Former Prime Minister and architect of Australia’s compulsory superannuation system, Paul Keating, headlined Alan Kohler’s four-part special on the future of retirement, aired on ABC’s 7.30 Report.

In this report, Paul Keating erroneously claimed that Australia’s ageing population would make the current Aged Pension system unsustainable without increases in the compulsory superannuation guarantee (SG):

PAUL KEATING: This is one of the critical points. When I started this 35 years ago, 6.7 people between 15 and 65 carried the retirement burden of everyone over 65.

Today that’s 3.7 and by 2030 it will be 3. So you have got three people by 2030 looking after every one over 65 where before there was 6.5 people.

So that burden means that you want superannuation to be able to withdraw the burden on the pension, so the few taxpayers left in the system are not carrying it…

This is why nothing beats self-provision, nothing beats self-provision.

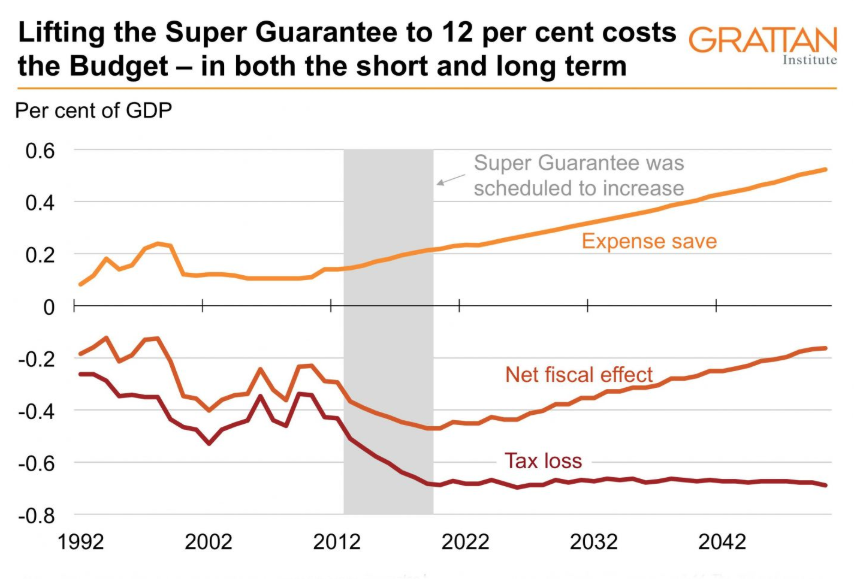

The Grattan Institute’s Brendan Coates has demolished Paul Keating’s claim, noting that lifting the SG to 12% would actually worsen the long-term sustainability of the federal budget:

Advertisement

The Retirement Income Review also concludes that the legislated increase in compulsory super from today’s 9.5 per cent of wages to 12 per cent will exacerbate rather than alleviate the budgetary costs of an ageing population, making the Age Pension less sustainable in future. Treasury projects that increasing compulsory super will cost taxpayers more in super tax breaks than it would save from spending on the Age Pension through until 2055. And even then, 35 years of accumulated debt — more than 2 per cent of GDP — would need to be paid back before taxpayers ended up ahead.

That’s right, the Retirement Income Review explicitly concluded that any cost savings for the Aged Pension would be more than offset by higher superannuation concession costs:

