The floor continues to fall out from under the mortgage market, especially with respect to fixed rates.

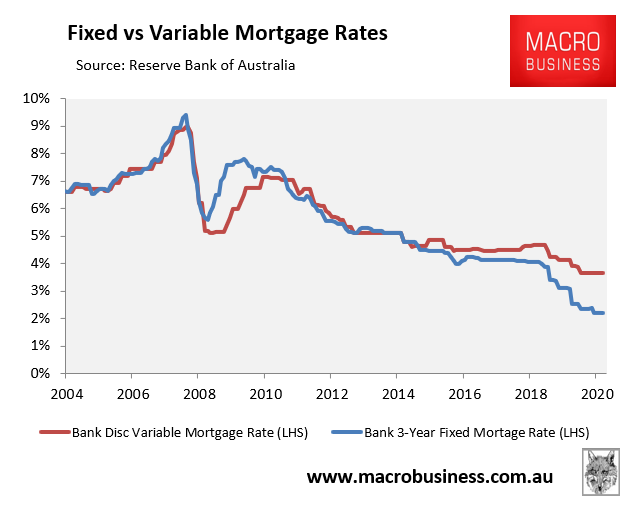

Since the beginning of the COVID-19 pandemic, fixed mortgage rates have experienced much bigger declines than variable mortgage rates, providing borrowers with opportunities to make big savings on their repayments.

As shown below, the average rate applying to existing 3-year fixed owner-occupied mortgages was only 2.19% as at February 2020, 1.46% below the average discount mortgage rate on existing owner-occupied variable mortgages:

Fixed mortgage rates cratered 1.46% below variable mortgage rates in February 2021.

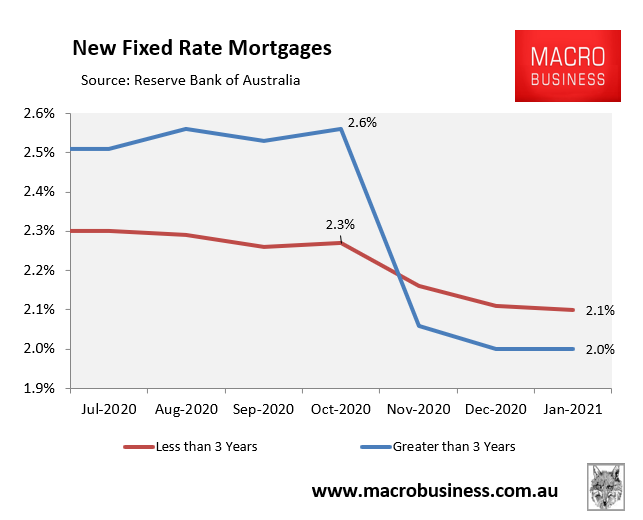

The rates on new fixed mortgages are even lower.

According to the RBA, a typical new owner-occupier borrower in January could obtain a fixed rate mortgage at just 2.1% if they chose a term of less than 3-years, or just 2.0% if they went for a term over 3-years:

Rates on new fixed term mortgages have plummeted to around 2%.

Amazingly, mortgage rates continue to fall with Westpac yesterday cutting its two and three-year fixed mortgage rates by up to 20 basis points:

Its two-year fixed owner-occupier loan now garners a rate of 1.79 per cent – the lowest on offer within the product category.

Westpac’s three-year fixed rate now sits at 1.88 per cent, while its four-year fixed is at 1.89 per cent.

Mortgage rate cuts have been implemented across the Westpac banking group, which includes St George, Bank of Melbourne and BankSA.

RateCity’s Sally Tindall believes mortgage rates will fall even further, stating “it’s likely there’ll be more cuts in the weeks to come as banks compete for the record levels of new lending coming through the door”.

Who knows how low mortgage rates could go? The RBA could always follow Europe’s lead and drop the rate on its Term Funding Facility (TFF) into negative from 0.1% currently. This could send fixed mortgage rates to around 1% or lower.

In an age of quantitative easing, the old rules no longer apply.