RBNZ tightens LVR clamps on “speculative” property market

Advertisement

The Reserve Bank of New Zealand (RBNZ) yesterday performed a stunning U-turn, reintroducing loan-to-value (LVR) mortgage restrictions just 10 months after such restrictions were lifted to aid the nation’s COVID-19 response.

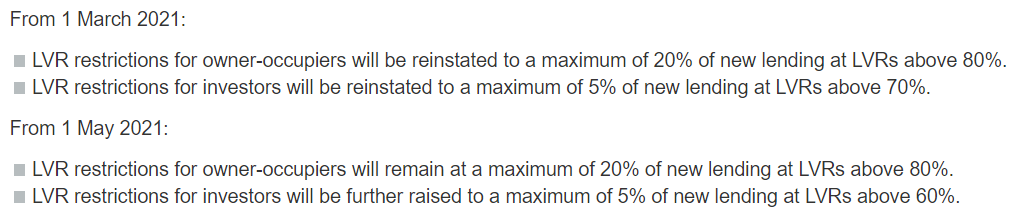

Under the changes, most investors will need 40% deposits and most owner-occupiers 20% deposits; although there are explicit carve-outs for new residential construction:

The RBNZ has chosen a staged approach to enable banks to manage their pipelines of loan applications that have been approved but have not yet settled.

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement