Suddenly irresponsible mortgage lending is a problem!

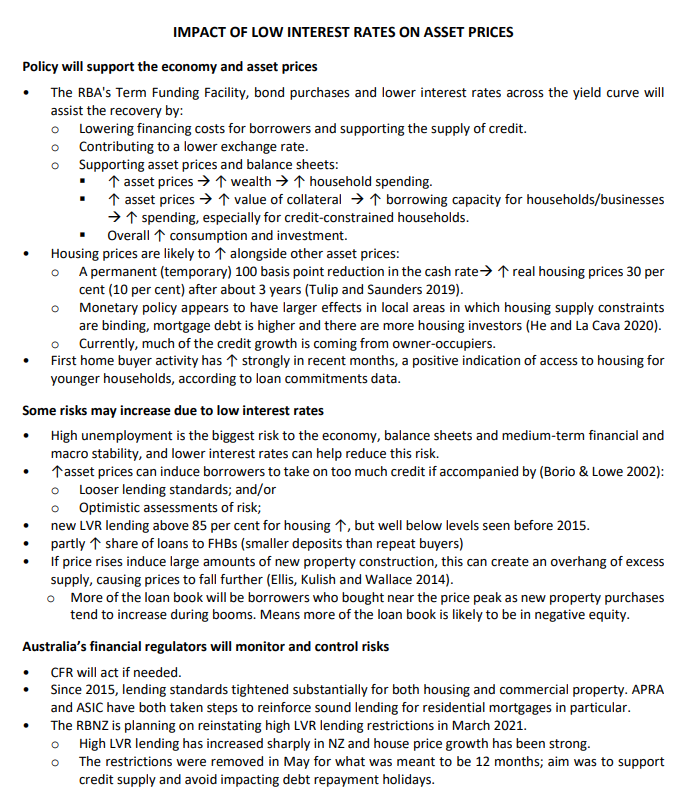

Freedom of Information (FOI) documents released on Friday by the Reserve Bank of Australia (RBA) reveals that it saw risks in its decision to cut the cash rate to 0.10%, alongside introducing the Term Funding Facility (TFF) for banks and buying government bonds.

In particular, the RBA noted that “a permanent (temporary) 100 basis point reduction in the cash rate [could] ↑ real housing prices 30 percent (10 per cent) after about 3 years”.

However, the RBA said the Council of Financial Regulators (CFR) “will act if needed” to control risks:

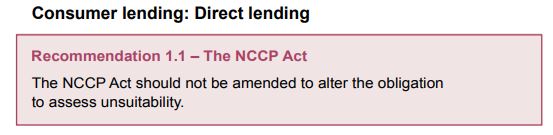

This is a curious admission by the RBA given that it supported Treasurer Josh Frydenberg’s decision to scrap responsible lending rules, which was in contravention of the very first recommendation of the Hayne Banking Royal Commission that such rules remain in place:

Indeed, in the lead up to the Morrison Government’s decision to scrap responsible lending rules, RBA Governor Phil Lowe told the Standing Committee on Economics that Australian mortgage restrictions had become too strict and were constraining the economy:

“The pendulum has probably swung a bit too far to blaming the bank if a loan goes bad, because the bank didn’t understand the customer; if it had done proper due diligence—this is the mindset of some—the bank would never have made the loan. So some of the banks have had this mindset, ‘Well, we can’t make loans that go bad'”.

The RBA and Treasury also directly undermined ASIC’s “wagyu and shiraz” responsible lending suit against Westpac:

The Australian Securities and Investments Commission has decided not to appeal to the High Court its case against Westpac for alleged responsible lending failures, after the heads of the Reserve Bank of Australia and Treasury both privately warned it would exacerbate economic uncertainty caused by COVID-19…

Worse, Australia’s financial regulators, ASIC and APRA, were not even consulted on the decision to scrap responsible lending rules:

Financial regulators weren’t asked for their assessment on the scrapping of responsible lending laws before the government’s surprise announcement, according to testimony, leaving the head of a leading regulator to learn about the controversial decision in media reports.

Commissioners from ASIC and APRA were questioned about the scrapping of responsible lending laws before a parliamentary committee last week, where they revealed they were given little-to-no notice and were not asked for their views on the decision…

“I’m the commissioner with responsibility for credit,” [ASIC’s Sean Hughes said], “and I was first advised when I read the Treasurer’s media statement through the media on the morning of 25 September.”

So, we find ourselves in the bizarre situation whereby the federal government, with the blessing of the RBA and Treasury, neutered our financial regulators by green-lighting irresponsible lending.

And yet these very same regulators, under the auspices of the CFR, will then be called upon to rein-in lending standards as the housing market inevitably inflates, due partly to irresponsible lending.

Expect no action this year. Australia is facing a case of closing the regulatory gate long after the mortgage horse has bolted.