Fixed rates are all the talk in Australia’s mortgage market.

Over the past year, fixed mortgage rates have experienced far larger declines than variable mortgage rates, thus offering borrowers huge opportunities for savings.

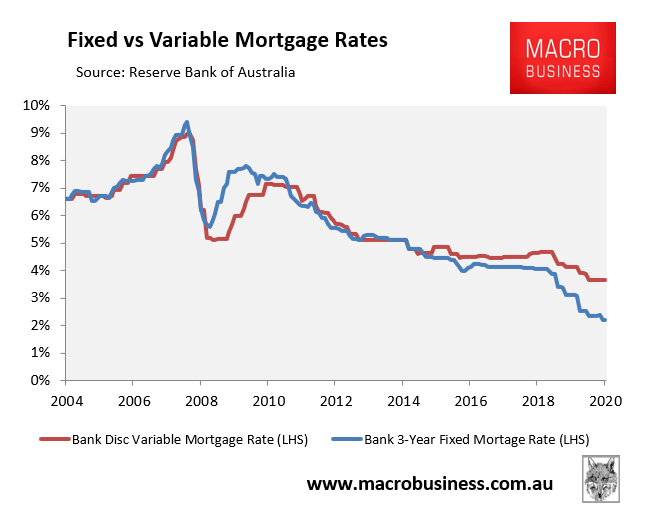

As shown in the next chart, the average rate applying to existing 3-year fixed owner-occupied mortgages was only 2.20% as at January 2020, 1.45% below the average discount mortgage rate on existing owner-occupied variable mortgages:

The rate applying to new fixed rate mortgages are even lower, according to the RBA.

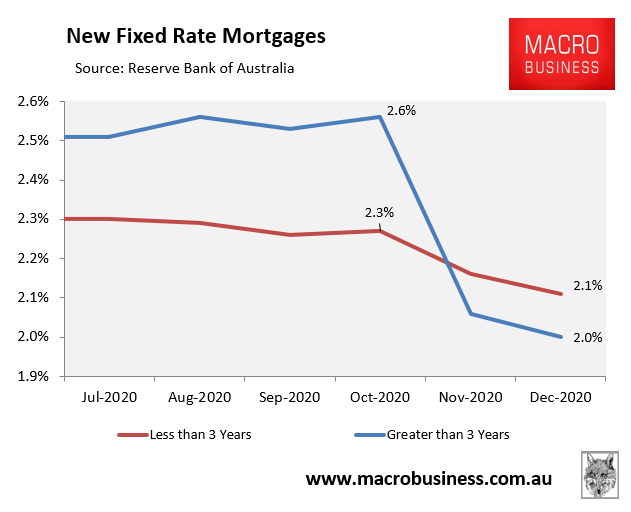

As shown in the next chart, a typical new owner-occupied borrower could expect to obtain a fixed rate mortgage at just 2.1% if they opt for a term of less than 3-years, or only 2.0% if they go for a term over 3-years:

Yesterday NAB joined the rate cutting frenzy, slashing some fixed mortgage rates below 2%:

NAB’s three-year fixed rate has been shaved by 11 basis points to 1.98 per cent, while its five-year fixed owner-occupier loan shed 55 basis points to 2.24 per cent…

“Both our three- and four-year fixed rates for owner-occupiers paying principal and interest are now below 2 per cent, a level that would have seemed unbelievable just a few years ago” [NAB executive Andy Kerr said]…

Some smaller lenders are offering even cheaper fixed rates:

The lowest three-year fixed rate advertised of 1.75 per cent is being advertised by NAB’s subsidiary UBank, while Homestar Finance offers the lowest variable rate of 1.79 per cent.

However, RateCity’s Sally Tindall believes we may be approaching the bottom of the rate cutting cycle:

“While we’re nearing the bottom of the rate cycle, provided the cash rates remains above zero, we could see one or two of the other big banks follow suit with some minor cuts in the weeks to come.”

I am less convinced that we are approaching the mortgage rate bottom. Much will depend on what the Reserve Bank of Australia (RBA) does with the Term Funding Facility (TFF).

Earlier this month, RBA Governor Phil Lowe said that the TFF is unlikely to be lowered, unless there is a “marked deterioration in funding and credit conditions”:

…the Term Funding Facility will be maintained as it is. Banks are able to draw on the facility up until end June, which means they will have the benefit of low-cost funding out to mid 2024. The Board would consider extending this facility if there were a marked deterioration in funding and credit conditions in the Australian financial system. At the moment, there are no signs of this.

One only needs to look across at Europe to see how the rates story is likely to unfold.

The European Central Bank (ECB) began with 0.1% funding for banks in 2014. By 2016 the rate had fallen to -0.4%. And now it’s -1.0%. So basically, the ECB will pay commercial banks up to 1% for every dollar they lend.

In fact, Denmark has already begun offering homeowners 20-year loans at a fixed interest rate of zero percent.

These developments could be a harbinger of what lies ahead for Australia.

Eventually, the TFF will likely go negative as the RBA chases mortgages with rates of 1% or less.