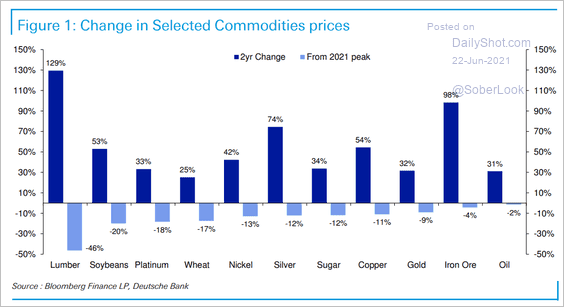

For the last few months, MB has had to battle a torrent of Wall Street (and local) drivel about a “new commodities supercycle”. This notion was never well-thought through. It mistook a global inventory supercycle for some kind of MMT supercycle. It mistook post-pandemic supply-side frictions for some kind of inflation supercycle. It mistook a bit of goods buying by DM households for Chinese stimulus. It mistook US Keynesian exceptionalism for Austrian weakness. It mistook some bad weather for the Book of Revelations.

It has been a comprehensive intellectual failure piled upon unscrupulous bubble-blowing spruik. Now it has begun the great unwind:

We are far from done here, in my view. And the slow dawning of fear is appearing in the whites of Wall Street eyes. One of the last investment banks to join the pile-on was JPM and it sounds positively jittery now:

The full text of this article is available to MacroBusiness subscribers