The great Chinese property developer shakeout is intensifying. This has global significance because this sector alone accounts for an enormous slice of global bulk and base metals demand and therefore inflation. Bloomie has a great article today on the unfolding drama around the “three red lines” policy:

- Many developers have gamed the new deleveraging rules.

- Some have used opaque HK dollar bonds and off-balance sheet vehicles to hide leverage.

- JVs have been used to disguise land purchases and financing.

- But markets have begun to dump equity associated with JVs.

- Without full control of projects, developers can’t sell and raise cash so easily.

- Ratings are in trouble as JVs may be reclassified as short-term debt.

- Beijing is not happy.

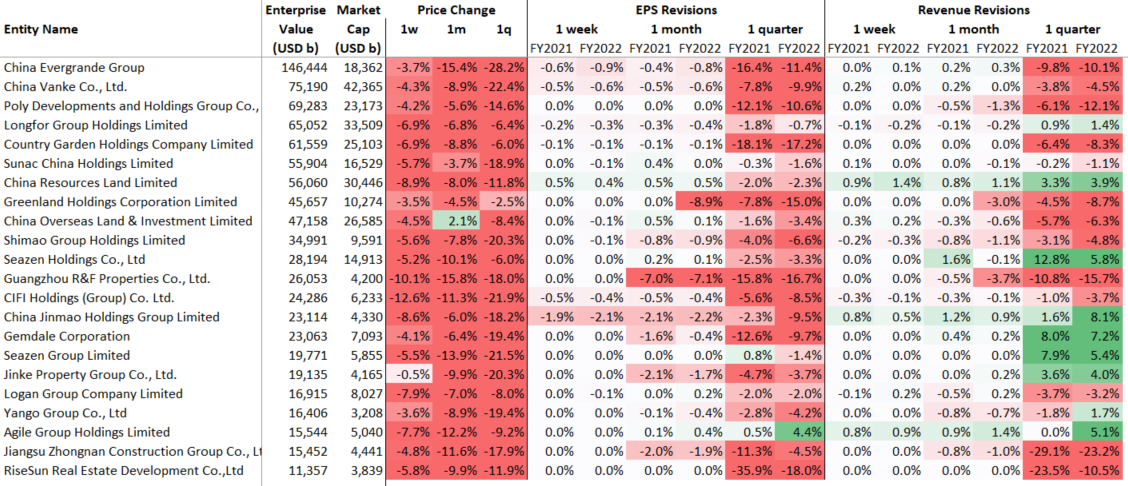

My table of listed Chinese developers is starting look like a bath of blood:

Advertisement