National Seniors Australia chief advocate Ian Henschke wants a universal pension scheme that isn’t means tested.

“Review after review complains about older people failing to spend down their capital; they don’t blame the system, they blame the retiree. And then they wonder why no one’s listening,” he told Savings.com.au.

“By setting income and asset limits which restrict you from, first, getting a pension, and second, limiting your entitlement, it punishes you for having more.”

Mr Henschke’s suggestions come on the heels of Superannuation Minister Jane Hume’s call to scrap the legislated increase in the superannuation guarantee. The minister says such increases would only serve to encourage retirees to hoard instead of spend…

The top two pension systems in the world – in The Netherlands and Denmark – both have defined benefits schemes, or universal basic pensions, in place.

Australia’s refusal to implement such a scheme hampers retiree confidence to go out and spend, instead of hoarding cash and assets, says Mr Henschke.

“That’s the beauty of a properly designed universal pension. It takes away the year-on-year risk, but ensures it is fiscally sustainable and fair,” he said.

A universal basic income could, over time, also be good for the government’s bottom line, as it would eliminate the need for massive administration costs.

“It would get rid of the pension assets and income tests, doing away with the need for unfair taper rates, deeming rates and work restrictions, and end the need to engage with Centrelink,” Mr Henschke said in May last year.

“If everyone of pension age received a pension, retirees could just add this to their other income and pay tax. Means testing is costly to administer and leads to perverse outcomes, which are more apparent in the current crisis.

“Asset taper rates unfairly penalise those who save more for their retirement. Income tests undermine ongoing workforce participation and lead to ongoing anger over deeming rates.”

NSA’s proposal makes a lot of sense and could easily be funded by abolishing the compulsory superannuation system, which is overly costly, inefficient and inequitable.

Compulsory superannuation acts like a tax and forces people to forgo current consumption, which is especially pernicious for lower-income earners.

Advertisement

Moreover, because superannuation balances at retirement depend on how long one works and how much they earn, the system inevitably misses lower income earners and those with broken work patterns like mothers.

Compulsory superannuation has also created a massive trough, worth some $30 billion a year, that has attracted snouts across the financial services industry like the big four banks. Australian management fees are among the highest in the world with Australian households spending twice as much each year on superannuation fees as they do on electricity.

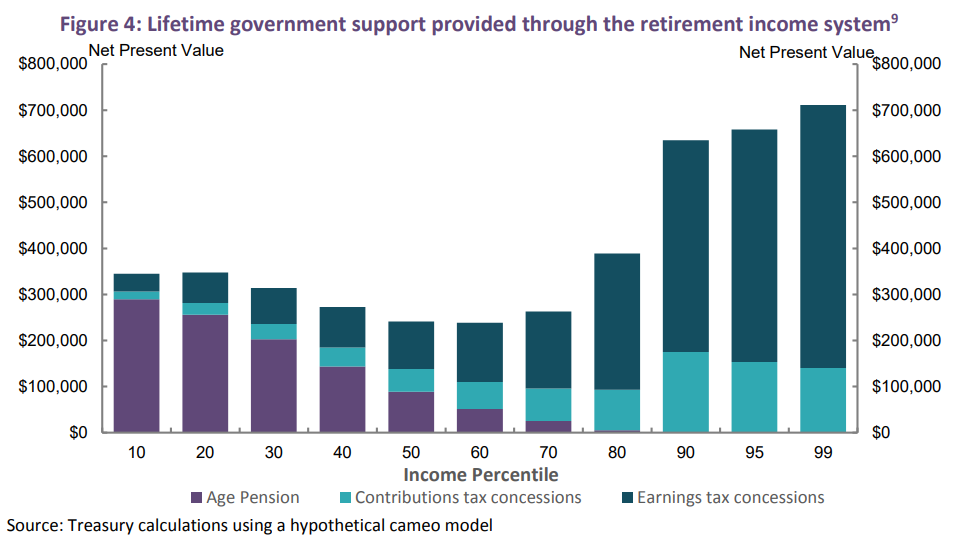

Superannuation concessions already cost the federal budget around $43 billion a year and are very poorly targeted to high income earners, who receive the overwhelming majority of taxpayer assistance through the retirement system:

Advertisement

Worse, the recently released Retirement Income Review estimates that the cost of superannuation concessions will dwarf the Aged Pension, and costs taxpayers more in net terms over the long-run:

