On average, retirees aged over 75 have just under $1m in equity in their homes plus other financial assets, according to the Grattan Institute, dwarfing their $127,000 still in super.

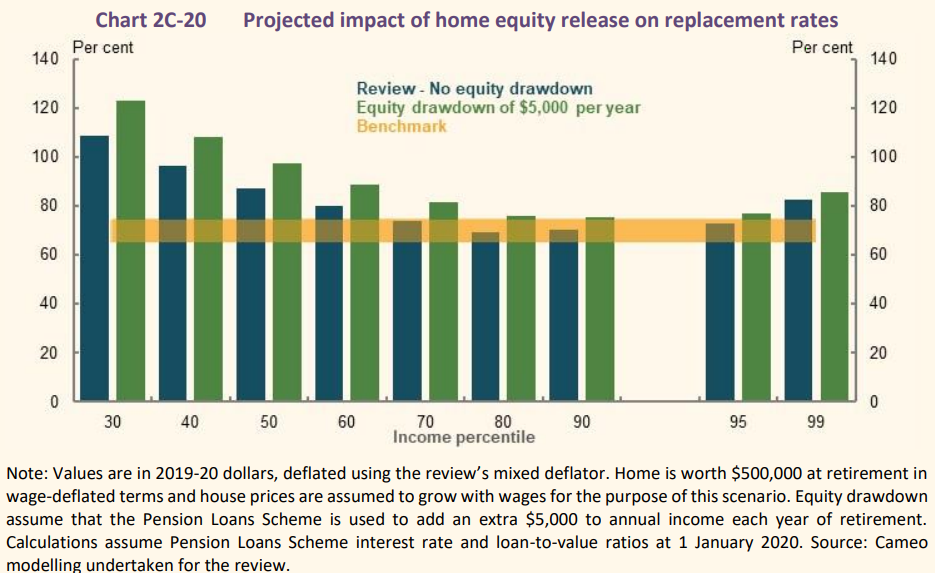

Why shouldn’t “eating your house”, or at least having a nibble using a reverse mortgage, be a reasonable option for retirees who run out of super or want a higher living standard than the fallback Age Pension can provide? “Withdrawing $5000 a year would mean that retirees still have about three-quarters of the value of their home at age 92, for a house worth $500,000 at retirement,” the review says…

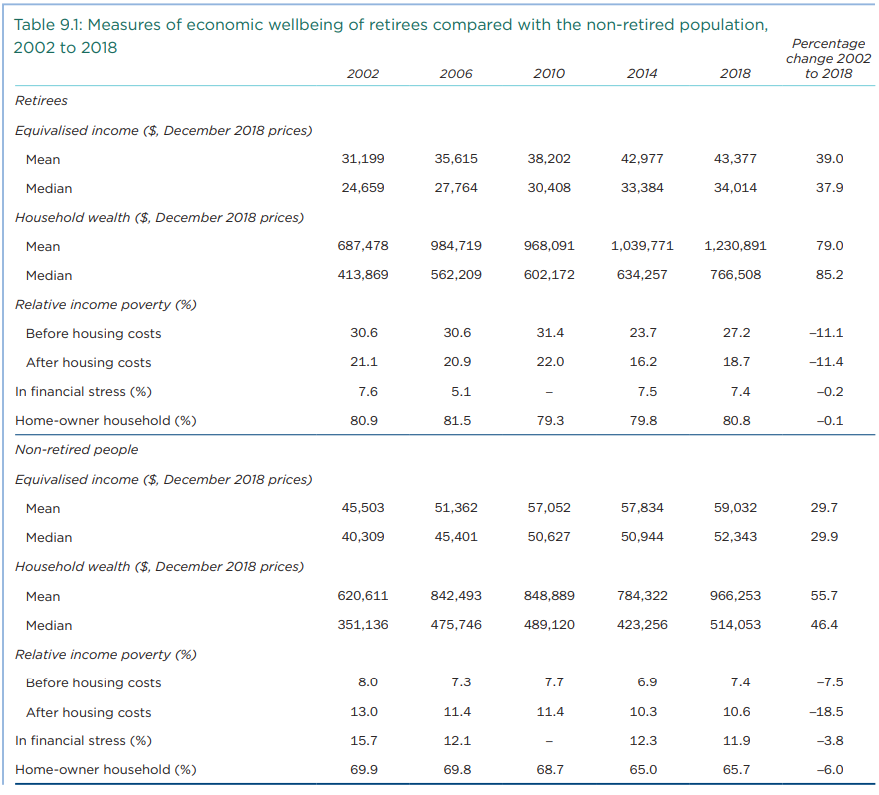

Too right. The latest Household, Income and Labour Dynamics in Australia (HILDA) report showed that Australians aged 65-plus enjoyed by far the biggest increase in wealth between 2002 and 2018:

Prior to 2010, the median wealth of people aged 65 to 74 was less than that of those aged 45 to 54, but by 2010 the median wealth of the 65 to 74 age group had overtaken the median wealth of those aged 45 to 54. This reflects the very strong growth in median wealth between 2002 and 2018 for the 65 to 74 age group, with the median increasing by 98.1%. Growth was also strong for the oldest age group, increasing by 83.4% between 2002 and 2018.

