It’s become increasingly apparent that New Zealand is facing another housing bubble.

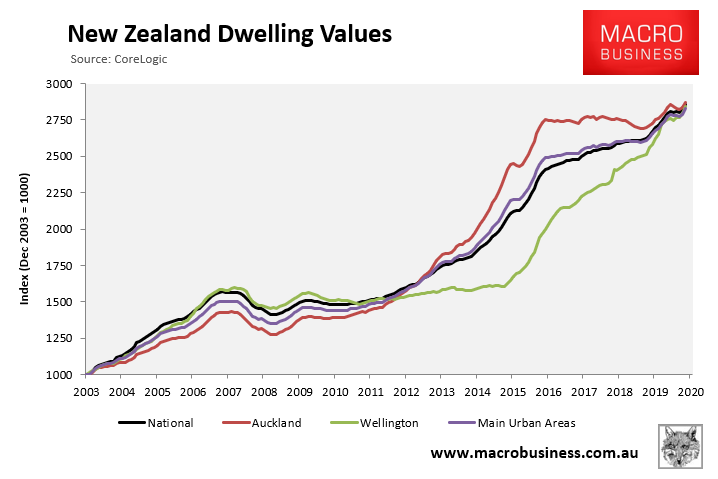

New Zealand’s housing market has brushed off the COVID-19 pandemic, recording 2.1% value growth in the two months to October to be up 8.0% year-on-year – reaching another record high:

According to CoreLogic:

The support mechanisms put in place by the Government (wage subsidies) and banks (mortgage deferrals) have helped cushion the market, while the Reserve Bank of New Zealand’s (RBNZ) intervention (Quantitative Easing programme lowering interest rates, temporary removal of loan-to-value ratio (LVR) restrictions) now appears to be boosting demand and therefore contributing to the uplift in value growth.

CoreLogic Head of Research, Nick Goodall, says, “Indeed, the RBNZ has acknowledged a consequence of its monetary policy is increasing asset prices, but that this is a better outcome than the counter-scenario of a loss in confidence, resulting in decreasing property values.”

A lack of supply of available properties on the market is also a key contributor to increasing prices, with listings hovering at all-time low levels across the country.

As noted above, part of the reason for the price rebound is that the RBNZ lifted LVR restrictions in May for at least 12 months, due in part technical reasons around the mortgage deferral scheme, which runs until March 2021. These LVR limits had been in place in some form since 2013.