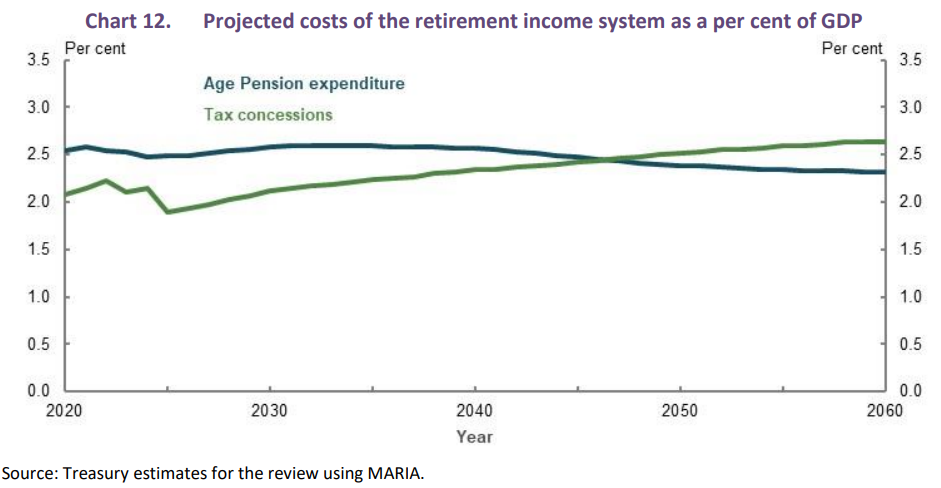

As the superannuation system matures, the cost of superannuation tax concessions is projected to grow as a proportion of GDP such that by around 2050 it exceeds the cost of Age Pension expenditure as a per cent of GDP (Chart 12). This is the result of growth in the cost of earnings tax concessions…

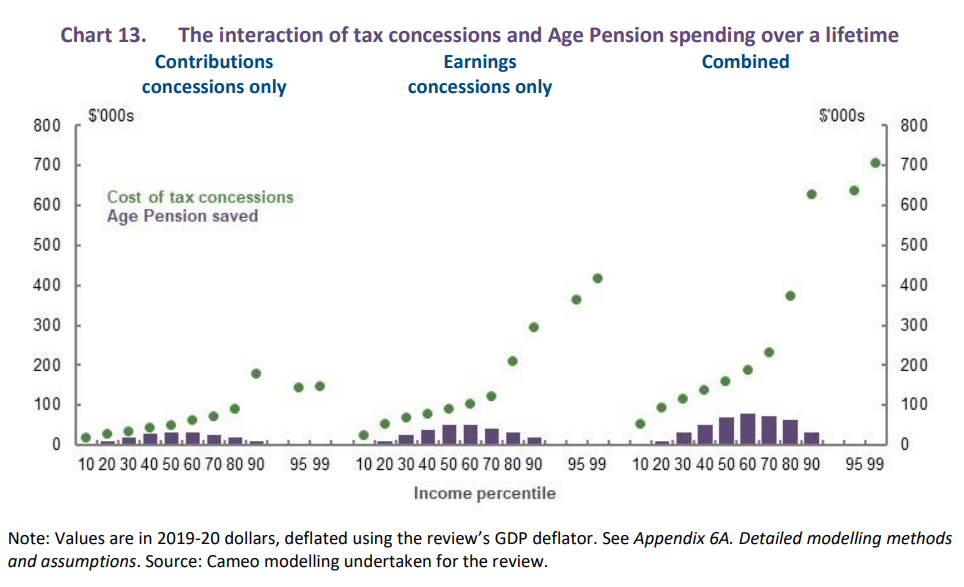

Across the income distribution, the lifetime cost of superannuation tax concessions is projected to outweigh the associated Age Pension saving (Chart 13)…

Advertisement

Modelling by actuary firm Rice Warner similarly concluded that lifting the SG would create net costs to the federal budget over both the short and long-term:

“Our modelling shows that the legislated increase in the SG will not have much impact on the Age Pension for many years but will reduce it by about 0.1% of GDP in the second half of this century on current means testing settings. Conversely, the tax concessions from the increase are more immediate and they will average about 0.22% of GDP throughout this century”.

An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).

As did modelling from the Grattan Institute, which estimated that raising the SG to 12% would cost the federal budget an additional $2 billion per year and would far outweigh any benefits from lower Aged Pension payments:

Lifting the superannuation guarantee would damage the federal budget.

Advertisement

Clearly, Paul Keating has it back-to-front. The high cost of Australia’s compulsory superannuation system (over $40 billion a year) is preventing the Age Pension from being lifted.

Raising the SG from 9.5% to 12% would only make the situation worse.

Disclosure: The MB super fund stands to gain from the SG increase going ahead, since it would mean having larger funds under management. Nevertheless, MB opposes the increase on public policy grounds.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.