One of the less well-understood dimensions of Chinese economic restructuring is the travails of its corporate bond market. For a few years now, authorities have been slowly removing the moral hazard that has dominated Chinese debt markets through its development phase. This causes periodic panics in financial markets but it should not. This is an excellent policy from the perspective of the Chinese. It is all about letting former rent-seeking corporations that were dependent upon rolling ponzi-debt go bust. Over time this will help shift Chinese capital from these misallocated laggards, often in the mining and real estate over-investment sectors, to more productive uses.

Another example is available today:

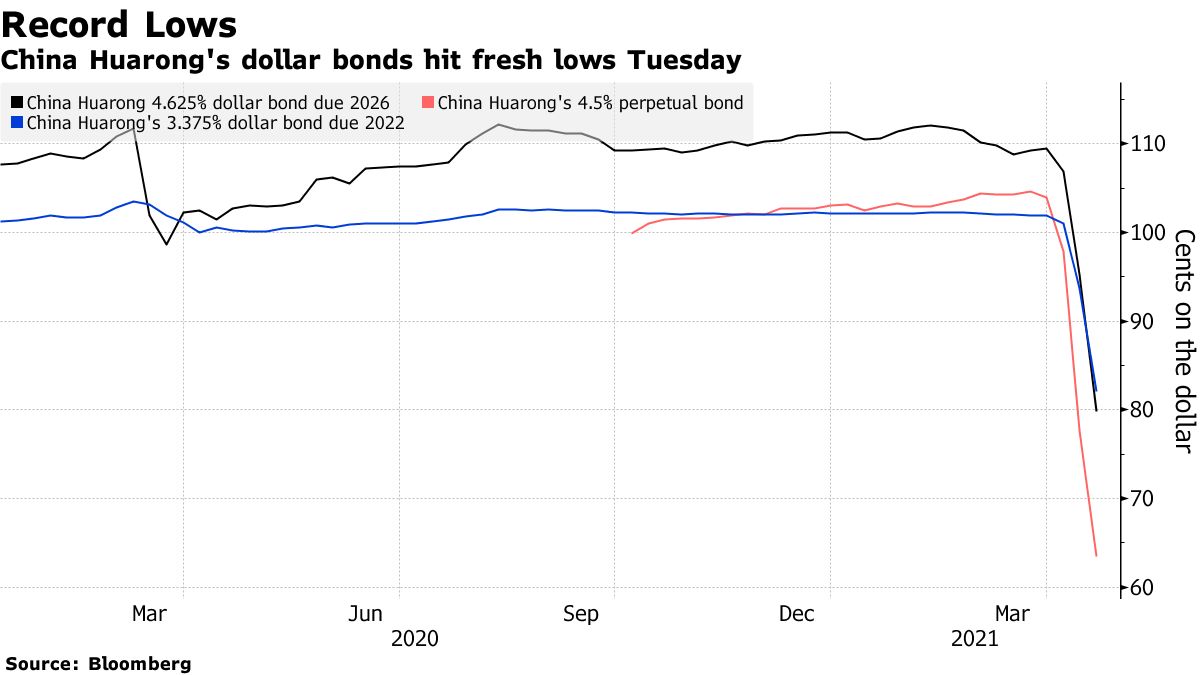

- Chinese debt manager, China Huarong Asset Management, is seeing distinct distress appear in its balance sheet.

- Contagion appeared in the junk bond market with real estate firms hit especially hard:

- Authorities have remained silent despite the firm’s $41bn in outstanding bonds, 41% of which roll in the next twelve months.

Amusingly, the CCP executed the chairman of Huarong for corruption in January so he’s not around to right the ship.

Goldman has more on the broader market:

Number of China stress situations still low.

Our emphasis at the beginning of this year was managing idiosyncratic risks, with credit analysis paramount, though not to adopt a broader negative stance. Supporting that is our belief that Chinapolicymakers will ensure systemic risk concerns remain in check, and therefore credit differentiation to be the main theme. And looking at the number of defaults so far this year, there are no signs that credit stresses are prevalent across larges ections of the China credit market. For example, the number of China new bond defaults in both the onshore and offshore markets has been relatively low since thestart of the year, and FY20 results for China property companies have, so far, shown improved compliance with the “Three Red Lines” regulation that aims to reduce leverage within the property sector.

But larger stresses and reducing moral hazard risks have led to repricing ofChina HY.

Despite the number of stressed situations being relatively low, there has been a large repricing of China tail risk, which has affected the overall China HY market. Spreads on the ABBI IG and ABBI HY indices are tighter by 12bps and 7bpsso far this year, with most sub indices seeing tighter spreads since the start of the year. The exception is the ABBI China HY index, where spreads have widened by82bps, substantially underperforming the overall Asia credit market. To us, this reflects two series of events that have dented China domestic investor sentiment. First, recent defaults have been large, most notably China Fortune Land, which had USD 4.6bn of offshore bonds outstanding at the time of default, reinforcing the notion that “too big to fail” may no longer apply to Chinese credits. Second, the impact from the defaults from state-owned enterprises (SOEs) at the end of 2020, in particularfor Yongcheng Coal & Electricity Holding Group, and the focus on tackling local government indebtedness suggest that implicit government support is waning.

No signs that China policymakers are to ease.

The increase in credit concerns raisesthe question whether they could lead to China policymakers easing. We believe that isnot likely at the current juncture. First, despite very heavy onshore bond redemptions inMarch and April, there has not been any pick up in refinancing difficulties amongstcorporates onshore, andnet domestic corporate bond issuanceturned positive in Jan toMarch this year, rebounding from the negative territory in Nov and Dec 2020. Second,China’s activity levels remain firm, as evidenced by theOfficial PMIsthat showedactivity growth accelerating in March. Therefore, unless onshore funding market stresspicks up and/or activity levels weaken more than expected, policymakers are unlikely todeviate from their credit cleanup path.

There is always the possibility that this turns to systemic risk and authorities are forced to intervene again. Yet, the global economic recovery and booming Chinese exports, as well as other internally-funded restructurings such as the push into technology, are the perfect cover for the debt cleanup.

While those transpire, the base case is China has the macro momentum to weather these constructive shakeouts in its corporate debt market. Notwithstanding the tail risk of a blowup.

But that should provide zero reassurance to Australian investors. This program of debt cleanups is focused especially on over-investment in areas like realty. It will land on construction if it continues, even as wider growth remains on a robust, if falling, flight path.

Indeed, the first two months of the year saw real estate starts get off to a surprisingly slow start (marked by blue circle) which coincided with the rollout of the “three red-lines” policy:

We need a few more months of data to confirm this as a new trend given early year releases are lumpy. But it is a real possibility that iron ore demand will slow sharply later this year as catch-up construction and new starts fade together.