On Friday, the federal government released Treasury’s 600-page Retirement Income Review Final Report, which highlighted in great detail why lifting the superannuation guarantee (SG) from 9.5% would be unambiguously bad policy.

First, the Review notes that the federal budget would be plunged further into deficit, since any cost savings for the Aged Pension would be more than offset by higher superannuation concession costs:

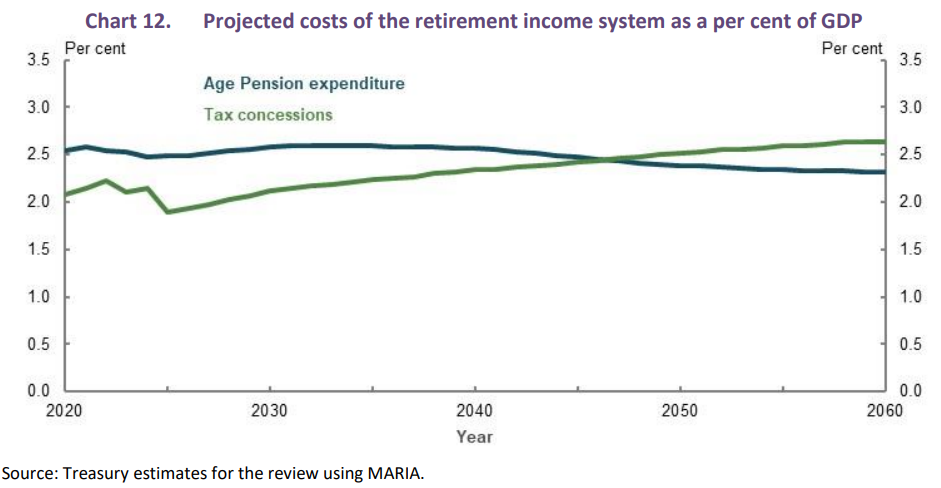

Government expenditure on the Age Pension as a proportion of GDP is projected to fall slightly over the next 40 years to around 2.3 per cent [from 2.5 per cent]. Higher superannuation balances reduce Age Pension costs. The cost of superannuation tax concessions is projected to grow as a proportion of GDP and exceed that of Age Pension expenditure by around 2050. This is due to earnings tax concessions. The increase in the SG rate to 12 per cent will increase the fiscal cost of the system over the long term…

The sustainability of compulsory superannuation is best assessed by looking at its full budgetary impact and not just the reduction in Age Pension expenditure as the superannuation system matures. The cost of superannuation tax concessions also needs to be taken into account…

Around 71 per cent of people over Age Pension eligibility age received Age Pension or other pension payments as at June 2019. Notwithstanding an ageing population, this proportion is projected to fall to 62 per cent in 2060. There is also a shift toward people receiving a part-rate pension (rather than the full-rate pension), rising from 38 per cent of age pensioners today to a projected 63 per cent in 2060. This shift is the result of higher superannuation balances and the impact of the means test, particularly the assets test, in determining eligibility for the Age Pension.

In contrast, as the superannuation system matures, the cost of superannuation tax concessions is projected to grow as a proportion of GDP such that by around 2050 it exceeds the cost of Age Pension expenditure as a per cent of GDP (Chart 12). This is the result of growth in the cost of earnings tax concessions…

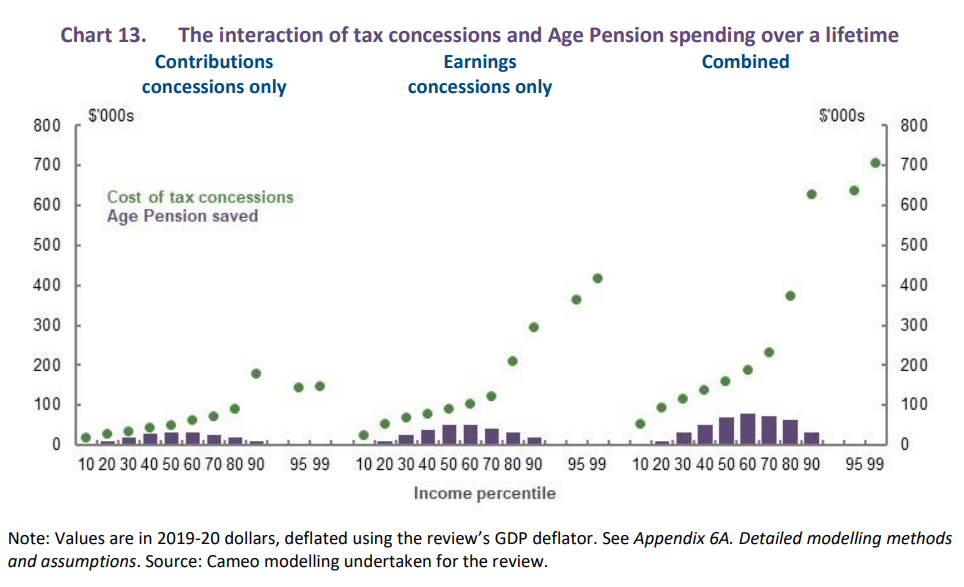

To the extent that superannuation tax concessions are contributing to higher superannuation balances of lower- to middle- income earners, they help to reduce Age Pension expenditure. But the main influence behind the growth in superannuation balances is the SG. Tax concessions are largely concentrated among higher-income earners who are close to and above preservation age. Across the income distribution, the lifetime cost of superannuation tax concessions is projected to outweigh the associated Age Pension saving (Chart 13)…

Second, the Review warns that lifting the SG to 12% would increase inequality in Australia, since super concessions overwhelmingly benefit higher income earners:

Advertisement

There are areas where superannuation tax concessions are not a cost-effective way to help people achieve adequate retirement incomes. In particular, the cost of the earnings tax exemption in retirement will grow faster than the growth in the economy as the system matures and provides the greatest boost to retirement incomes of higher-income earners…

Changes to superannuation earnings tax concessions would improve equity, and in turn boost public support for the system…

While the Age Pension helps offset inequities in retirement outcomes, the design of superannuation tax concessions increases inequality in the system. Tax concessions provide greater benefit to people on higher incomes.

Third, the Review notes that lifting the SG to 12% would reduce wage growth:

The weight of evidence suggests the majority of increases in the SG come at the expense of growth in take-home wages. This view is based on empirical research, economic theory, evidence across a number of countries, and the original policy intent of the SG…

Estimates suggest that maintaining the SG at 9.5 per cent will result in working-life incomes about 2 per cent higher than under a 12 per cent SG rate in the longer term…

Advertisement

These same concerns were noted in the Henry Tax Review and have been argued ad nauseum on this site.

As we keep saying, the main beneficiary from lifting the SG to 12% are superannuation funds, which would earn fatter fees on bigger funds under management. But their gains would come at the direct expense of both taxpayers and workers.

It’s time to abandon the planned increases in the SG once and for all.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.