By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The Australian Government Budget has improved significantly since the 2020/21 Mid-Year Economic and Fiscal Outlook(MYEFO -published 17 December 2020).

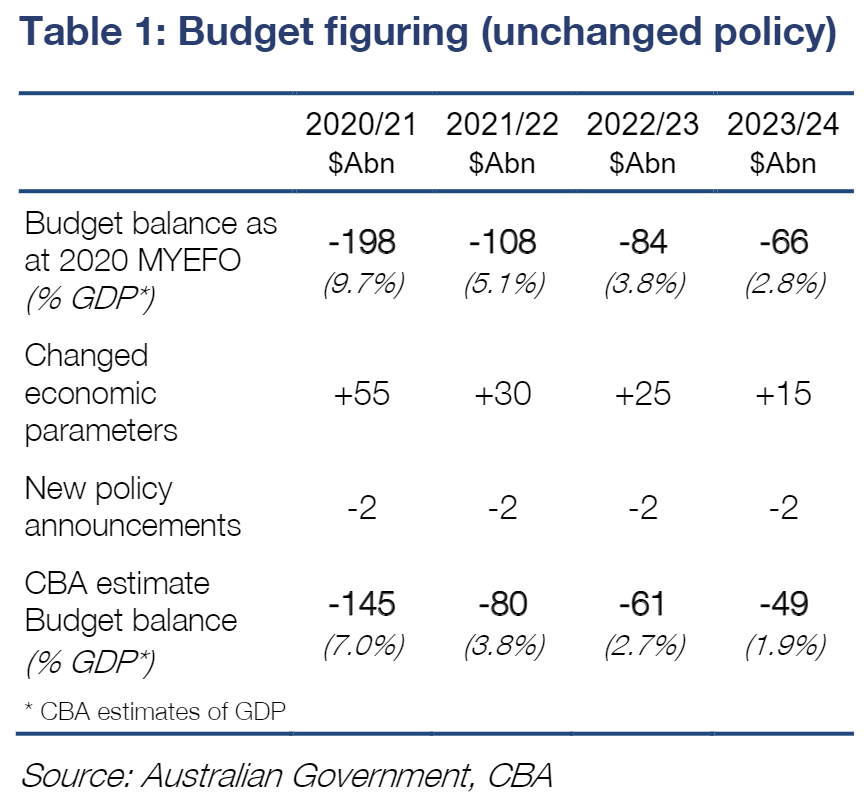

- Our point estimate for the revised underlying cash deficit in 2020/21 is $A145bn (unchanged policy basis).

- Changes to economic parameters and a better starting point mean we put the underlying cash deficit in 2021/22 at $A80bn (unchanged policy basis).

Overview:

The Australian economic recovery has been a lot stronger and a lot faster than the official forecasting family expected (i.e. the Commonwealth Treasury and the RBA).

A better performing economy means an improved fiscal position. And we expect to see a material upgrade to the Government’s economic forecasts and by extension the fiscal projections in the 2021 Budget (likely to be handed down on 11 May 2021, although the date is still to be confirmed).

We will publish a full 2021 Budget Preview in due course that will take into account potential policy changes which will impact the Government’s coffers. But we thought it to be a worthwhile exercise at this juncture to estimate the improvement in the Government’s fiscal position purely based on the improvement in the economy and any announced policy changes since the MYEFO.

Revenue up a lot and expenditure down

On our estimates, changes to the economic parameters that drive the fiscal forecasts will deliver a massive improvement of $A55bn in 2020/21relative to MYEFO (see Table 1).

Parameter changes primarily relate to changes in economic forecasts, particularly nominal GDP which drives the revenue side of the equation, as well as the level of unemployment which underpins welfare payment forecasts. The news around both nominal GDP and the labour market is significantly better than was expected in the 2020/21 MYEFO.

