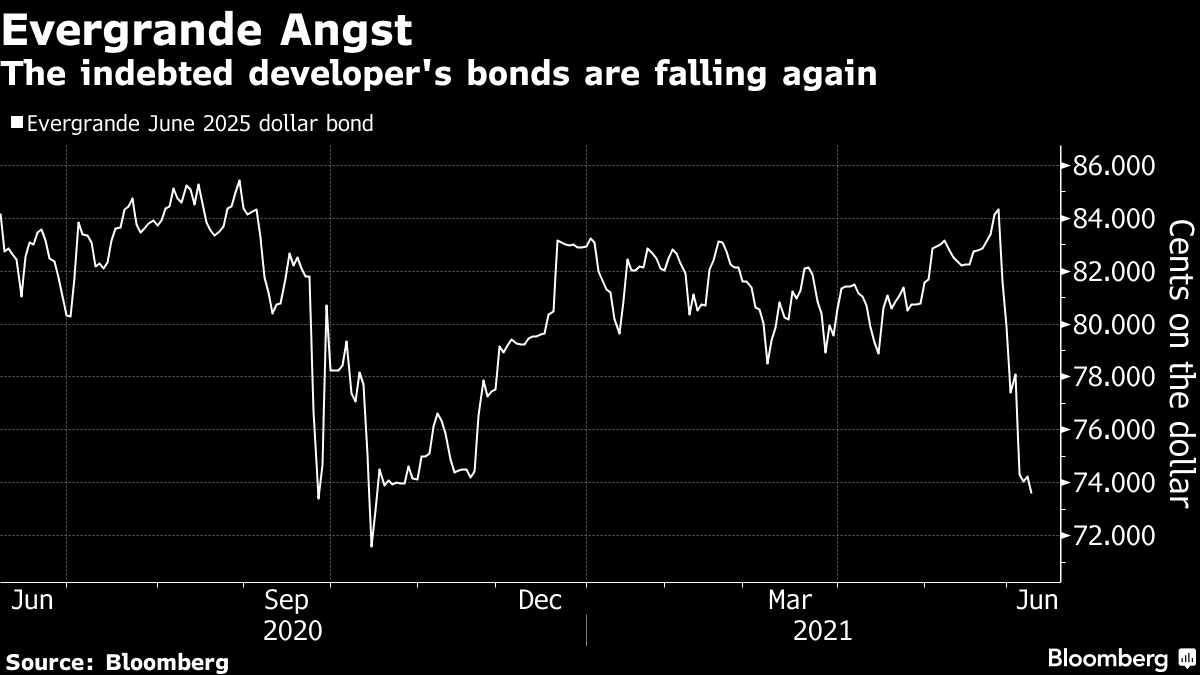

Lordy, already! A few months of three red lines policy and the titans totter. China’s largest property developer, Evergrande, is increasingly on the nose for credit markets:

And equity markets:

- Regulators have instructed Evergrande counterparties to stress test their exposures.

- Evergrande denies any wrongdoing in its partly-owned Shengjing Bank Co, as well as heavy discounting for empty apartments.

- Evergrande has $50bn in debt, 80% of which is due in the next year. Sheesh.

- $20bn is dollar bonds.

- It is behind all “three red lines” for develeraging imposed earlier this year.

Advertisement