Ever since China installed its “three red lines” policy early this year, there have been increasing signs of stress in China’s mega-development sector. Floor area starts have dropped sharply, equity markets have punished the sector and credit markets begun to tighten the noose on the more freewheeling names.

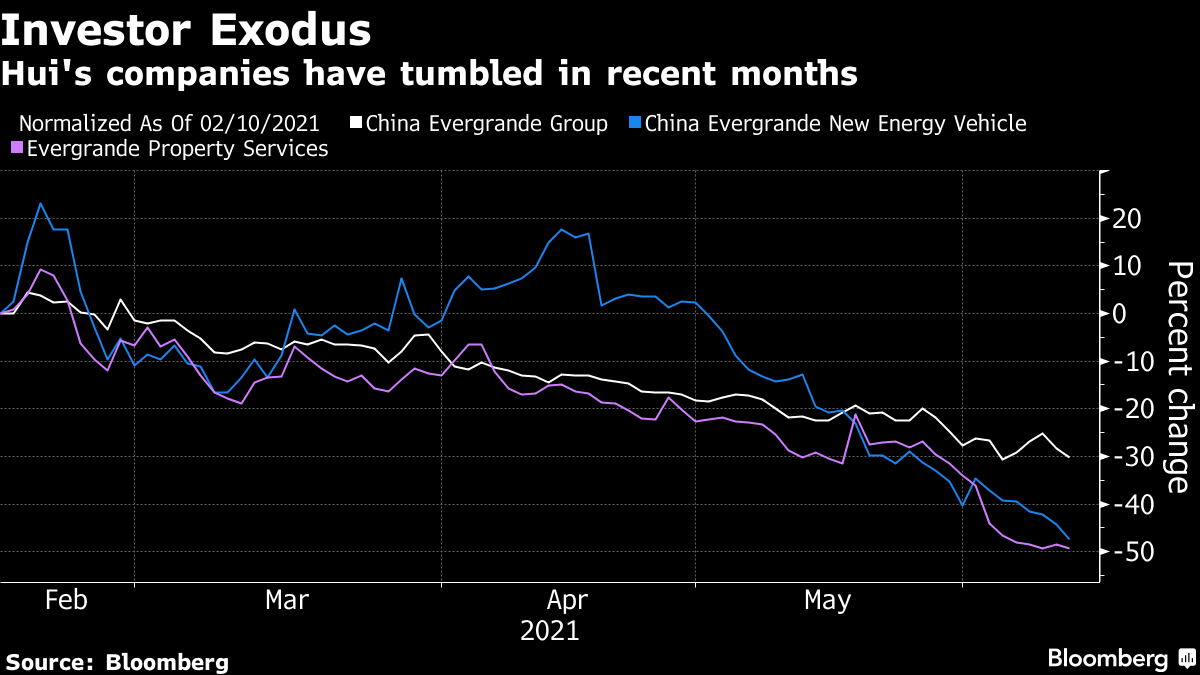

That process continues today as Chin’s greatest and most rogue developer, Evergrande, slides towards deeper crisis. Its equity has halved in six months:

The numbers at risk are pretty staggering. The full Evergrande group has an astonishing $305bn in debt with $50bn in dollar bonds. Some of the yields on this junk are going ballistic and they are not near term:

Advertisement