Last week we received two very strong pieces of data pertaining to the Australian property market.

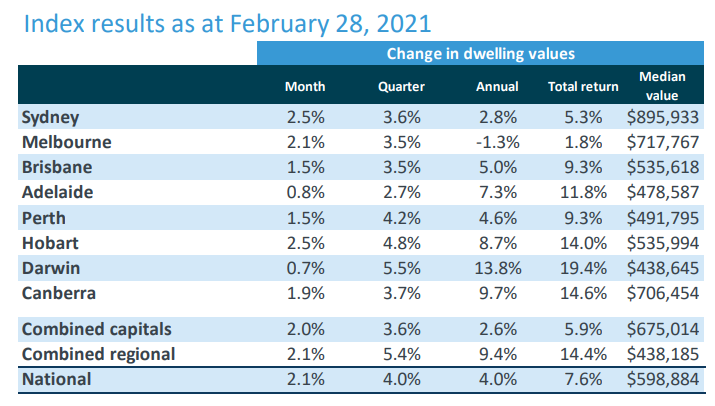

First, CoreLogic released its dwelling value results for February 2021, which recorded the strongest monthly rise in values (2.1%) since August 2003. Moreover, every jurisdiction across Australia reported strong quarterly price growth (4.0% nationally):

Dwelling values are rising strongly across every Australian jurisdiction, according to CoreLogic.

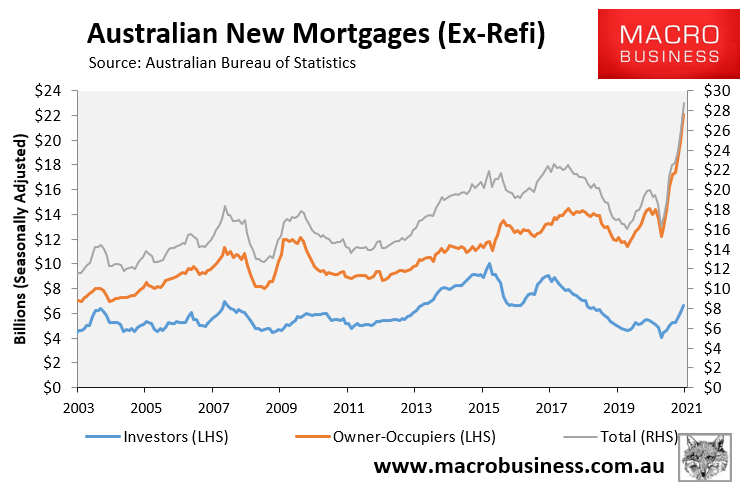

Second, the Australian Bureau of Statistics (ABS) released data on new mortgage commitments, which reported their strongest ever monthly growth:

Australian mortgage demand has never been hotter, led by owner-occupiers.

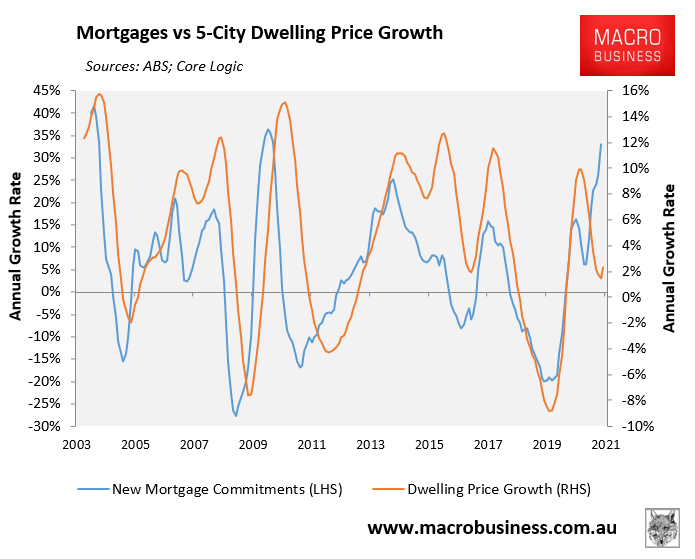

Regular readers will know that I consider mortgage growth to be the single best indicator for Australian dwelling value growth. This is based on years of empirical data showing that growth in new mortgages typically leads growth in dwelling values, as illustrated in the next national chart:

The strong rise in mortgage demand is pointing to big dwelling value gains.

Clearly, the massive acceleration in mortgage demand is pointing to very strong price growth nationally, which we have already begun to witness.

Below are charts plotting new mortgage growth versus dwelling values across the five major capital city markets.

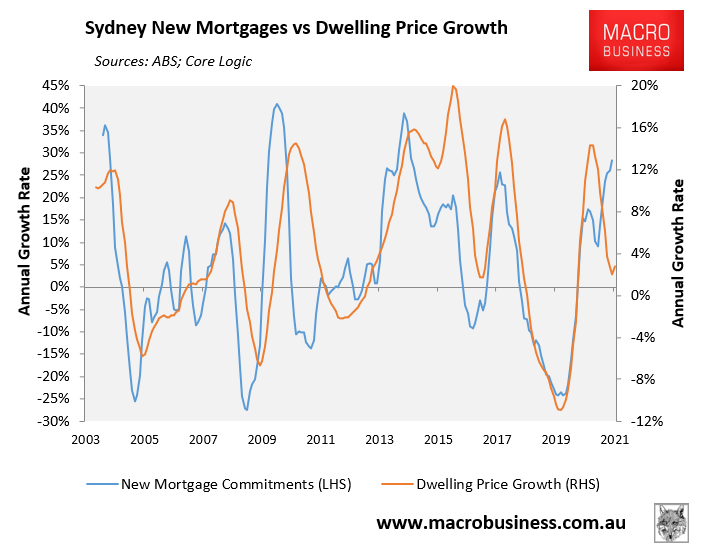

Sydney:

Mortgage demand in Sydney has accelerated to levels above the 2017 boom, but below the 2013 boom. This would suggest the Sydney’s property market is headed for strong price growth in 2021:

The acceleration in mortgage demand is suggesting strong price growth for Sydney in 2021.

