Industry Super Australia (ISA) continues to lobby the federal government to increase the superannuation guarantee (SG), arguing that if the super rate increase was abandoned, it would “heap pressure on the pension”:

ISA said it was vital the legislated increases in the superannuation guarantee – from 9.5 per cent to 12 per cent of wages – go ahead as planned.

“Ditching the legislated increase would heap pressure on the pension and be a cruel blow to those who had to make the tough choice to sacrifice retirement savings to get them through the pandemic downturn,” ISA CEO Bernie Dean said…

“Ripping [the super guarantee rise] away from [young workers] would be a cruel double blow,” Mr Dean said.

“It would leave them with far less at retirement and saddle these young workers with a whopping pension bill they pay for through higher taxes.”

As usual, ISA is conveniently looking at only one side of the equation – the cost to the Aged Pension – while ignoring entirely the massive budgetary costs of superannuation.

The Treasury’s 600-page Retirement Income Review Final Report slams the ISA’s approach and shows unambiguously that lifting the SG to 12% would cost the federal budget far more than it saves in Aged Pension costs [my emphasis]:

Advertisement

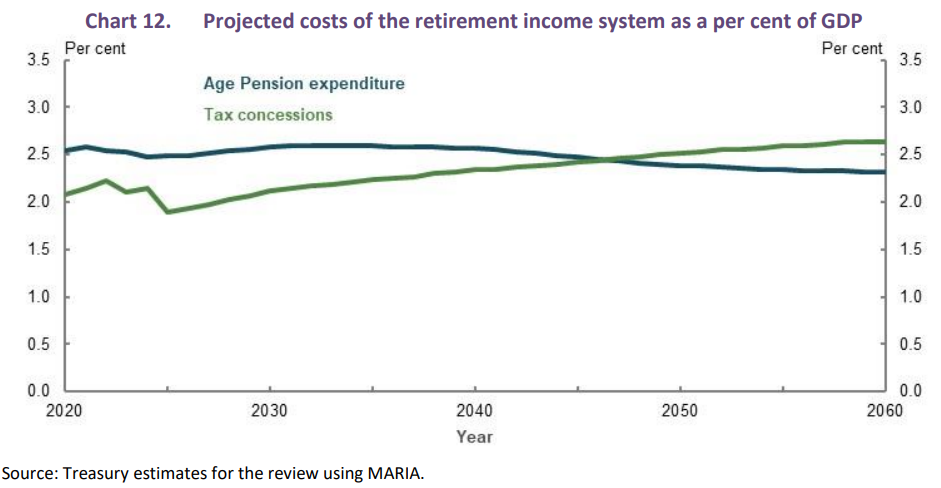

Government expenditure on the Age Pension as a proportion of GDP is projected to fall slightly over the next 40 years to around 2.3 per cent [from 2.5 per cent]. Higher superannuation balances reduce Age Pension costs. The cost of superannuation tax concessions is projected to grow as a proportion of GDP and exceed that of Age Pension expenditure by around 2050. This is due to earnings tax concessions. The increase in the SG rate to 12 per cent will increase the fiscal cost of the system over the long term…

The sustainability of compulsory superannuation is best assessed by looking at its full budgetary impact and not just the reduction in Age Pension expenditure as the superannuation system matures. The cost of superannuation tax concessions also needs to be taken into account.

…as the superannuation system matures, the cost of superannuation tax concessions is projected to grow as a proportion of GDP such that by around 2050 it exceeds the cost of Age Pension expenditure as a per cent of GDP (Chart 12). This is the result of growth in the cost of earnings tax concessions…

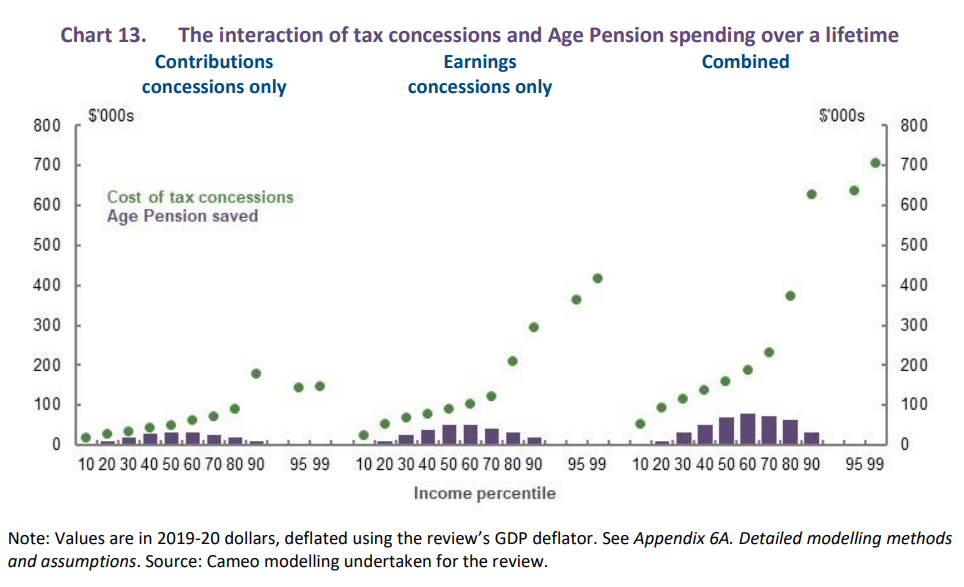

Across the income distribution, the lifetime cost of superannuation tax concessions is projected to outweigh the associated Age Pension saving (Chart 13)…

Modelling by actuary firm Rice Warner also showed unambiguously that lifting the SG would cost the federal budget over both the short and long-term:

“Our modelling shows that the legislated increase in the SG will not have much impact on the Age Pension for many years but will reduce it by about 0.1% of GDP in the second half of this century on current means testing settings. Conversely, the tax concessions from the increase are more immediate and they will average about 0.22% of GDP throughout this century”.

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

Let’s also remember that superannuation concessions cost the federal budget $43 billion a year and are very poorly targeted to high income earners, who receive the lion’s share of taxpayer assistance:

The already excessive cost of superannuation concessions necessarily means there are less funds available in the federal budget to lift the Aged Pension.

If budget sustainability and equity in retirement outcomes was the true goal, there is a strong case to abolish superannuation altogether and to channel the immense budget savings into lifting the Aged Pension.

Because it is the high cost of superannuation concessions that is preventing the pension from being lifted. Lifting the SG to 12% would only make the situation worse.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.