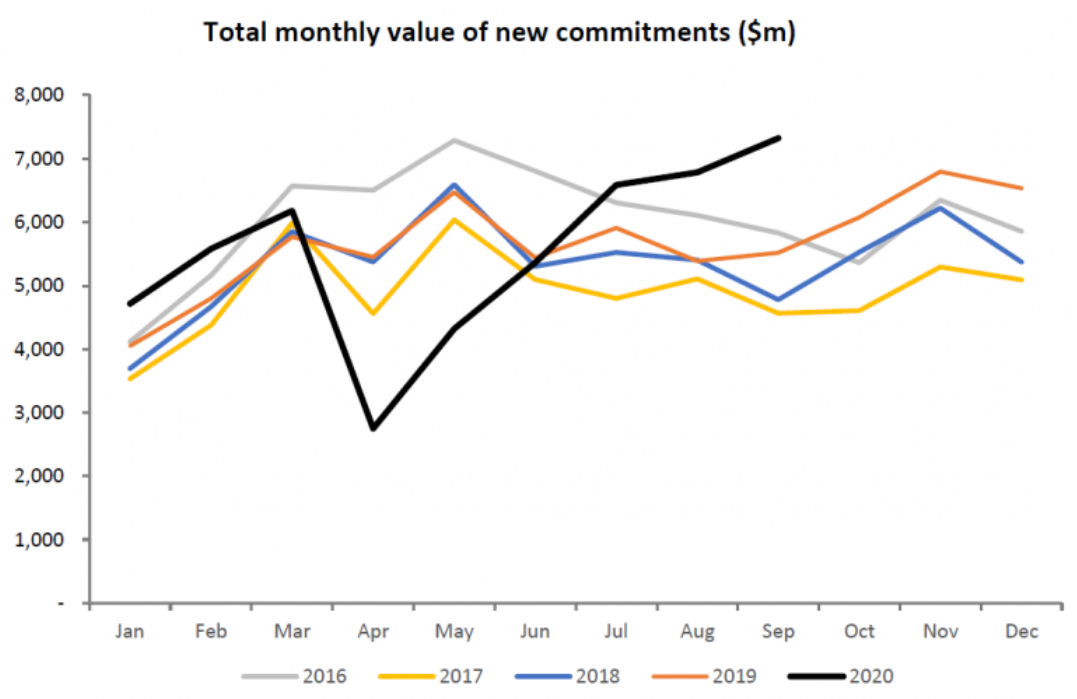

The upshot is that mortgage commitments are now booming which, when combined with low stock levels, is fueling price rises:

According to the RBNZ, $7.3 billion of mortgage lending activity took place in September – the highest month on record since the survey began in 2013 and almost $2 billion (32.8%) above the same month last year.

ANZ’s latest Property Focus reported that FOMO (Fear of Missing Out) has now infested New Zealand’s property market:

A “frothy” speculative element appears to be emerging, with FOMO (fear of missing out) part of the equation. Buyers are of the view that it is a good time to buy despite being in the midst of an enormous economic downturn, and house prices appear to be moving against the tide of fundamentals from already very elevated levels. That could contribute to a more volatile cycle if a turn in the market comes – particularly if buyers entering the market have high debt to income, making them more vulnerable to income strains.

Hilariously, New Zealand’s Property Investors Federation is blaming first home buyers for “making the housing crisis worse”:

The Property Investors Federation is blaming first home buyers for the housing crisis, warning that by taking rental properties off the market they’re making it worse.

Speaking to RNZ on Tuesday, executive officer Sharon Cullwick argued that while property investors aren’t helping solve the crisis, they’re not the problem.

“If a first home buyer purchases a property that was a rental property, then you’ll need another house to house the extra people living in that rental house,” she told reporter Eva Corlett.

“So every time a first home buyer buys a house – even though it’s great they are getting into the market – it actually makes the housing crisis worse.”

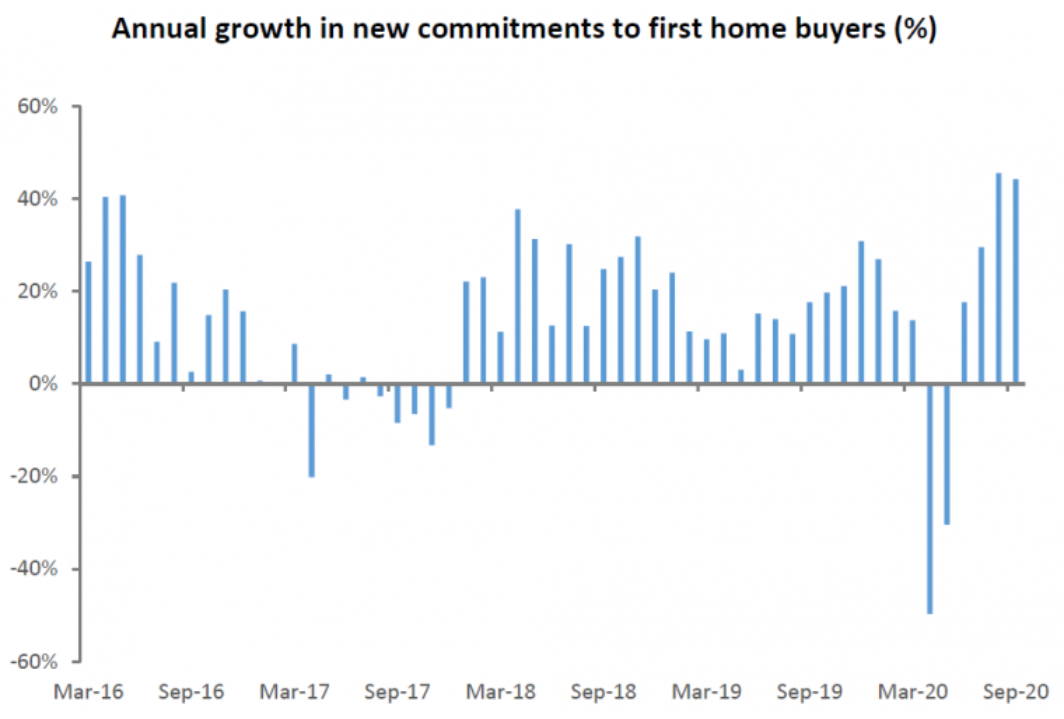

Sharon Cullwick’s argument defies logic. If a first home buyer buys a home rather than rents, they remove rental supply in the same proportion as they remove rental demand. So it’s a nill all draw.