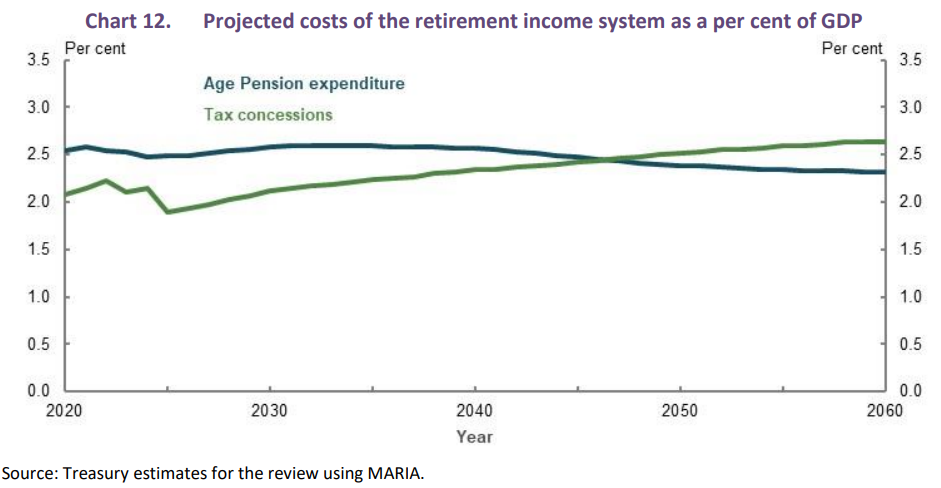

As the superannuation system matures, the cost of superannuation tax concessions is projected to grow as a proportion of GDP such that by around 2050 it exceeds the cost of Age Pension expenditure as a per cent of GDP (Chart 12). This is the result of growth in the cost of earnings tax concessions…

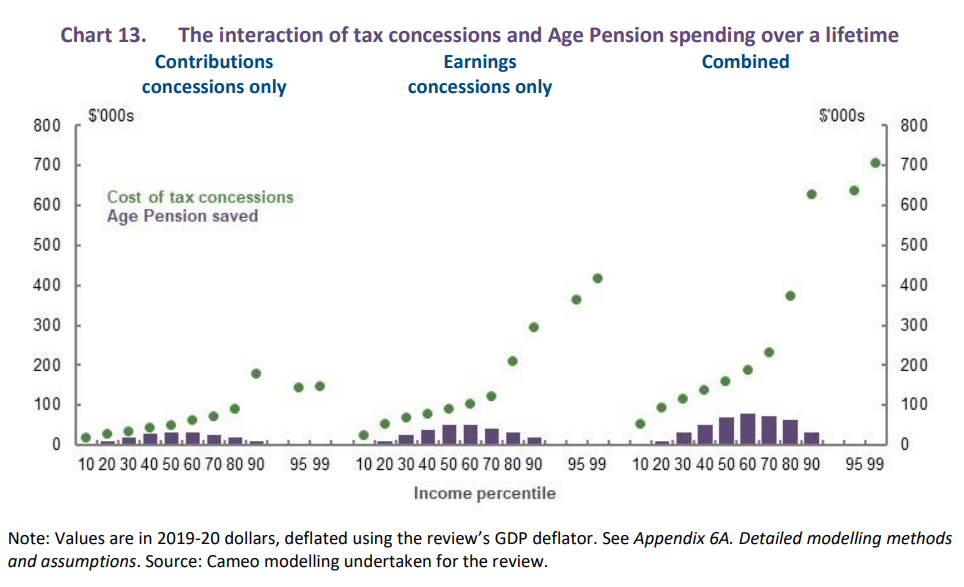

To the extent that superannuation tax concessions are contributing to higher superannuation balances of lower- to middle- income earners, they help to reduce Age Pension expenditure. But the main influence behind the growth in superannuation balances is the SG. Tax concessions are largely concentrated among higher-income earners who are close to and above preservation age. Across the income distribution, the lifetime cost of superannuation tax concessions is projected to outweigh the associated Age Pension saving (Chart 13)…

Advertisement

By extension, the massive costs and inefficiency surrounding compulsory superannuation means there are less funds available in the federal budget to lift the Aged Pension – Australia’s genuine retirement pillar.

Given the obscene cost, inefficiency and poor targeting of superannuation concessions, optimal public policy dictates unwinding these concessions and using the money saved to boost the Aged Pension.

Abolishing the compulsory superannuation system in favour of a universal aged pension has merit and should be given detailed consideration.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.