For the past thirty years, markets and economies have enjoyed what has become known as the Great Moderation. This was a period of declining inflation and therefore business cycle volatility.

Many reasons are have been proferred for the evolution of these longer and less volatile business cycles.

Some see it as the triumph of the central bank as independence and inflation-targeting overtook the boom and bust inflation cycles of the 70s and 80s.

Others see it as part and parcel with globalisation as labour markets became globally integrated meaning that local inflationary bursts were brief as they tended to mobilise an inexhaustible supply of cheap foreign labour to quell producer prices. This is especially the case in Australia over the past two cycles as governments have explicitly linked Australian labour market conditions to much lower standards offshore via mass immigration and temporary work visas.

A third explanation is the age of information technology which handed capital an indispensable productivity investment tool that could likewise short-circuit labour inflation outbreaks.

I would add that inequality has played a major role as demand deficits get worse everywhere thanks to poor and corrupted policy that has hollowed out middle classes and guaranteed oversupply of everything worldwide.

And, in turn, the evolution of peak private debt which was a self-perpetuating feature of the Great moderation itself, has further exacerbated demand deficits.

Doubtless, it is all of these factors rolled into one.

So, as we enter what is a much more dedicated effort by some monetary and fiscal authorities – most notably in the US where the emergence of the populist Donald Trump gave it greater urgency – we need to ask will this also end the Great Moderation? Will we return to boom and bust cycles of the past?

Morgan Stanley has crack at that today:

All cycles have their quirks. The last three US recessions were adjacent to: 1) The largest equity bubble in history; 2) The largest financial crisis since the Great Depression; and 3) A global pandemic. If you’re looking for a ‘normal’ recession, good luck!

Surprisingly, as different as these three recessions were, they were all preceded by similar phenomena. All three saw an inverted yield curve within~6months before they started. All three followed a Fed hiking cycle and core CPI above 2.4%Y. All three were preceded by high consumer confidence, low unemployment and declining equity market breadth.

…Yet while this cycle has so far followed many ‘normal’ patterns, its evolution could be unique. For several reasons, in the US and globally, this cycle could burn unusually hot.

The first is stimulus. The global economy is seeing record levels of fiscal and monetary stimulus at the same time. ‘Unprecedented’ is an overused word in our business, but this cycle qualifies and is unique among other post-recessionary periods.

The second is savings. Savings rates stand at historically highs in the US, Europe and China. While the distribution of these savings is uneven, they provide substantial fuel for consumption. Corporate cash balances are also elevated, a buffer against COVID-19 uncertainty that could find its way into spending as confidence returns.

Third is the labour market. Our economists note that the majority of recent job losses were in COVID-19-related sectors. If the economy can reopen safely, it seems reasonable that we could see an unusually fast labour normalisation as

the sectors comeback.Finally, there is the future path of policy. Global central banks are signalling a strong commitment to supporting growth and returning inflation to more normal levels. Governments are showing little desire to eventually raise taxes or cut spending. Both stances suggest a hotter cycle, less likely to be restrained by policy tightening than the previous expansions.

