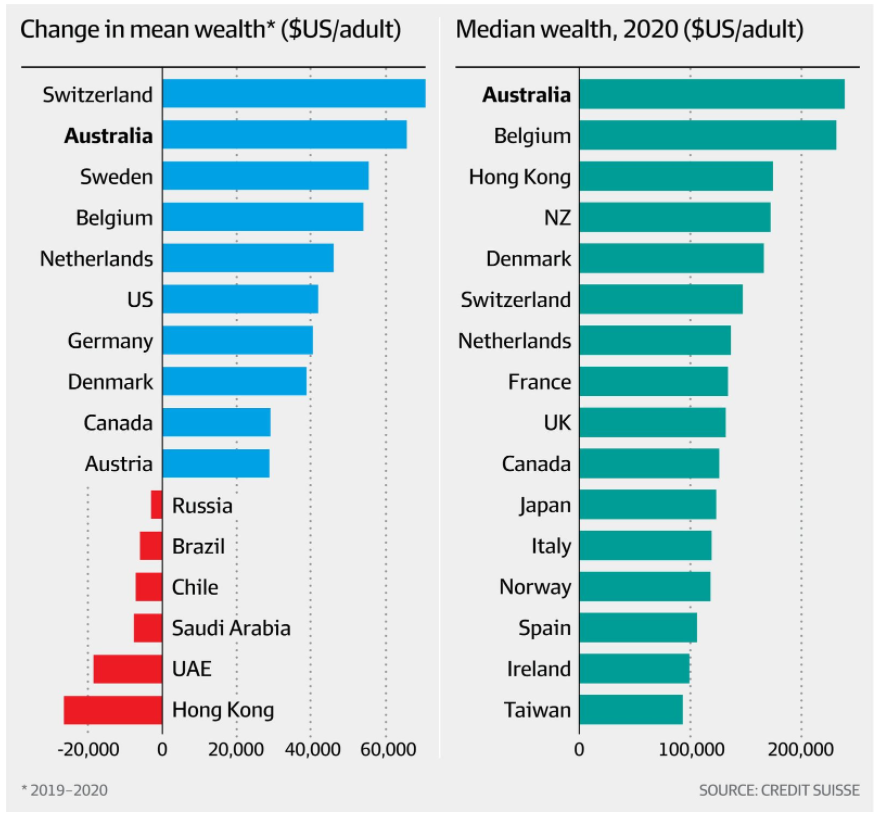

One ‘benefit’ of having some of the world’s most expensive homes, alongside a high home ownership rate, its that it makes households ‘rich’.

That’s the conclusion from the latest Credit Suisse Global Wealth Report, which has declared Australian households the worlds richest:

Aussies top global wealth rankings.