Melbourne:

The mortgage rebound has not been quite as strong in Melbourne, suggesting softer (but still strong) property price growth in 2021:

Mortgage demand has bounced in Melbourne, indicating strong price growth in 2021.

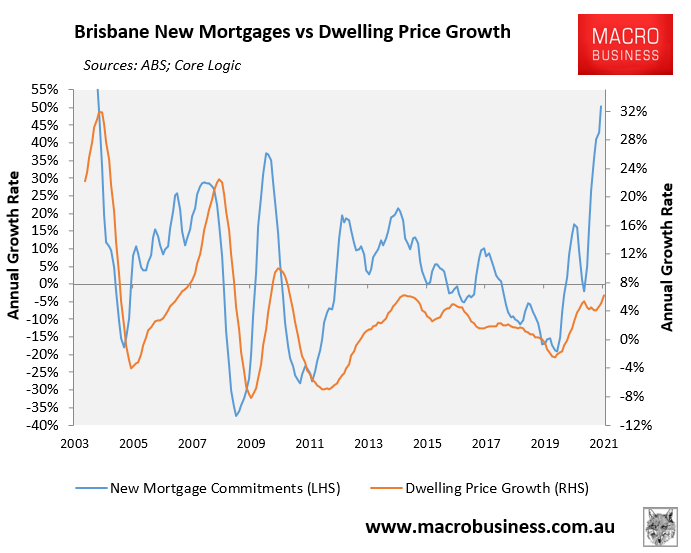

Brisbane

Brisbane’s mortgage demand is the second strongest in recorded history, suggesting turbo-charged price growth in 2021:

Brisbane’s mortgage demand is off-the-charts, suggesting very strong price growth in 2021.

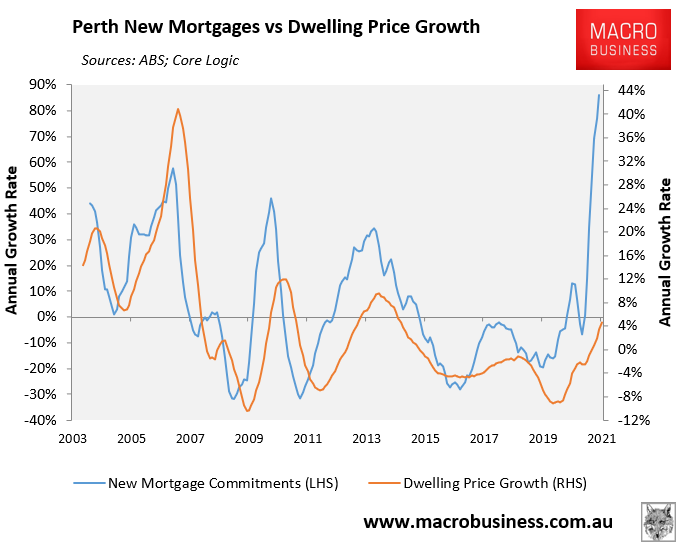

Perth:

Perth’s mortgage demand is even stronger – the highest in recorded history – suggesting massive price growth in 2021:

Perth’s mortgage demand has never been stronger, suggesting massive price growth in 2021.

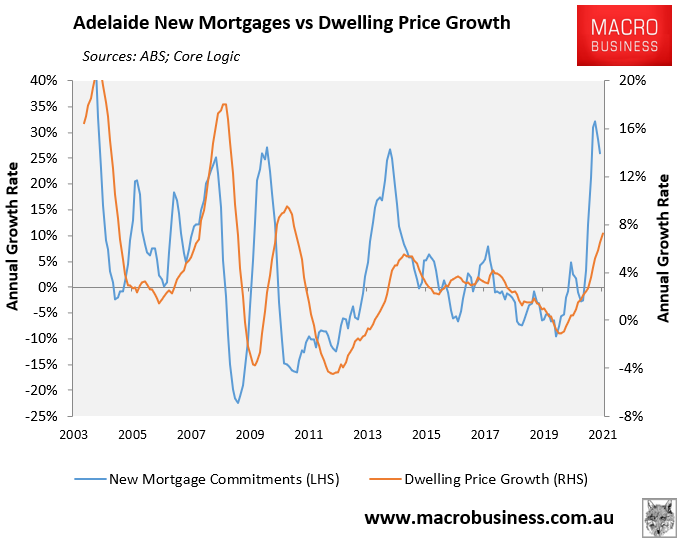

Adelaide:

Unlike the other major capitals, mortgage demand has moderated in Adelaide, which suggests that price growth will soon peak:

Adelaide’s mortgage demand has softened, suggesting price growth will soon moderate.

Clearly, 2021 is shaping up to be a boom year for Australian property.

That said, I am most bullish on Perth and Brisbane. Not only is mortgage growth strongest in these two markets, but they also represent much better relative value, based on rental returns and their historical valuations versus the other capitals.