Advertisement

Meanwhile, Treasury’s 600-page Retirement Income Review took direct aim at pensioners’ houses, questioning why housing was excluded from the assets test to qualify for the aged pension:

The Pension Loans Scheme is an effective option for accessing equity in the home for both age pensioners and self-funded retirees. The current exemption of the principal residence from the Age Pension assets test is a disincentive to using the equity in the home to support retirement incomes…

Using relatively small portions of home equity through the Pension Loans Scheme or similar equity release products can substantially improve retirement incomes for many people… This is effectively a reverse mortgage for age pensioners and self-funded retirees, where income from the scheme is not assessable in the Age Pension means test…

Use of the Pension Loans Scheme is limited. Between 1 July 2018 and 17 January 2020, more than 9,000 people made downsizer contributions…

Releasing home equity can boost retirement incomes with a modest impact on debt. Withdrawing $5,000 a year would mean that retirees still have about three-quarters of the value of their home at age 92, for a house worth $500,000 at retirement. Retirees with higher value homes would maintain even higher proportions of home equity while still benefiting from significant improvements in replacement rates…

At present, the majority of age pensioners are home owners, so removing the assets test exemption for housing could have a significant impact on the adequacy of retirement outcomes…

Including the full value of the home in the Age Pension assets test would remove the inequities between renters and home owners and remove the incentive to invest in housing due to the exemption. However, it would have significant adequacy impacts on retirees. Channels to mitigate this impact include changes to the rate of Age Pension or providing increased access to equity release (e.g. the Pension Loans Scheme)…

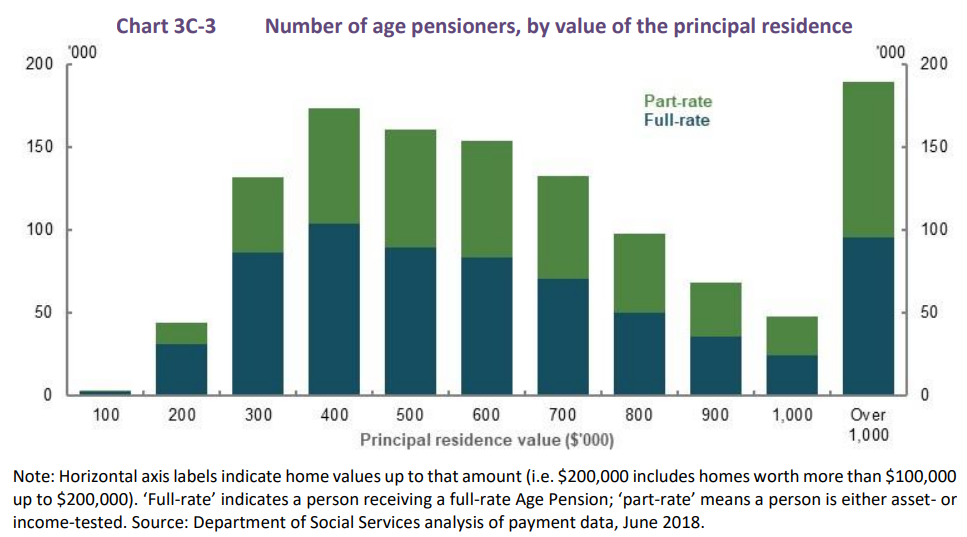

Given the exemption of the principal residence reduces their assets assessable under the Age Pension assets test, a large number of home owners are relying on the Age Pension (Chart 3C-3)…

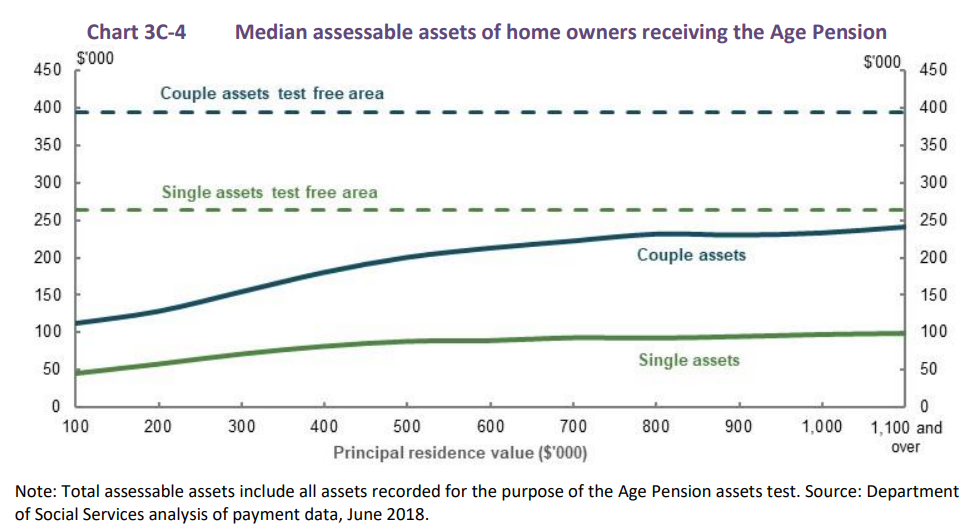

Around 63 per cent of home owners receiving the Age Pension have assessable assets below the full-rate threshold. The median value of assessable assets does not seem to vary proportionately with the value of the retiree’s principal residence (Chart 3C-4).

One logical policy solution that MB has espoused is to:

Advertisement

Include one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2022), thus allowing current retirees and prospective retirees adequate time to make arrangements; and

Significantly raise the overall pension asset test threshold as well as the base rate.

Under this solution, house-rich pensioners choosing to remain in place could continue to receive an income stream as they do now under the Aged Pension via the Pension Loans Scheme, but with less drain on the Budget and on younger taxpayers. But they would similarly be incentivised to move as the family home would no longer be a tax free shelter.

Poorer retirees that do not own a dwelling would also be made better-off via the increase in the overall assets test (thus allowing greater financial assets to be held without cutting-off access to the pension), as well as the increase in the pension base rate.

Advertisement

It’s a solution that would greatly improve equity and ensure that Australia’s welfare system is better targeted towards those in genuine need.

It would also ensure that the pension system evolves alongside the structural reduction in home ownership rates, by making the system more neutral towards property ownership and financial assets.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.