The findings are based on the assumption that buyers have a 20% deposit and factors in the costs of buying, holding a mortgage and the overall costs of renting.

The research also assumes 3% annual price growth over the decade.

From the REA report:

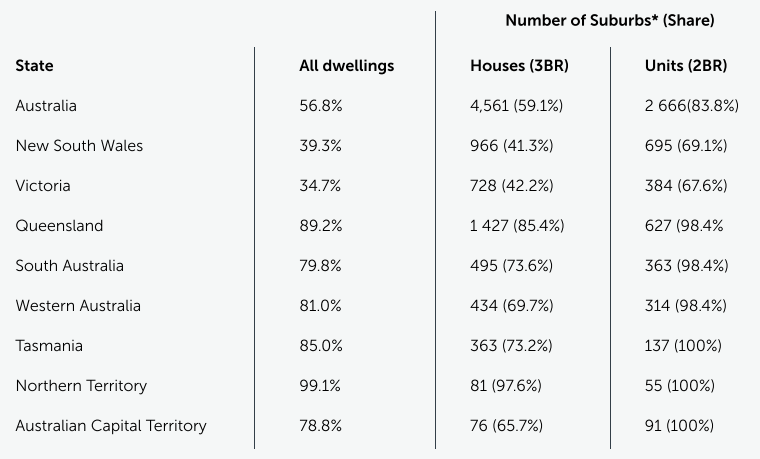

Analysis suggests it is cheaper to buy than rent around 57 per cent of dwellings across Australia. This is based on only modest housing price growth of 3 per cent per year over the next decade.

The results differ by property type. Just over half of houses are cheaper to buy over the next 10 years, but the share of units that are cheaper to buy is almost 75 per cent.

Buying conditions are particularly favourable outside of New South Wales and Victoria. More than 80 per cent of houses, and almost all units outside of the most populous states are estimated to be cheaper to buy than rent.

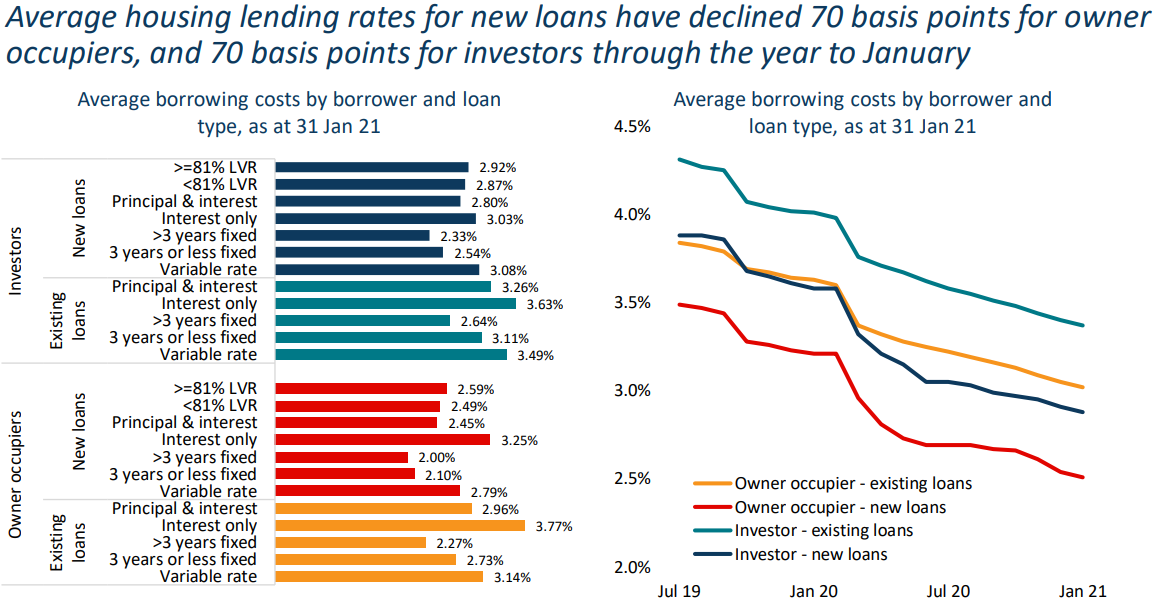

The findings of this report makes sense. Mortgage rates have collapsed below 3% for new owner-occupied borrowers:

New mortgage rates for owner-occupiers are below 3%.

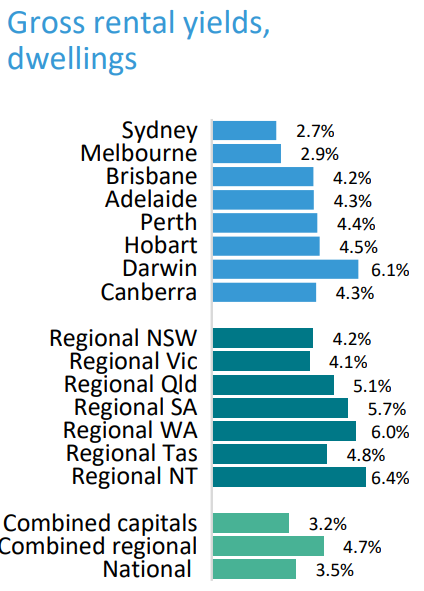

At the same time, gross rental yields outside of Sydney and Melbourne are above 4%:

Gross rental yields are well above mortgage rates outside of Sydney and Melbourne.

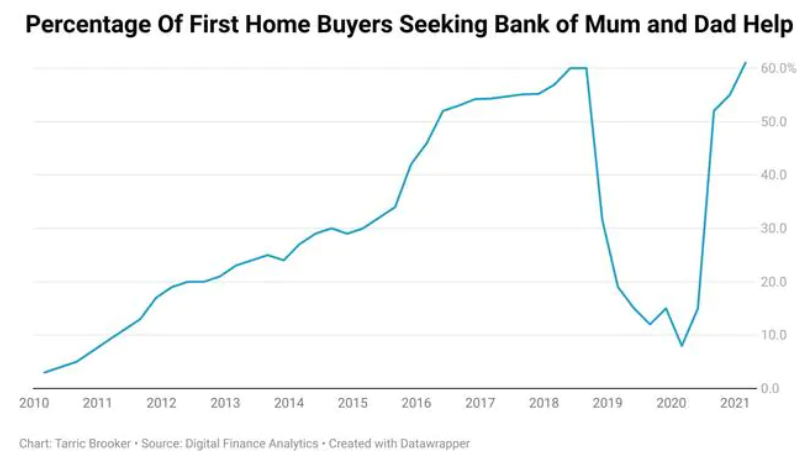

The big issue, however, remains saving for a deposit. This helps to explain why borrowing from parents – the ‘Bank of Mum & Dad’ – has hit a record high 60% of first home buyer mortgages, with the average parental assistance totalling around $90,000:

A record share of first home buyers are receiving financial assistance from their parents.

Repaying one’s mega-mortgage has also become increasingly difficult due to record low inflation and wage growth.

Thus, it may never be cheaper in most markets to service a mortgage, but never more expensive to save for a deposit or pay off the loan.