credit a strong determinant of credit growth.

Credit underpins the Australian dream of home ownership…

Now, more than ever, it is important that there are no unnecessary barriers to the flow of credit to households and business, especially small and medium sized businesses, as the economy recovers…

As the Governor of the Reserve Bank of Australia observed recently, what began as responsible lending principles has translated into a practice that has become imbalanced between a lender and its customer, leading to the undesirable consequence of unduly restricting lending.

Yet, when questioned about the effects of the responsible lending laws on in Senate estimates this month, ASIC Commissioner Sean Hughes said it was “yet to see any empirical evidence that responsible lending has impeded the flow of credit to consumers”.

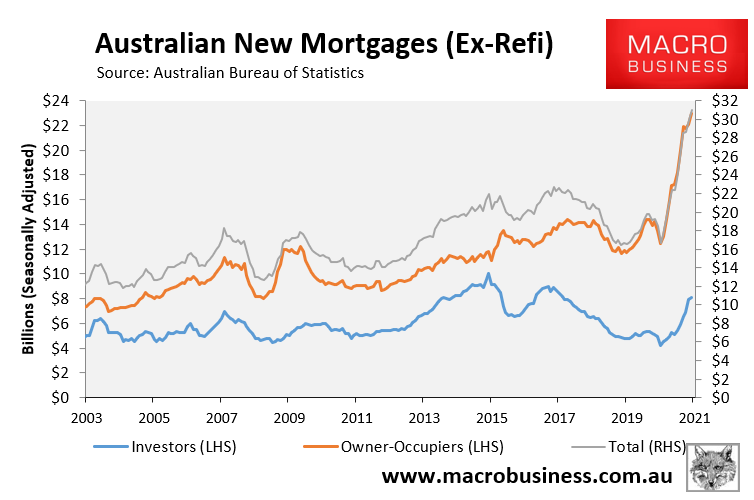

Thus, the entire justification for axing responsible lending obligations has evaporated. Australia’s mortgage market is experiencing its biggest ever boom, which is bonafide evidence that restrictive credit is not an issue:

A fresh record high in new mortgage commitments.

Australia’s financial regulators are also becoming increasingly concerned about the explosive growth in mortgages, as stated by RBA Governor Phil Lowe on Thursday.

Therefore, removing responsible lending obligations would work at cross-purposes and risks APRA responding sooner with macro-prudential tightening.

Josh Frydenberg should admit that he was wrong to propose the responsible lending legislation and scrap it. It doesn’t have Senate or community support anyway and is precisely the wrong reform at the wrong time.