Dr Cameron Murray is a good friend of the site and one of the few commentators in the country to tip a property boom mid last year during the height of the COVID-19 pandemic.

This week Dr Murray was interviewed by The Guardian where he tipped that smaller markets will lead this property cycle:

Our macro-stabilisation policy works by juicing house prices”…

“This is a policy most central banks have adopted. Secondly, we’re just at that point in the cycle. The best parallel to the situation now is 2004. I think we’re in a very similar phase right now. Sydney boomed early, then it tapered off. Then the rest of the country shot up for four years in line with the broad global house price cycle.

“The economy runs in cycles and a lot of regional Australia hasn’t been through that boom cycle. Now it’s their turn.”

My view is that pretty much all markets outside of Melbourne and Sydney will lead the boom.

There are two primary reasons for this view: 1) affordability; and 2) juicy rental yields.

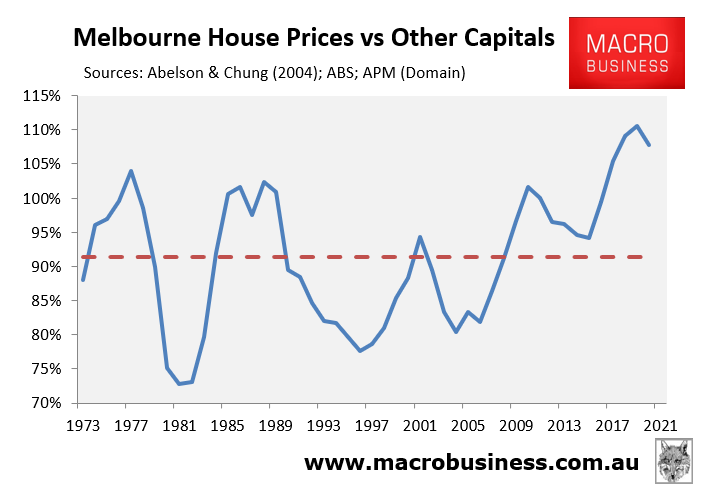

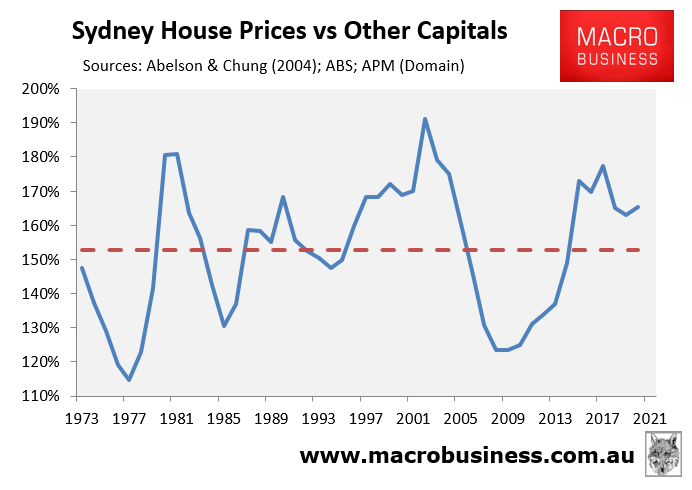

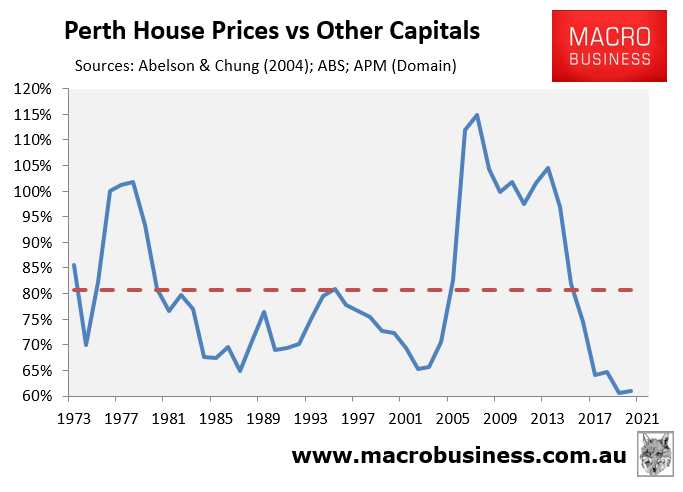

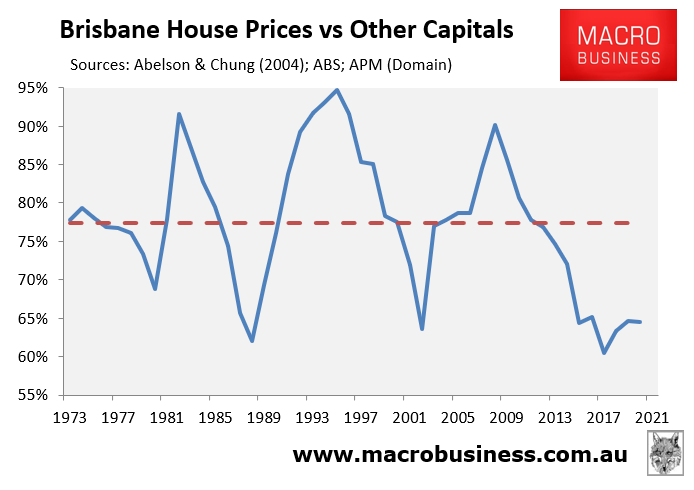

To illustrate the first point – affordability – below are charts plotting median house prices in the five main capitals against the weighted average of the other capital cities.