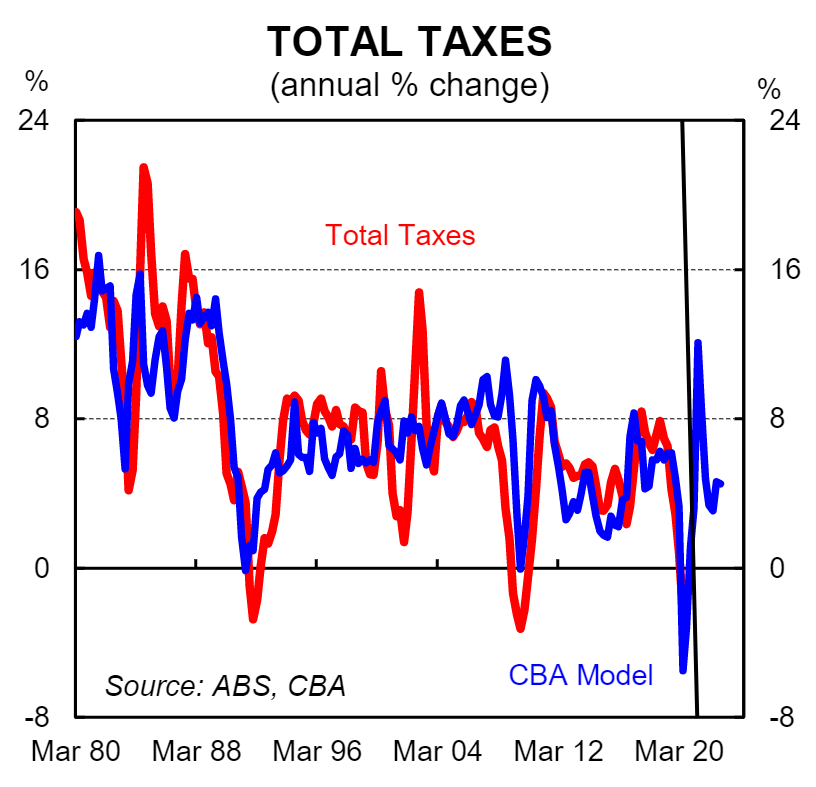

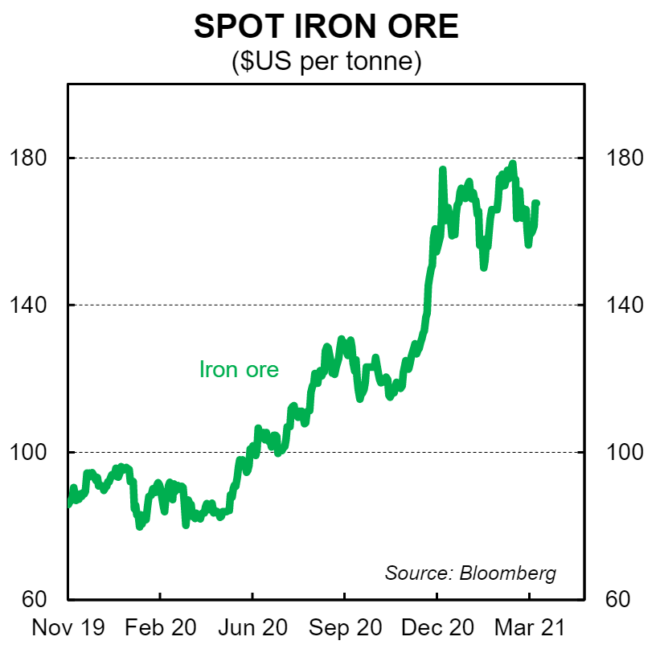

The stronger than expected improvement in nominal GDP has been driven by a sharp rebound in production and a surge in commodity prices, particularly the price of iron ore. Our fiscal model indicates that tax receipts should be boosted by ~$A35bn in 2020/21 relative to what was expected in the MYEFO (indeed the monthly Government financial statistics indicate that revenue was tracking $A10.7bn higher in February relative to MYEFO).

The expenditure side also looks in much better shape. The unemployment rate has so far undershot Treasury estimates which means unemployment benefit payments will be lower than forecast. There will be JobKeeper savings too. Based on the monthly Government financial statistics it appears that the JobKeeper payments in Q1 2021 were materially lower than Treasury forecast in the MYEFO.

Overall we estimate a reduction in total expenditure of $A20bn in 2020/21 relative to MYEFO (excluding the two policies outlined below). That figures primarily comprises the savings from both less people receiving JobKeeper and JobSeeker. In addition it includes an expectation that the impact of the expiry of JobKeeper in terms of job losses will not be as large as Treasury would have assumed in the MYEFO (note that we don’t have specifics, but measures of labour demand are no doubt stronger than the Government would have expected at end-March 2021 when the MYEFO was published).

New policy announcements since MYEFO comprise the permanent increase in the JobSeeker payment of $A50 per fortnight. This is forecast to add ~$0.7bn to the Budget bottom line in 2020/21 and $A9bn over four years. The recently announced tourism support package is expected to cost $A1.2bn this fiscal year.

Looking further out, we estimate that on an unchanged policy basis the underlying cash deficit should be $A80bn (3.8% of GDP) in 2021/22. This represents an improvement of $A38bn relative to MYEFO. This is not, however, the number that we expect to see in the 2021 Budget.

The Government will no doubt announce new policies in the 2021 Budget that will add to the Budget bottom line. We will incorporate provisions for such policies in our Budget Preview, to be published late April, once we have a sense of what policy direction the Government intends to take in 2021/22.