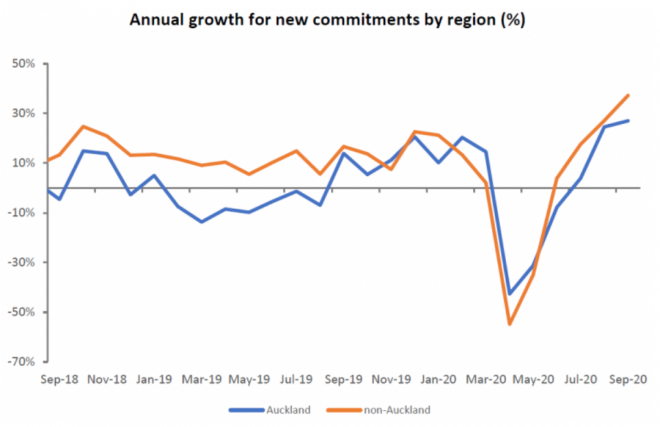

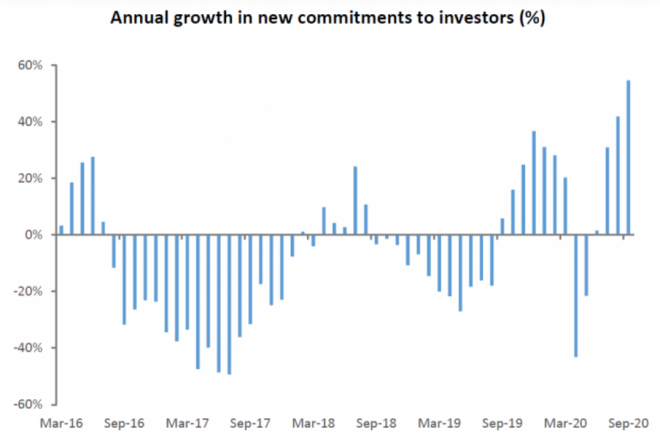

She also has conveniently left out that investor demand has surged more than first home buyer demand:

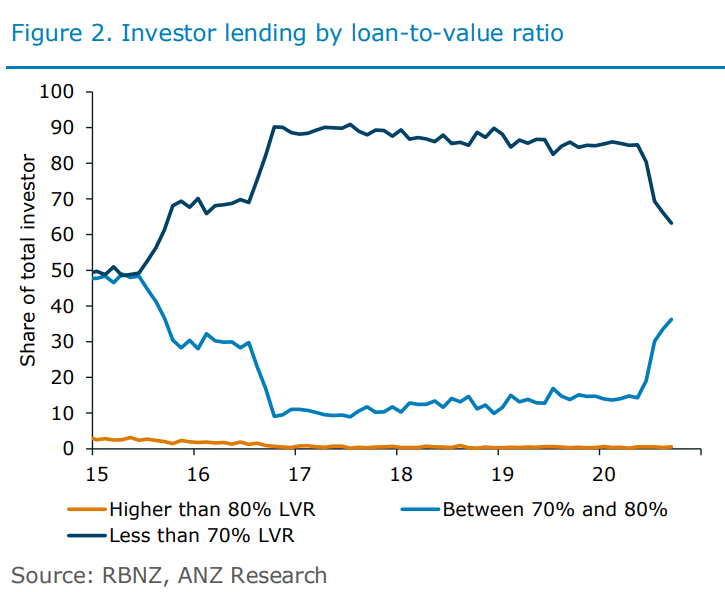

Or that investors are engaging in riskier lending:

Regardless, Prime Minister Jacinda Adern has her work cut out if she is to fulfil her promise of tackling New Zealand’s housing crisis.