Melbourne’s ‘relative value’ is poor based on this metric with its median house price tracking at 108% of the other capital cities as at December 2020 – close to the highest level in nearly 50 years of data:

It’s a similar story in Sydney where its median house price was tracking at 165% of the other capital cities as at December 2020 – well above the historical average of 153%:

A polar opposite situation exists in Perth whose housing market was the ‘cheapest’ in nearly 50 years in comparison with the other capitals.

Perth’s median house prices was tracking at 61% of the other capitals as at December 2020, well below the historical average of 81%:

Brisbane’s relative affordability is also excellent, with its median house price tracking at 65% of the other capitals as at December 2020, well below the historical average of 77%:

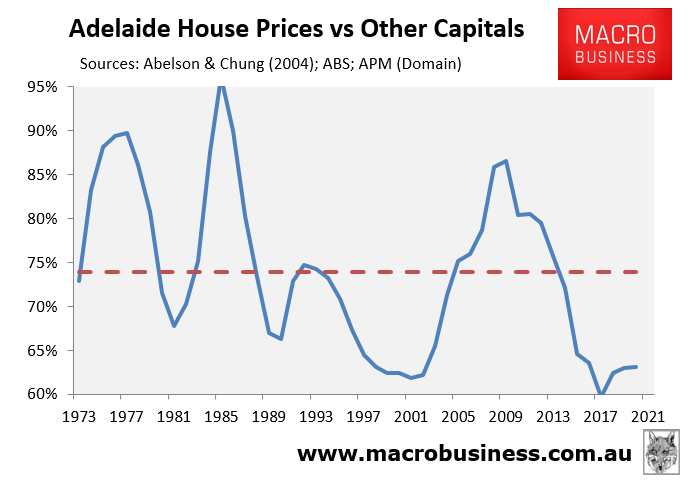

The story is similar for Adelaide whose median house price was 63% of the other capitals as at December 2020, again way below the historical average of 74%:

While I don’t have data on the other capitals or regions, we can infer that the situation is similar across most locations across Australia by looking at rental yields:

Rental yields are typically much higher outside of Sydney and Melbourne. They are also typically growing at a much faster pace.

The upshot is that if you are looking to invest in the Australian property market, you will likely achieve better returns looking outside of the two major capitals.