US inflation breakevens

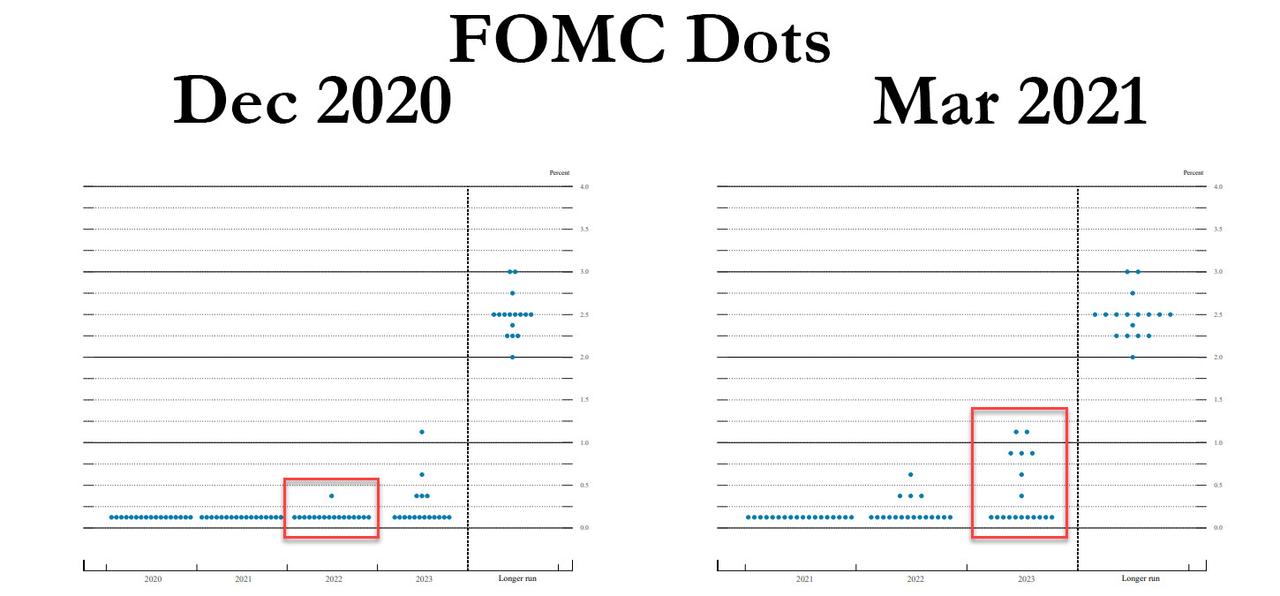

It’s not a stupid idea. One only has to glance at the Fed “dot plot” to see the risk of a boom and bust cycle:

Join the dots

That’s a rather sudden policy normalisation commencing in 2024, no?

That said, there is a comfort for markets as well in the MS chart of inflation breakevens which are indicating that inflationary pressures are still very cyclical and policy-driven not structural. Indeed, it illustrates that disinflation and deflation remain the underlying structure of the global economy. I agree given:

- Degloblsiation is young and will result in more Balkanisation of supply chains along security lines than it will repatriation to DMs.

- The IT and tech revolution remains in full swing with robots next.

- Middle-class demand will take decades to repair and may not even be possible if the will of policymakers wilts under pressure from interests. Moreover, there is little sign of authority grasping the nettle of develeraging for anybody.

- China has been a key source of inflationary demand for commodities, not just deflationary labour. The former is going to come apart faster than the latter ebbs away.

- There is a lot of energy deflation ahead as decarbonisation makes the economic energy system, especially in transport, immensely more efficient.

With all of this in mind, let me draw your attention to a few words from Credit Suisse:

US 30yr Bond Yields moved sharply higher on Thursday, although not ably outperformed on the curve, in line with our prior expectation that the steepening of 10s30s over the past week would continue in the short term before petering out again. Indeed, the 10s30s Bond Curve may now be forming a more important “head and shoulders” top, which would be confirmed below 69.5/69bps and projects a move to 52bps. We therefore look for the 30yr Yield to start lagging significantly on any further moves higher.

That’s exactly what I expect as the underpinning deflationary structure of the ongoing Great Moderation reasserts itself as we pass through the post-pandemic catch-up growth phase.

No doubt, US fiscal is going to remain a terrific tailwind for its economy over the next cycle as the Biden Administration injects $2-4tr ahead in infrastructure spending. But this is still fighting against a tsunami of deflationary forces that will take decades to beat.

I don’t discount the possibility of a boom and bust cycle. But my base case is for a boom and slump cycle, led by the US with more inflation there than elsewhere, but in consequence, more deflation everywhere else as the US dollar dominates and China slows.

That will mean factor rotations as much as cyclical rotations will remain the key to equity outperformance.