The Australian Bureau of Statistics (ABS) yesterday released its International Trade Price Indexes for the March quarter of 2021, which revealed that export prices rose by 11.2% over the quarter and by 8.6% through the year.

The increase in export prices was driven by an 18.2% quarterly rise in metalliferous ores and metal scrap prices driven by strong iron ore demand from China and constrained global supply owing to the tragic dam failure at a Vale mine in Brazil in early 2019.

Over the year, metalliferous ores and metal scrap prices surged by 49.8%, again driven by soaring iron ore prices.

Iron ore prices are approaching $US200 a tonne.

By contrast, import prices rose by only 0.2% in the March quarter and fell by 6.2% through the year.

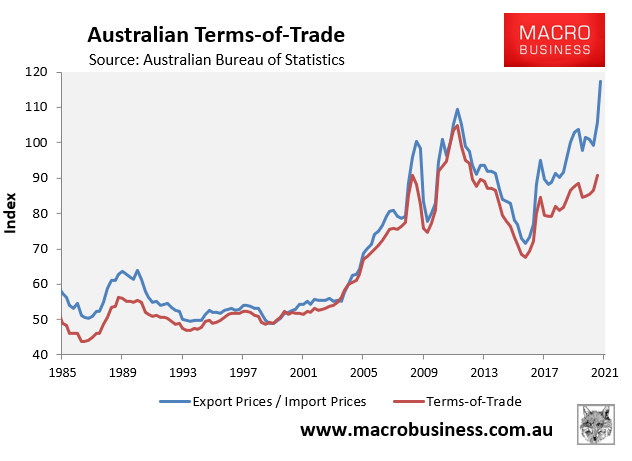

The change in the import/export price index gives a good proxy for Australia’s terms-of-trade (ToT). As shown in the next chart, Australia’s ToT is looking at a circa 11.0% increase in the March quarter and a 15.8% increase through the year:

Australia’s terms-of-trade should record a massive rise in Q1 2021.

The importance of this cannot be understated. The ToT measures the average price level of exports to the average price level of imports. Thus, when the ToT rises a given quantity of exports can pay for a larger quantity of imports, effectively granting the nation a pay rise.

The ToT, therefore, is a key determinant of national income, as well as a key driver of government finances via company tax receipts.

Indeed, UBS yesterday forecast that tax revenue could rise by $US20 billion in the federal government’s 11 May Budget due to the strong iron ore price. The spot price of benchmark iron ore has risen by 130% in the last year (see above chart), and it recently peaked at around $US193 per tonne. The federal government’s previous revenue forecasts were based on an average iron ore price of just $US55 per tonne in 2020-21.

Macquarie also believes that the price of iron ore could soon top $US200 a tonne, although Vivek Dhar of the Commonwealth Bank says an easing of demand in China could see the price fall to around $US110 per tonne by the end of 2021.

Much like they did between 2009 and 2012, the federal budget and company profits will ride the iron ore boom. The main difference this time around is that the price boom is not being matched by increased mining investment, which means there will be little spillover into jobs and wages. It is largely a profitless boom for Australian workers.